|

市場調查報告書

商品編碼

1876628

農產品包裝設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Packaging Equipment for Agricultural Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

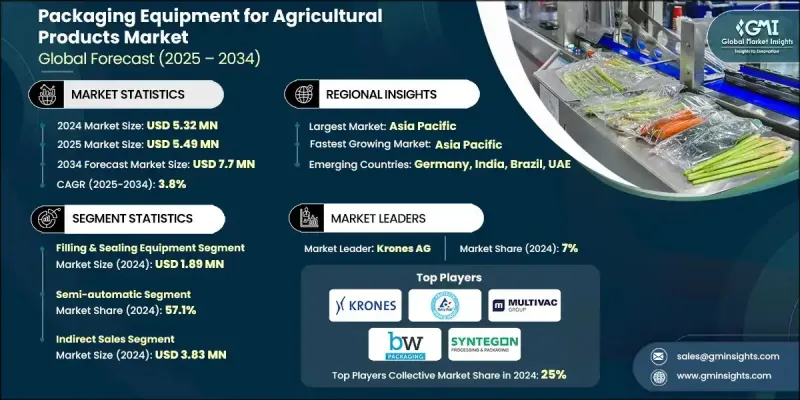

2024 年全球農產品包裝設備市場價值為 532 萬美元,預計到 2034 年將以 3.8% 的複合年成長率成長至 770 萬美元。

市場擴張的驅動力在於自動化包裝系統的日益普及,這些系統能夠提升營運效率、準確性和生產力。自動化設備簡化了填充、封口和貼標等流程,幫助生產商減少對人工的依賴,最大限度地減少人為錯誤,並加快大規模農業生產的生產速度。智慧包裝技術的整合,包括能夠實現即時追蹤和資料採集的功能,正在創造顯著價值。這些技術增強了可追溯性,支援食品安全合規,並最佳化了高階農產品出口商和供應商的庫存管理。消費者對品質保證和透明度的日益成長的期望也推動了自動化和智慧包裝解決方案的普及。隨著全球食品安全法規的不斷收緊,生產商正增加對具備數位化監控和預測性維護功能的設備的投資。這種轉變提高了營運可靠性,改善了數據驅動的決策,並減少了包裝浪費。開發模組化和物聯網賦能包裝系統的公司,在這個不斷變化的產業格局中佔據了有利地位,有望獲得競爭優勢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 532萬美元 |

| 預測值 | 770萬美元 |

| 複合年成長率 | 3.8% |

2024年,半自動包裝機械市佔率達57.1%。由於價格實惠且靈活,半自動系統仍然是中小農業生產者的首選。這些配置兼顧了手動操作和全自動操作,既能幫助企業降低勞動成本,又能維持生產的彈性。它們使生產者無需大量資本投資即可擴大產能,為擴大生產規模提供了一種經濟高效的方法。

2024年,間接銷售通路創造了383萬美元的銷售額,佔據了相當大的市場。間接銷售模式使製造商能夠與區域經銷商和經銷商合作,更容易進入那些難以直接進入的市場。這種方式在新興地區尤其重要,因為成熟的分銷網路能夠提供更好的市場滲透率,並幫助企業更好地了解當地的農業實踐。這種分銷合作關係使企業能夠在無需建立獨立銷售基礎設施的情況下,有效地拓展客戶群。

2024年,美國農產品包裝設備市場佔78.2%的市場佔有率,市場規模達89萬美元。由於先進的農業運作和政府為促進永續發展和食品安全而製定的支持性法規,美國市場展現出高度的成熟度。自動化技術在整個產業中廣泛應用,農場和加工廠紛紛投資先進的填充、封口和堆疊設備,以滿足日益成長的對速度、一致性和合規性的需求。

全球農產品包裝設備市場的主要參與者包括BW Packaging、Combi Packaging Systems、Concetti Group、General Packer、Haver & Boecker、IMA Group、Krones AG、Landpack、MULTIVAC Group、Paglierani、Premier Tech Systems &這些領導企業正致力於多項策略性舉措,以鞏固其市場地位。許多企業優先考慮產品創新,開發模組化、物聯網賦能且節能的系統,以滿足日益成長的智慧自動化包裝解決方案需求。他們正拓展與當地經銷商和區域經銷商的合作關係,以擴大市場覆蓋範圍並提升客戶可及性,尤其是在新興經濟體。此外,各企業也投資於數位監控能力和預測性維護功能,以提高營運可靠性並減少停機時間。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 自動化與智慧包裝整合

