|

市場調查報告書

商品編碼

1876568

碳化矽(SiC)無線電動汽車充電市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Silicon Carbide (SiC) for Wireless EV Charging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

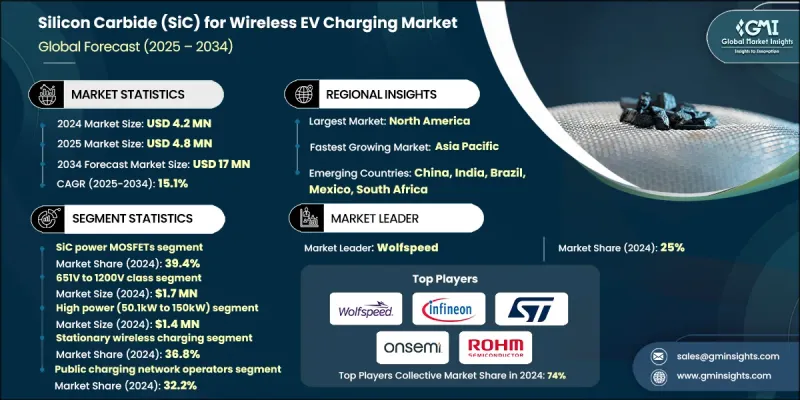

2024 年全球用於電動車無線充電的碳化矽 (SiC) 市場價值為 420 萬美元,預計到 2034 年將以 15.1% 的複合年成長率成長至 1700 萬美元。

全球電動車普及率的激增推動了無線電動汽車充電系統對碳化矽(SiC)的需求,因為消費者和商業車隊越來越傾向於更快、更有效率、更便利的充電解決方案。與傳統的矽元件相比,SiC 裝置具有更高的功率轉換效率和更低的能量損耗,使其非常適合高頻無線充電應用。 SiC 能夠在更高的電壓和溫度下工作,這使得充電器設計更加緊湊輕便,也使其成為下一代電動車充電基礎設施的關鍵推動因素。 SiC 半導體材料和製造流程的進步,例如更高的晶圓品質、更高的生產良率和更最佳化的裝置結構,都提高了效率、熱穩定性和可靠性。 SiC MOSFET 和二極體的創新進一步降低了能量損耗,並支援更小巧、整合度更高、功率密度和開關頻率更高的充電解決方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 420萬美元 |

| 預測值 | 1700萬美元 |

| 複合年成長率 | 15.1% |

預計到2024年,SiC功率MOSFET元件將佔據39.4%的市場佔有率,這主要得益於其卓越的效率、更低的開關損耗和更高的功率密度。這些特性使得無線電動汽車充電器能夠實現更快、更緊湊、散熱效率更高的應用。製造商正致力於提升裝置的可靠性、閘極氧化層穩定性以及封裝性能,以滿足高頻運作的需求。

由於其適用於中高功率無線電動汽車充電,651V至1200V電壓等級的逆變器市場預計在2024年將創造170萬美元的銷售額。這些組件具有卓越的效率和散熱性能,生產商正致力於提升裝置的穩健性、柵極可靠性和車規級封裝整合,同時與電動汽車OEM廠商合作進行逆變器設計和熱建模,以增強產品市場定位。

2024年,北美無線電動汽車充電用碳化矽(SiC)市場佔有率預計將達到34.5%,這主要得益於電動車普及率的提高、政府扶持政策的訂定以及對先進充電基礎設施的投資。環保意識的增強和清潔能源激勵措施的訂定,也推動了對高效SiC技術的需求成長。製造商有機會在城市和郊區擴展無線電動汽車充電網路,透過與公用事業公司建立戰略合作夥伴關係以及投資可擴展的SiC基礎設施,可以更好地滿足日益成長的住宅、商業和公共交通充電需求。

全球電動車無線充電式碳化矽 (SiC) 市場的主要參與者包括英飛凌科技、三菱電機、微芯科技、意法半導體、GeneSiC Semiconductor(Qorvo)、安森美半導體、UnitedSiC(Qorvo)、富士電機、東芝、羅姆半導體、WixelDA. Ltd.、Plugless Power Inc.(Evatran)、高通技術公司(Halo)、InductEV Inc.、ABB Ltd.、羅伯特博世有限公司、豐田汽車公司、西門子公司和大陸集團。這些企業正透過持續的產品創新等策略來鞏固其在電動車無線充電碳化矽 (SiC) 市場的領先地位,專注於高效、耐熱的 SiC MOSFET 和二極體。許多企業正在與電動車原始設備製造商 (OEM) 和公用事業供應商建立策略合作夥伴關係,以將 SiC 解決方案整合到無線充電網路中。對可擴展製造製程、晶圓品質改進和封裝最佳化的投資提高了可靠性並降低了能量損耗。各公司也致力於擴大區域影響力、參與合作研究並展示高性能應用,以獲得競爭優勢。行銷活動著重強調碳化矽解決方案的能源效率和緊湊設計優勢,以吸引住宅和商業客戶,從而鞏固其在蓬勃發展的電動車生態系統中的地位。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 電動車(EV)的普及率不斷提高

