|

市場調查報告書

商品編碼

1876554

健康監測汽車座椅市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Health-Monitoring Car Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

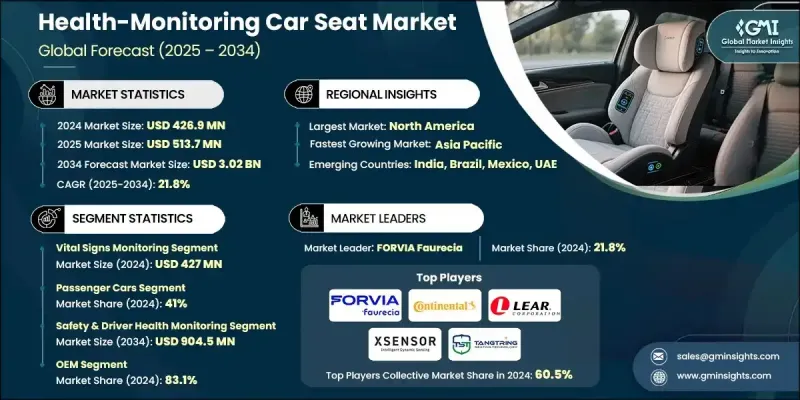

2024 年全球健康監測汽車座椅市場價值為 4.269 億美元,預計到 2034 年將以 21.8% 的複合年成長率成長至 30.2 億美元。

人們日益關注個人健康和福祉,推動了對配備健康監測技術的智慧汽車座椅的需求。消費者越來越重視能夠追蹤生命徵象、疲勞和壓力水平的安全功能,這促使汽車製造商將生物辨識感測器和人工智慧健康系統整合到汽車座椅中。穿戴式電極、感測器和人工智慧技術的進步,使得即時監測乘員的心率、呼吸和姿勢成為可能,從而實現預測性健康警報、個人化舒適體驗和提升駕駛安全性。預計到2030年,該市場規模將從2024年的32.2萬套成長至85.6萬套。隨著汽車互聯性和自動駕駛程度的提高,車內健康監測正成為一項關鍵的差異化優勢,能夠持續追蹤乘員的健康狀況,並支持主動安全措施。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.269億美元 |

| 預測值 | 30.2億美元 |

| 複合年成長率 | 21.8% |

2024年,生命徵象監測市場規模達到4.27億美元,預計到2034年將以21.3%的複合年成長率成長。該市場透過嵌入座椅的電容式心電圖感測器採集心率、血壓和呼吸數據,提供可靠且穩定的訊號。受監管要求和消費者日益增強的駕駛員健康意識的推動,該市場在商用車隊和高階汽車製造商中尤其受歡迎。

到 2024 年,乘用車細分市場將佔據 41% 的佔有率,因為 SUV 和轎車擴大採用人工智慧座椅系統,該系統可以監測生命徵象、姿勢和疲勞程度,提供即時警報和可自訂的舒適度。

預計到2024年,美國健康監測汽車座椅市場將佔據85.4%的佔有率,市場規模達7,280萬美元。美國汽車製造商正引領健康監測技術的整合,尤其是在高階車型領域。關注商用駕駛員健康的監管架構進一步推動了此類系統在車隊營運中的應用,從而提升乘員的安全和福祉。

全球健康監測汽車座椅市場的主要參與者包括 Tangtring Seating Technology、ZF Friedrichshafen AG、偉世通公司、大陸集團、NOVELDA、羅伯特博世有限公司、佛吉亞佛吉亞、李爾、延鋒和 XSENSOR Technology。這些公司正採取多種策略來鞏固市場地位並擴大市場佔有率。他們加大研發投入,以提高感測器精度、人工智慧驅動的分析能力以及座椅舒適度。與汽車製造商和健康技術供應商的合作加速了先進監測系統的創新和整合。各公司致力於透過可自訂和預測性的健康功能實現產品差異化,從而提升安全性和使用者體驗。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預報

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 健康意識日益增強

- 感測器和人工智慧領域的技術進步

- 監管和安全標準

- 互聯自動駕駛汽車的成長

- 消費者對個人化機艙體驗的需求日益成長

- 產業陷阱與挑戰

- 實施成本高昂

- 資料隱私和安全問題

- 市場機遇

- 與穿戴式設備和健康應用程式整合

- 拓展電動車和高階汽車業務

- 人工智慧驅動的預測性健康分析

- 新興市場與都市化

- 成長促進因素

- 成長潛力分析

- 監管環境

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 目前技術

- 新興技術

- 專利分析

- 價格趨勢分析

- 按組件

- 按地區

- 成本分解分析

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來趨勢

- 主要市場趨勢和顛覆性因素

- 成本效益分析與投資報酬率模型

- 總擁有成本分析

- 投資報酬率計算

- 成本削減路線圖

- 按市場區隔分類的價值主張

- 使用者體驗與人因工程

- 人體工學設計考量

- 使用者接受度和採用障礙

- 文化和地域偏好

- 無障礙設計與通用設計

- 未來展望與技術路線圖

- 技術演進路線圖(2025-2035)