- 多元化發展,進軍農業化學品及特用產品領域

- 永續發展驅動的設備需求

- 產業陷阱與挑戰

- 高昂的資本成本和投資報酬率壓力

- 供應鏈波動

- 機會

- 智慧包裝設備

- 環保包裝生產線

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依設備類型

- 監管環境

- 標準和合規要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依設備類型分類,2021-2034年

- 主要趨勢

- 灌裝和封口設備

- 垂直成型-填充-密封 (VFFS)

- 水平成型-填充-密封(HFFS)系統

- 其他

- 分類和分級設備

- 裝袋和包裝線

- 稱重和分份系統

- 碼垛和包裝設備

第6章:市場估算與預測:依營運方式分類,2021-2034年

- 主要趨勢

- 手動的

- 半自動

- 自動的

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 新鮮農產品包裝

- 穀物和種子加工

- 動物飼料和農業投入

- 其他(雞蛋、乳製品等)

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 初級農業生產者

- 農產品及食品加工設施

- 其他(農業合作社和協會、農民所有的加工設施等)

第9章:市場估算與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 直銷

- 間接銷售

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- BW Packaging

- Combi Packaging Systems

- Concetti Group

- General Packer

- Haver & Boecker

- IMA Group

- Krones AG

- Landpack

- MULTIVAC Group

- Paglierani

- Premier Tech Systems & Automation

- STATEC BINDER

- Syntegon Technology

- Tetra Pak

- WOLF Packaging

The Global Packaging Equipment for Agricultural Products Market was valued at USD 5.32 million in 2024 and is estimated to grow at a CAGR of 3.8% to reach USD 7.7 million by 2034.

The market's expansion is driven by the increasing adoption of automated packaging systems that enhance operational efficiency, accuracy, and productivity. Automated equipment simplifies processes such as filling, sealing, and labeling, helping producers reduce dependence on manual labor, minimize human error, and accelerate throughput for large-scale agricultural operations. The integration of smart packaging technologies, including features that enable real-time tracking and data collection, is adding significant value. These technologies enhance traceability, support food safety compliance, and optimize inventory management for exporters and suppliers dealing with premium agricultural goods. Rising consumer expectations for quality assurance and transparency are also fueling the adoption of automated and intelligent packaging solutions. As food safety regulations continue to tighten globally, producers are increasingly investing in machinery that offers digital monitoring and predictive maintenance capabilities. This shift enables greater operational reliability, improves data-driven decision-making, and reduces packaging waste. Companies developing modular and IoT-enabled packaging systems are well-positioned to gain a competitive edge in this evolving industry landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.32 Million |

| Forecast Value | $7.7 Million |

| CAGR | 3.8% |

In 2024, the semi-automatic packaging machines segment held a 57.1% share. Semi-automatic systems remain a preferred choice among small and medium agricultural producers due to their affordability and flexibility. These configurations strike a balance between manual and fully automated operations, helping businesses reduce labor costs while maintaining adaptability in production. They allow producers to expand output capacity without requiring major capital investment, offering a cost-efficient approach for scaling production.

The indirect sales channels generated USD 3.83 million in 2024, capturing a substantial portion of the market. Indirect sales models enable manufacturers to collaborate with regional distributors and dealers, making it easier to reach markets that are challenging to access directly. This approach is especially valuable in emerging regions where established distributor networks provide better market penetration and understanding of local agricultural practices. Such distribution partnerships allow companies to grow their customer base efficiently without building independent sales infrastructures.

United States Packaging Equipment for Agricultural Products Market held a 78.2% share and generated USD 0.89 million in 2024. The U.S. market demonstrates high sophistication due to advanced agricultural operations and supportive government regulations promoting sustainability and food safety. Automation is widely implemented across the industry, with farms and processing facilities investing heavily in advanced filling, sealing, and palletizing equipment to meet growing demand for speed, consistency, and compliance.