- 碳化矽半導體技術的進步

- 政府對永續交通的支持力道不斷加大

- 越來越重視快速且有效率的無線充電

- 產業陷阱與挑戰

- 碳化矽材料和製造成本高昂

- 複雜的製造和設計要求

- 市場機遇

- 全球電動車普及率的提高和政府激勵措施將推動全球對高效碳化矽無線充電解決方案的強勁需求。

- SiC半導體技術的進步將使無線充電器速度更快、體積更小、能源效率更高,從而擴大住宅和商業領域的市場機會。

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

- 技術格局

- 當前趨勢

- 新興技術

- 管道分析

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依碳化矽產品類型分類,2021-2034年

- 主要趨勢

- SiC功率MOSFET

- 碳化矽肖特基勢壘二極體

- SiC功率模組

- SiC 分立元件

第6章:市場估算與預測:依電壓等級分類,2021-2034年

- 主要趨勢

- 最高650V級

- 651V 至 1200V 級

- 1201V 至 1700V 級

- 1700V以上等級

第7章:市場估算與預測:依功率等級分類,2021-2034年

- 主要趨勢

- 低功率(最高 11kW)

- 中等功率(11.1kW 至 50kW)

- 高功率(50.1kW 至 150kW)

- 超高功率(150kW以上)

第8章:市場估算與預測:依應用類型分類,2021-2034年

- 主要趨勢

- 固定式無線充電

- 動態無線充電

- 準動態無線充電

- 其他

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 住宅用戶

- 商業車隊營運商

- 大眾運輸管理局

- 公共充電網路營運商

- 其他

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Wolfspeed

- Infineon Technologies

- STMicroelectronics

- onsemi (ON Semiconductor)

- ROHM Semiconductor

- Mitsubishi Electric

- Fuji Electric

- GeneSiC Semiconductor (Qorvo)

- UnitedSiC (Qorvo)

- Microchip Technology

- Toshiba

- General Electric (GE)

- Littelfuse (IXYS)

- WiTricity Corporation

- InductEV Inc.

- Plugless Power Inc. (Evatran)

- HEVO Inc.

- Electreon Wireless Ltd.

- Qualcomm Technologies (Halo)

- Robert Bosch GmbH

- Continental AG

- Toyota Motor Corporation

- ABB Ltd.

- Siemens AG

- ENRX (Norway)

The Global Silicon Carbide (SiC) for Wireless EV Charging Market was valued at USD 4.2 million in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 17 million by 2034.

The surge in electric vehicle adoption worldwide is driving demand for SiC in wireless EV charging systems, as consumers and commercial fleets increasingly prefer faster, more efficient, and convenient charging solutions. SiC components provide higher power conversion efficiency and lower energy losses than conventional silicon devices, making them highly suitable for high-frequency wireless charging applications. Their ability to function at elevated voltages and temperatures also allows for compact and lightweight charger designs, positioning SiC as a critical enabler of next-generation EV charging infrastructure. Advancements in SiC semiconductor materials and manufacturing such as higher wafer quality, improved production yield, and refined device architecture have enhanced efficiency, thermal stability, and reliability. Innovations in SiC MOSFETs and diodes further reduce energy losses and support smaller, integrated charging solutions with higher power density and switching frequency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Million |

| Forecast Value | $17 Million |

| CAGR | 15.1% |

The SiC power MOSFETs segment held a 39.4% share in 2024, driven by their superior efficiency, lower switching losses, and higher power density. These features enable faster, more compact, and thermally efficient wireless EV chargers. Manufacturers are focusing on improving device reliability, gate oxide stability, and packaging to meet high-frequency operational demands.

The 651V to 1200V class segment generated USD 1.7 million in 2024, owing to its suitability for mid- to high-power wireless EV charging. These components offer exceptional efficiency and thermal performance, and producers are investing in device robustness, gate reliability, and automotive-grade packaging integration, while collaborating with EV OEMs on inverter design and thermal modeling to enhance product positioning.

North America Silicon Carbide (SiC) for Wireless EV Charging Market held a 34.5% share in 2024, driven by rising EV adoption, supportive government initiatives, and investments in advanced charging infrastructure. Environmental awareness and clean energy incentives are increasing demand for high-efficiency SiC technology. Manufacturers have opportunities to expand wireless EV charging networks in both urban and suburban areas, with strategic partnerships with utilities and investments in scalable SiC infrastructure helping to capture growing residential, commercial, and public transit charging demand.