- 新興應用及用例

- 與自動駕駛車輛的整合

- 5G 和邊緣運算的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重要新聞和舉措

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依功能分類,2021-2034年

- 主要趨勢

- 生命徵象監測

- 姿勢/座椅壓力監測

- 疲勞/嗜睡偵測

- 生物特徵感測

- 熱舒適度/居住舒適度感測

- 多參數/整合感測

第6章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 低容量性狀

- MCV

- C型肝炎

- 電動車

- 純電動車

- 插電式混合動力汽車

- 燃料電池電動車

第7章:市場估算與預測:依銷售管道分類 2021-2034 年

- 主要趨勢

- OEM

- 售後市場

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 安全與駕駛員健康監測

- 舒適性和人體工學提升

- 健康/預防保健

- 車隊駕駛員監控

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳新銀行

- 新加坡

- 泰國

- 越南

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球參與者

- Continental AG

- Denso Corporation

- FORVIA (Faurecia)

- Lear

- Magna International Inc.

- Robert Bosch GmbH

- Valeo SA

- ZF Friedrichshafen AG

- 區域玩家

- Aptiv PLC

- Autoliv AB

- Gentex Corporation

- HARMAN International (Samsung)

- Hyundai Mobis

- Infineon Technologies AG

- Joyson Safety Systems

- NOVELDA

- Tangtring Seating Technology Inc.

- Visteon Corporation

- XSENSOR Technology

- Yanfeng

- Technology Specialists (Components / Sensors)

- NXP Semiconductors

- Sensirion AG

- STMicroelectronics

- TDK Corporation

- TE Connectivity

- Texas Instruments

- 新興企業/新創公司

- Comfort Motion Global

- ContinUse Biometrics

- Neteera Technologies

The Global Health-Monitoring Car Seat Market was valued at USD 426.9 million in 2024 and is estimated to grow at a CAGR of 21.8% to reach USD 3.02 billion by 2034.

The rising focus on personal health and wellness is driving the demand for smart automotive seats equipped with health-monitoring technologies. Consumers are increasingly prioritizing safety features that track vital signs, fatigue, and stress, encouraging automakers to integrate biometric sensors and AI-enabled wellness systems. Advances in wearable electrodes, sensors, and artificial intelligence now enable real-time monitoring of occupants' heart rate, respiration, and posture, allowing predictive health alerts, personalized comfort, and enhanced driving safety. In terms of units, the market is expected to expand from over 322K in 2024 to 856K by 2030. As vehicles become more connected and autonomous, in-cabin health monitoring is emerging as a key differentiator, enabling continuous tracking of occupant wellbeing and supporting proactive safety measures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $426.9 Million |

| Forecast Value | $3.02 Billion |

| CAGR | 21.8% |

The vital signs monitoring segment generated USD 427 million in 2024 and will grow at a CAGR of 21.3% through 2034. This segment captures heart rate, blood pressure, and respiration via capacitive ECG sensors embedded in the seat, delivering reliable and consistent signals. It is particularly popular among commercial fleets and high-end vehicle manufacturers, driven by regulatory requirements and growing consumer awareness of driver health.

The passenger cars segment held a share of 41% in 2024, as SUVs and sedans increasingly incorporate AI-enabled seat systems that monitor vital signs, posture, and fatigue, providing real-time alerts and customizable comfort.

U.S. Health-Monitoring Car Seat Market held 85.4% share in 2024, valued at USD 72.8 million. US automakers are spearheading the integration of health-monitoring technologies, particularly in premium vehicle segments. Regulatory frameworks focusing on commercial driver health further encourage the adoption of such systems in fleet operations, promoting occupant safety and well-being.

Key players in the Global Health-Monitoring Car Seat Market include Tangtring Seating Technology, ZF Friedrichshafen AG, Visteon Corporation, Continental AG, NOVELDA, Robert Bosch GmbH, FORVIA Faurecia, Lear, Yanfeng, and XSENSOR Technology. Companies in the health-monitoring car seat market are adopting several strategies to strengthen their market presence and expand their foothold. They are investing in research and development to enhance sensor accuracy, AI-driven analytics, and seat comfort features. Collaborations with automakers and health technology providers accelerate innovation and integration of advanced monitoring systems. Firms are focusing on product differentiation through customizable and predictive wellness features that enhance safety and user experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Feature

- 2.2.2 Vehicle

- 2.2.3 Sales channel

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health awareness

- 3.2.1.2 Technological advancements in sensors and ai

- 3.2.1.3 Regulatory and safety standards

- 3.2.1.4 Connected and autonomous vehicle growth

- 3.2.1.5 Increasing consumer demand for personalized in-cabin experience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation cost

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with wearables and health apps

- 3.2.3.2 Expansion in electric and premium vehicles

- 3.2.3.3 Ai-driven predictive health analytics

- 3.2.3.4 Emerging markets and urbanization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

