|

市場調查報告書

商品編碼

1876559

個人化癌症疫苗市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Personalized Cancer Vaccine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

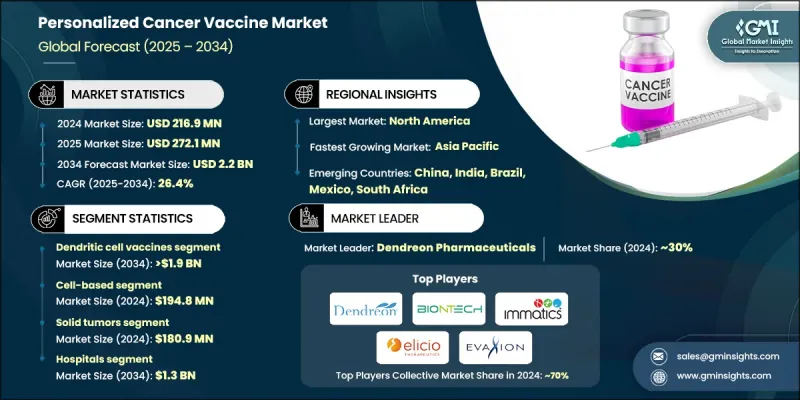

2024 年全球個人化癌症疫苗市場價值為 2.169 億美元,預計到 2034 年將以 26.4% 的複合年成長率成長至 22 億美元。

這一快速成長是由全球癌症發病率的不斷上升以及基因組學、精準醫療和免疫療法的進步共同推動的。新一代定序 (NGS) 和基因組分析使臨床醫生能夠識別腫瘤特異性新抗原,這對於開發患者特異性疫苗至關重要。定序成本的下降使得這些技術在臨床實務中更容易獲得應用。個人化癌症疫苗能夠訓練患者的免疫系統識別並攻擊其特有的癌細胞,為傳統療法提供了一種標靶替代方案。全球癌症病例的增加、人口老化以及醫療保健支出的成長正在推動市場對個人化疫苗的需求,尤其是在北美和亞太地區,這些地區先進的診斷和醫療基礎設施為個人化治療提供了支持。這些疫苗的發展與精準醫療、免疫療法和個人化患者護理的更廣泛趨勢相契合。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.169億美元 |

| 預測值 | 22億美元 |

| 複合年成長率 | 26.4% |

2024年,樹突細胞疫苗市佔率佔85.5%,預計到2034年將達到19億美元。樹突細胞是高效的抗原呈現細胞,能夠誘發強烈的T細胞反應,因此是個人化癌症疫苗的理想選擇。樹突細胞疫苗具有標靶作用,可最大限度地減少脫靶效應,並改善患者預後。

2024年,實體瘤領域創造了1.809億美元的收入。實體瘤是超過一半正在進行的個人化癌症疫苗試驗的核心,包括黑色素瘤、非小細胞肺癌、膠質母細胞瘤和胰臟癌。積極的臨床結果正在加速法規核准並推動疫苗應用,驗證了這些疫苗在實體腫瘤治療中的有效性。

預計到2034年,醫院領域的市場規模將達到13億美元。醫院是疫苗接種、病患監測和臨床試驗的主要場所,因此也是提供個人化癌症疫苗最值得信賴和最高效的管道。醫院在診斷和綜合護理方面發揮著至關重要的作用,使其成為以患者為中心的治療路徑中不可或缺的一部分。

預計到2024年,北美個人化癌症疫苗市佔率將達到46.2%。該地區開展了全球近一半的此類疫苗臨床試驗,主要針對黑色素瘤、非小細胞肺癌和膠質母細胞瘤。在公私合作、聯邦撥款和創投的支持下,各大生技公司正大力投資北美地區的研發工作。

全球個人化癌症疫苗市場的主要參與者包括Immunomic Therapeutics、BioNTech、Elicio Therapeutics、Immatics、Takis Biotech、Candel Therapeutics、VacV Biotherapeutics、Agenus、Moderna、OSE Immunalotherutics、Evax Biotech、Dendmonangenetechs、Dendendelion、Imionet Biotechintra、Dendonanas。這些公司正在實施多種策略以鞏固其市場地位。他們大力投資研發,以提高疫苗效力、最佳化抗原選擇並改進患者特異性配方。與學術機構、醫院和生物技術合作夥伴的策略合作有助於加速臨床驗證和監管批准。各公司正透過合作和授權協議拓展地域版圖,以進入新興市場。此外,他們還利用數位化工具、人工智慧和基因組分析來簡化疫苗設計並縮短生產週期。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 基因組學和測序技術的進步

- 人工智慧與生物資訊學的融合日益加深

- 全球癌症和慢性疾病的盛行率不斷上升

- 精準醫療的趨勢日益增強

- 產業陷阱與挑戰

- 高昂的生產成本

- 複雜的監管環境

- 市場機遇

- 拓展至預防腫瘤學領域

- 臨床試驗項目日益增多

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術格局

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 定價分析

- 臨床試驗分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依疫苗類型分類,2021-2034年

- 主要趨勢

- 樹突細胞疫苗

- 基於mRNA的疫苗

- 基於胜肽的疫苗

- 基於新抗原的疫苗

- 其他疫苗類型

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 基於細胞

- mRNA PCV

- 其他技術

第7章:市場估算與預測:依指示劑分類,2021-2034年

- 主要趨勢

- 實體腫瘤

- 血液系統惡性腫瘤

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 癌症研究中心

- 生物技術和製藥公司

- 其他最終用途

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- BioNTech

- Moderna

- Immatics

- Candel Therapeutics

- Elicio Therapeutics

- Evaxion Biotech

- Immunomic Therapeutics

- Imugene

- Infinitopes

- OSE Immunotherapeutics

- Takis Biotech

- VacV Biotherapeutics

- ImmunityBio

- Agenus

- Dendreon Pharmaceuticals

The Global Personalized Cancer Vaccine Market was valued at USD 216.9 million in 2024 and is estimated to grow at a CAGR of 26.4% to reach USD 2.2 billion by 2034.