Leading players in the Global Silicon Carbide (SiC) for Wireless EV Charging Market include Infineon Technologies, Mitsubishi Electric, Microchip Technology, STMicroelectronics, GeneSiC Semiconductor (Qorvo), onsemi (ON Semiconductor), UnitedSiC (Qorvo), Fuji Electric, Toshiba, ROHM Semiconductor, WiTricity Corporation, HEVO Inc., Littelfuse (IXYS), General Electric (GE), Electreon Wireless Ltd., Plugless Power Inc. (Evatran), Qualcomm Technologies (Halo), InductEV Inc., ABB Ltd., Robert Bosch GmbH, Toyota Motor Corporation, Siemens AG, and Continental AG. Companies in the Silicon Carbide (SiC) for Wireless EV Charging Market are strengthening their presence through strategies such as continuous product innovation, focusing on high-efficiency, thermally robust SiC MOSFETs and diodes. Many are forming strategic partnerships with EV OEMs and utility providers to integrate SiC solutions into wireless charging networks. Investments in scalable manufacturing processes, wafer quality improvements, and packaging optimization enhance reliability and reduce energy losses. Firms also focus on expanding regional presence, participating in collaborative research, and demonstrating high-performance applications to gain a competitive edge. Marketing efforts highlight the energy efficiency and compact design advantages of SiC-based solutions to attract both residential and commercial clients, solidifying their foothold in the growing EV ecosystem.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Voltage trends

- 2.2.4 Power level trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of electric vehicles (EVs)

- 3.2.1.2 Advancements in SiC semiconductor technology

- 3.2.1.3 Rising government support for sustainable mobility

- 3.2.1.4 Increasing focus on fast and efficient wireless charging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of SiC materials and manufacturing

- 3.2.2.2 Complex fabrication and design requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Rising global EV adoption and government incentives will drive strong demand for high-efficiency SiC-based wireless charging solutions worldwide.

- 3.2.3.2 Technological advancements in SiC semiconductors will enable faster, compact, and energy-efficient wireless chargers, expanding market opportunities across residential and commercial sectors.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By SiC Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 SiC power MOSFETs

- 5.3 SiC schottky barrier diodes

- 5.4 SiC power modules

- 5.5 SiC discrete components

Chapter 6 Market Estimates and Forecast, By Voltage Rating, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Up to 650V class

- 6.3 651V to 1200V class

- 6.4 1201V to 1700V class

- 6.5 Above 1700V class

Chapter 7 Market Estimates and Forecast, By Power Level, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Low power (Up to 11kW)

- 7.3 Medium power (11.1kW to 50kW)

- 7.4 High power (50.1kW to 150kW)

- 7.5 Ultra-high power (Above 150kW)

Chapter 8 Market Estimates and Forecast, By Application Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Stationary wireless charging

- 8.3 Dynamic wireless charging

- 8.4 Quasi-dynamic wireless charging

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Residential users

- 9.3 Commercial fleet operators

- 9.4 Public transit authorities

- 9.5 Public charging network operators

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Wolfspeed

- 11.2 Infineon Technologies

- 11.3 STMicroelectronics

- 11.4 onsemi (ON Semiconductor)

- 11.5 ROHM Semiconductor

- 11.6 Mitsubishi Electric

- 11.7 Fuji Electric

- 11.8 GeneSiC Semiconductor (Qorvo)

- 11.9 UnitedSiC (Qorvo)

- 11.10 Microchip Technology

- 11.11 Toshiba

- 11.12 General Electric (GE)

- 11.13 Littelfuse (IXYS)

- 11.14 WiTricity Corporation

- 11.15 InductEV Inc.

- 11.16 Plugless Power Inc. (Evatran)

- 11.17 HEVO Inc.

- 11.18 Electreon Wireless Ltd.

- 11.19 Qualcomm Technologies (Halo)

- 11.20 Robert Bosch GmbH

- 11.21 Continental AG

- 11.22 Toyota Motor Corporation

- 11.23 ABB Ltd.

- 11.24 Siemens AG

- 11.25 ENRX (Norway)

碳化矽市場:2026-2032年全球市場預測(依產品類型、應用、終端用戶產業及通路分類)

碳化矽市場:2026-2032年全球市場預測(依產品類型、應用、終端用戶產業及通路分類) 碳化矽市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年LED用碳化矽載體市場:依產品類型、技術、額定功率、類型、裝置類型、應用、最終用戶分類,全球預測(2026-2032年)

碳化矽市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年LED用碳化矽載體市場:依產品類型、技術、額定功率、類型、裝置類型、應用、最終用戶分類,全球預測(2026-2032年) 氮化鎵/碳化矽(GaN on SiC)與氮化鎵/矽(GaN on Si)市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶和功能分類

氮化鎵/碳化矽(GaN on SiC)與氮化鎵/矽(GaN on Si)市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶和功能分類 碳化矽:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

碳化矽:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球碳化矽市場規模、佔有率、趨勢和成長分析報告2026-2034年超高純度碳化矽全球市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球碳化矽市場規模、佔有率、趨勢和成長分析報告2026-2034年超高純度碳化矽全球市場規模、佔有率、趨勢和成長分析報告 2026年全球燒結碳化矽市場報告

2026年全球燒結碳化矽市場報告 碳化矽粉末:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)SiC元件市場按應用、元件類型、電壓範圍、終端用戶產業和功率等級分類-2026年至2032年全球預測

碳化矽粉末:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)SiC元件市場按應用、元件類型、電壓範圍、終端用戶產業和功率等級分類-2026年至2032年全球預測