- 3.13 Future trends

- 3.14 Major market trends and disruptions

- 3.15 Cost-benefit analysis & roi models

- 3.15.1 Total cost of ownership analysis

- 3.15.2 Return on investment calculations

- 3.15.3 Cost reduction roadmap(15-20% decline by 2030)

- 3.15.4 Value proposition by market segment

- 3.16 User experience & human factors

- 3.16.1 Ergonomic design considerations

- 3.16.2 User acceptance & adoption barriers

- 3.16.3 Cultural & regional preferences

- 3.16.4 Accessibility & universal design

- 3.17 Future outlook & technology roadmap

- 3.17.1 Technology evolution roadmap (2025-2035)

- 3.17.2 Emerging applications & use cases

- 3.17.3 Integration with autonomous vehicles

- 3.17.4. 5 G & edge computing impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Feature, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Vital signs monitoring

- 5.3 Posture/seat-pressure monitoring

- 5.4 Fatigue/drowsiness detection

- 5.5 Biometric sensing

- 5.6 Thermal / occupant comfort sensing

- 5.7 Multi-parameter / integrated sensing

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

- 6.4 Electric vehicle

- 6.4.1 BEV

- 6.4.2 PHEV

- 6.4.3 FCEV

Chapter 7 Market Estimates & Forecast, By Sales channel 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.1.1 Safety & driver health monitoring

- 8.1.2 Comfort & ergonomics enhancement

- 8.1.3 Wellness / preventive health

- 8.1.4 Fleet driver monitoring

- 8.1.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 Singapore

- 9.4.6 Thailand

- 9.4.7 Vietnam

- 9.4.8 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Continental AG

- 10.1.2 Denso Corporation

- 10.1.3 FORVIA (Faurecia)

- 10.1.4 Lear

- 10.1.5 Magna International Inc.

- 10.1.6 Robert Bosch GmbH

- 10.1.7 Valeo SA

- 10.1.8 ZF Friedrichshafen AG

- 10.2 Regional players

- 10.2.1 Aptiv PLC

- 10.2.2 Autoliv AB

- 10.2.3 Gentex Corporation

- 10.2.4 HARMAN International (Samsung)

- 10.2.5 Hyundai Mobis

- 10.2.6 Infineon Technologies AG

- 10.2.7 Joyson Safety Systems

- 10.2.8 NOVELDA

- 10.2.9 Tangtring Seating Technology Inc.

- 10.2.10 Visteon Corporation

- 10.2.11 XSENSOR Technology

- 10.2.12 Yanfeng

- 10.3 Technology Specialists (Components / Sensors)

- 10.3.1 NXP Semiconductors

- 10.3.2 Sensirion AG

- 10.3.3 STMicroelectronics

- 10.3.4 TDK Corporation

- 10.3.5 TE Connectivity

- 10.3.6 Texas Instruments

- 10.4 Emerging Players / Startups

- 10.4.1 Comfort Motion Global

- 10.4.2 ContinUse Biometrics

- 10.4.3 Neteera Technologies

電動汽車座椅馬達市場:按馬達類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測

電動汽車座椅馬達市場:按馬達類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測 汽車座椅:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

汽車座椅:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球汽車座椅及配件市場報告

2026年全球汽車座椅及配件市場報告 越野車座椅市場成長機會、成長要素、產業趨勢分析及2026年至2035年預測

越野車座椅市場成長機會、成長要素、產業趨勢分析及2026年至2035年預測 汽車座椅市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、技術、銷售管道、地區和競爭格局分類,2021-2031年寵物汽車座椅套市場:依材質、寵物類型、寵物體型、防水等級、價格範圍、應用和銷售管道,全球預測,2026-2032年按座椅類型、安裝技術、材料、銷售管道和分銷管道分類的客製化汽車座椅市場-全球預測,2026-2032年汽車分離式座椅市場(按座椅類型、燃料類型、材料、舒適性功能、車輛類型和分銷管道分類),全球預測,2026-2032年汽車座椅冷卻系統市場:依冷卻技術、座椅位置、冷卻介質、通路和車輛類型分類,全球預測(2026-2032年)汽車座椅海綿市場按泡棉類型、車輛類型、車輛等級、應用、通路和最終用戶分類-2026-2032年全球預測

汽車座椅市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、技術、銷售管道、地區和競爭格局分類,2021-2031年寵物汽車座椅套市場:依材質、寵物類型、寵物體型、防水等級、價格範圍、應用和銷售管道,全球預測,2026-2032年按座椅類型、安裝技術、材料、銷售管道和分銷管道分類的客製化汽車座椅市場-全球預測,2026-2032年汽車分離式座椅市場(按座椅類型、燃料類型、材料、舒適性功能、車輛類型和分銷管道分類),全球預測,2026-2032年汽車座椅冷卻系統市場:依冷卻技術、座椅位置、冷卻介質、通路和車輛類型分類,全球預測(2026-2032年)汽車座椅海綿市場按泡棉類型、車輛類型、車輛等級、應用、通路和最終用戶分類-2026-2032年全球預測