|

市場調查報告書

商品編碼

1936602

越野車座椅市場成長機會、成長要素、產業趨勢分析及2026年至2035年預測Off-Road Vehicle Seats Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

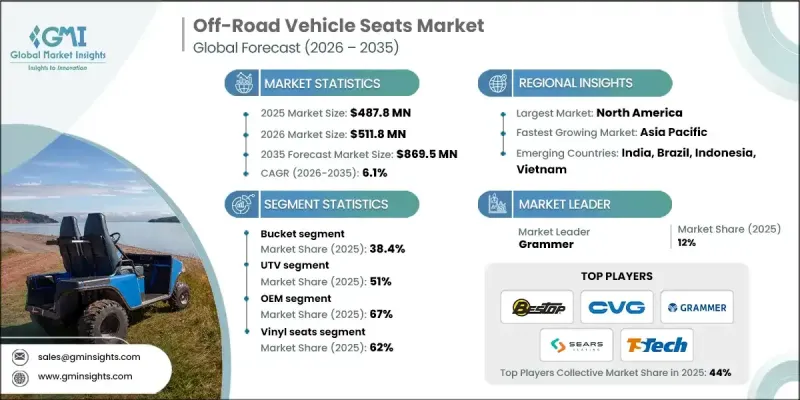

全球越野車座椅市場預計到 2025 年將達到 4.878 億美元,到 2035 年將達到 8.695 億美元,年複合成長率為 6.1%。

該市場涵蓋農業、建築和礦業車輛以及專為惡劣環境設計的休閒越野車的座椅。市場需求深受車輛使用頻率和時長、駕駛舒適度要求以及工業和商業環境中嚴格的職場安全法規的影響。隨著戶外活動的日益普及,休閒車輛,尤其是多功能車輛,持續推動售後市場需求。由於操作人員越來越重視舒適性、支撐性和減震性,製造商正致力於開發耐用且符合人體工學的座椅解決方案,以提高安全性並減少長時間工作帶來的疲勞。可調節和帶襯墊座椅的進步也滿足了不斷發展的職業安全標準和專業期望。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 4.878億美元 |

| 預測金額 | 8.695億美元 |

| 複合年成長率 | 6.1% |

預計到2025年,凹背單人座椅市佔率將達到38.4%,並在2035年之前以5.6%的複合年成長率成長。這類座椅旨在為在崎嶇不平地形上駕駛越野車輛的駕駛提供卓越的側向支撐、穩定性和姿勢控制。桶形座椅主要應用於曳引機、裝載機和多用途車輛,在長時間駕駛過程中,舒適性和安全性至關重要。製造商正致力於改進凹背單人座椅的緩衝性能、可調節性和減震性能,以提高駕駛者的工作效率並減輕疲勞。

預計到2025年,UTV(多用途越野車)市佔率將達到51%,並在2035年之前以7.1%的複合年成長率成長。 UTV座椅的設計旨在滿足各種作業需求,包括運輸、拖曳和人員運輸,特別注重長時間乘坐的舒適性、安全性和人體工學支撐。 UTV在農業、建築和休閒娛樂領域的日益普及,推動了對兼具耐用性、增強緩衝性、可調節配置和整合安全功能(例如安全帶)的座椅的需求。

預計到2025年,美國越野車座椅市場將佔據88%的市場佔有率,市場規模達2.214億美元。農業、建築、採礦和休閒車產業的強勁需求是推動市場成長的主要動力。高運轉率和長時間作業促使人們採用重型、減震且符合人體工學設計的座椅系統,以確保操作人員的安全和舒適。農業工人尤其依賴耐用且支撐良好的座椅來保持生產力,並減少長時間工作帶來的疲勞。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 農業和建築機械化的發展