Key players in the Global Packaging Equipment for Agricultural Products Market include BW Packaging, Combi Packaging Systems, Concetti Group, General Packer, Haver & Boecker, IMA Group, Krones AG, Landpack, MULTIVAC Group, Paglierani, Premier Tech Systems & Automation, STATEC BINDER, Syntegon Technology, Tetra Pak, and WOLF Packaging. Leading companies in the Packaging Equipment for Agricultural Products Market are focusing on several strategic initiatives to strengthen their market position. Many are prioritizing product innovation by developing modular, IoT-enabled, and energy-efficient systems to cater to the growing demand for smart and automated packaging solutions. Partnerships with local distributors and regional dealers are being expanded to enhance market reach and customer accessibility, especially in emerging economies. Firms are also investing in digital monitoring capabilities and predictive maintenance features to boost operational reliability and reduce downtime.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Operation

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Automation & smart packaging integration

- 3.2.1.2 Diversification into agrochemicals & specialty products

- 3.2.1.3 Sustainability-driven equipment demand

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital costs & ROI pressure

- 3.2.2.2 Supply chain volatility

- 3.2.3 Opportunities

- 3.2.3.1 Smart packaging equipment

- 3.2.3.2 Eco-friendly packaging lines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling & sealing equipment

- 5.2.1 Vertical form-fill-seal (VFFS)

- 5.2.2 Horizontal form-fill-seal (HFFS) systems

- 5.2.3 Others

- 5.3 Sorting & grading equipment

- 5.4 Bagging & packaging lines

- 5.5 Weighing and portioning systems

- 5.6 Palletizing and wrapping equipment

Chapter 6 Market Estimates and Forecast, By Operation, 2021 - 2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Fresh produce packaging

- 7.3 Grain & seed processing

- 7.4 Animal feed & agricultural inputs

- 7.5 Others (eggs, dairy pack, etc.)

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Primary agricultural producers

- 8.3 Agro & food processing facilities

- 8.4 Others (agricultural cooperatives & associations, farmer-owned processing facilities, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 BW Packaging

- 11.2 Combi Packaging Systems

- 11.3 Concetti Group

- 11.4 General Packer

- 11.5 Haver & Boecker

- 11.6 IMA Group

- 11.7 Krones AG

- 11.8 Landpack

- 11.9 MULTIVAC Group

- 11.10 Paglierani

- 11.11 Premier Tech Systems & Automation

- 11.12 STATEC BINDER

- 11.13 Syntegon Technology

- 11.14 Tetra Pak

- 11.15 WOLF Packaging

農業包裝市場:2026-2032年全球市場預測(按包裝材料、包裝形式、應用、最終用戶和分銷管道分類)

農業包裝市場:2026-2032年全球市場預測(按包裝材料、包裝形式、應用、最終用戶和分銷管道分類) 農業包裝市場報告:按材料、產品類型、阻隔性能、應用和地區分類(2026-2034 年)

農業包裝市場報告:按材料、產品類型、阻隔性能、應用和地區分類(2026-2034 年) 農業包裝市場分析及預測(至2035年):依類型、產品類型、材質、應用、技術、最終使用者、功能、形式、實施類型及解決方案分類農業包裝市場分析及預測(至2035年):依類型、產品類型、材質、應用、技術、最終用戶、形式、製程及功能分類

農業包裝市場分析及預測(至2035年):依類型、產品類型、材質、應用、技術、最終使用者、功能、形式、實施類型及解決方案分類農業包裝市場分析及預測(至2035年):依類型、產品類型、材質、應用、技術、最終用戶、形式、製程及功能分類 全球農業包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 農業包裝市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、材料、應用、地區和競爭格局分類,2021-2031年農業化學品包裝市場-2026-2031年預測

農業包裝市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、材料、應用、地區和競爭格局分類,2021-2031年農業化學品包裝市場-2026-2031年預測 農業包裝市場規模、佔有率和成長分析(按材料、產品、應用和地區分類):產業預測(2026-2033 年)全球農業包裝市場:依產品類型、材料類型、應用、區域範圍、預測

農業包裝市場規模、佔有率和成長分析(按材料、產品、應用和地區分類):產業預測(2026-2033 年)全球農業包裝市場:依產品類型、材料類型、應用、區域範圍、預測 農業化學品包裝市場報告:趨勢、預測和競爭分析(至 2031 年)

農業化學品包裝市場報告:趨勢、預測和競爭分析(至 2031 年)