This rapid growth is driven by the increasing prevalence of cancer worldwide, coupled with advancements in genomics, precision medicine, and immunotherapy. Next-generation sequencing (NGS) and genomic profiling allow clinicians to identify tumor-specific neoantigens, which are critical for developing patient-specific vaccines. Declining sequencing costs have made these technologies more accessible in clinical practice. Personalized cancer vaccines train a patient's immune system to recognize and attack their unique cancer cells, offering a targeted alternative to conventional therapies. The rise in cancer cases, aging populations, and growing healthcare expenditure globally are fueling demand, particularly in North America and the Asia-Pacific, where advanced diagnostic and healthcare infrastructure support personalized treatments. These vaccines align with the broader shift toward precision medicine, immunotherapy, and individualized patient care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $216.9 Million |

| Forecast Value | $2.2 Billion |

| CAGR | 26.4% |

The dendritic cell vaccine segment accounted for an 85.5% share in 2024 and is expected to reach USD 1.9 billion by 2034. Dendritic cells are highly effective antigen-presenting cells capable of eliciting strong T-cell responses, making them ideal for personalized cancer vaccines. DC vaccines provide targeted action, minimize off-target effects, and enhance patient outcomes.

The solid tumors segment generated USD 180.9 million in 2024. Solid tumors are central to more than half of ongoing personalized cancer vaccine trials, including melanoma, non-small cell lung cancer, glioblastoma, and pancreatic cancer. Positive clinical outcomes are accelerating regulatory approvals and driving adoption, validating the efficacy of these vaccines in solid tumor treatment.

The hospitals segment is expected to reach USD 1.3 billion by 2034. Hospitals are the primary sites for vaccine administration, patient monitoring, and clinical trials, positioning them as the most trusted and efficient channels for delivering personalized cancer vaccines. Their role in diagnostics and integrated care makes them essential in patient-centric treatment pathways.

North America Personalized Cancer Vaccine Market held a 46.2% share in 2024. The region hosts nearly half of the global clinical trials for these vaccines, focusing on melanoma, NSCLC, and glioblastoma. Major biotech companies are heavily investing in research and development in North America, supported by public-private partnerships, federal grants, and venture capital funding.

Prominent players in the Global Personalized Cancer Vaccine Market include Immunomic Therapeutics, BioNTech, Elicio Therapeutics, Immatics, Takis Biotech, Candel Therapeutics, VacV Biotherapeutics, Agenus, Moderna, OSE Immunotherapeutics, Evaxion Biotech, Dendreon Pharmaceuticals, ImmunityBio, Infinitopes, and Imugene. Companies in the Personalized Cancer Vaccine Market are implementing multiple strategies to strengthen their market position. They are investing heavily in research and development to enhance vaccine efficacy, optimize antigen selection, and improve patient-specific formulations. Strategic collaborations with academic institutions, hospitals, and biotechnology partners help accelerate clinical validation and regulatory approvals. Firms are expanding geographic footprints through partnerships and licensing agreements to access emerging markets. Additionally, they are leveraging digital tools, AI, and genomic analytics to streamline vaccine design and reduce production timelines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Technology area trends

- 2.2.4 Indication trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in genomics and sequencing technologies

- 3.2.1.2 Increasing integration of artificial intelligence and bioinformatics

- 3.2.1.3 Growing prevalence of cancer and chronic diseases globally

- 3.2.1.4 Increasing shift towards precision medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Complex regulatory landscape

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into preventive oncology

- 3.2.3.2 Growing pipeline of clinical trials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Clinical trial analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dendritic cell vaccines

- 5.3 mRNA-based vaccines

- 5.4 Peptide-based vaccines

- 5.5 Neoantigen-based vaccines

- 5.6 Other vaccine types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cell-based

- 6.3 mRNA PCV

- 6.4 Other technologies

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Solid tumors

- 7.3 Hematological malignancies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Cancer research centers

- 8.4 Biotechnology and pharmaceutical companies

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BioNTech

- 10.2 Moderna

- 10.3 Immatics

- 10.4 Candel Therapeutics

- 10.5 Elicio Therapeutics

- 10.6 Evaxion Biotech

- 10.7 Immunomic Therapeutics

- 10.8 Imugene

- 10.9 Infinitopes

- 10.10 OSE Immunotherapeutics

- 10.11 Takis Biotech

- 10.12 VacV Biotherapeutics

- 10.13 ImmunityBio

- 10.14 Agenus

- 10.15 Dendreon Pharmaceuticals