- 更加重視操作員舒適度與安全標準

- 休閒越野車的使用日益增多

- 產業潛在風險與挑戰

- 先進懸吊座椅高成本

- 暴露於惡劣的工作環境中

- 市場機遇

- 採用懸吊式和氣壓懸吊座椅系統

- 替換和售後市場需求不斷成長

- 針對特定應用需求進行客製化

- 成長潛力分析

- 監管環境

- 北美洲

- 美國職業安全與健康標準與設備標準

- OSHA座椅和操作員安全指南

- 農業和施工機械合規性

- 加拿大機械安全法規

- 歐洲

- 歐盟機械指令和座椅要求

- 操作手冊基於EN標準

- 國家層級的農業機械合規性

- 職場人體工學和振動暴露法規

- 亞太地區

- 中國農業和施工機械法規

- 印度操作員安全與機械標準

- 日本工業設備表指南

- 韓國機械安全合規

- 東協區域設備安全框架

- 拉丁美洲

- 巴西農業機械標準

- 阿根廷設施安全合規性

- 墨西哥工業機械法規

- 區域運營商安全指南

- 中東和非洲

- 阿拉伯聯合大公國設施安全和操作人員指南

- 沙烏地阿拉伯工業機械合規性

- 南非職業安全標準

- 區域設施安全框架

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費基礎

- 出口和進口

- 成本細分分析

- 座椅框架和材料成本

- 緩衝懸掛和內裝成本

- 組裝和品管成本

- 測試和認證費用

- 監理合規成本

- 配送服務及更換費用

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 操作員人體工學與健康影響分析

- 全身振動 (WBV) 和懸吊性能基準測試

- 座椅安全與約束系統整合分析

- 客製化和特定應用座椅設計

- 材料耐久性和生命週期性能

- 電氣化和智慧座椅相容性

- 未來中斷和設計替代風險

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依座位容量分類的市場估算與預測,2022-2035年

- 凹背單人座椅

- 長椅

- 懸掛式座椅

- 折疊式/可調式座椅

第6章 依車輛類型分類的市場估計與預測,2022-2035年

- ATV

- UTV

- 雪上摩托車

- 越野自行車

7. 2022-2035年按分銷管道分類的市場估算與預測

- OEM

- 售後市場

第8章 按材料分類的市場估算與預測,2022-2035年

- 織品座椅

- 乙烯基片材

- 真皮座椅

- 其他

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 個人消費者

- 商業用戶

- 賽車運動和賽車隊

- 其他

第10章 依驅動機制分類的市場估計與預測,2022-2035年

- 電動座椅驅動系統(ESAS)

- 手動座椅調整系統(MSAS)

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 挪威

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第12章:公司簡介

- 世界玩家

- CVG Commercial Vehicle

- Grammer

- ISRI Seats

- Lear

- Milsco

- Recaro Automotive Seating

- TS Tech

- Ultra Seat

- KL Seating

- Knoedler

- 本地製造商

- Bestop

- KAB Seating

- National Seating

- Pilot Seating

- Sears Seating

- UnitedSeats

- 新興企業和利基製造商

- Beard Seats

- Corbeau Seats

- MasterCraft Safety

- OMP Racing

- PRP Seats

- Simpson race products

The Global Off-Road Vehicle Seats Market was valued at USD 487.8 million in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 869.5 million by 2035.

The market caters to seating for agricultural, construction, and mining vehicles, as well as recreational off-road applications designed for rugged environments. Market demand is strongly influenced by the intensity and duration of vehicle usage, operator comfort requirements, and strict workplace safety regulations across industrial and commercial settings. Recreational vehicles, particularly utility vehicles, continue to drive aftermarket demand as the popularity of outdoor activities grows. Operators prioritize comfort, support, and vibration reduction, prompting manufacturers to focus on durable, ergonomic seating solutions that enhance safety and reduce fatigue over long operational hours. Advances in adjustable and cushioned seating are also aligning with evolving occupational safety standards and professional expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $487.8 Million |

| Forecast Value | $869.5 Million |

| CAGR | 6.1% |

The bucket seat segment captured 38.4% of the market in 2025 and is projected to grow at a CAGR of 5.6% through 2035. These seats are engineered to provide superior lateral support, stability, and posture maintenance for operators handling off-road vehicles on rugged or uneven terrain. They are predominantly utilized in tractors, loaders, and utility vehicles, where comfort and safety during prolonged operation are critical. Manufacturers are increasingly focusing on enhancing cushioning, adjustability, and vibration reduction in bucket seats to improve operator productivity and reduce fatigue.

The UTV segment held a 51% share in 2025 and is expected to grow at a CAGR of 7.1% through 2035. UTV seats are specifically designed for long-duration comfort, safety, and ergonomic support, accommodating diverse operational needs such as hauling, towing, and transporting work crews. The growing use of UTVs in agricultural, construction, and recreational applications is driving demand for seats that combine durability with enhanced cushioning, adjustable configurations, and integrated safety features such as seat belts.

US Off-Road Vehicle Seats Market held an 88% share, generating USD 221.4 million in 2025. Market growth is supported by strong demand from the agricultural, construction, mining, and recreational vehicle sectors. High utilization rates and extended operational hours have driven the adoption of robust, vibration-reducing, and ergonomically designed seating systems to protect operators' safety while ensuring comfort. Agricultural operators rely heavily on durable and supportive seats to maintain productivity and reduce fatigue during long working hours.

Key players in the Global Off-Road Vehicle Seats Market include Bestop, CVG Commercial Vehicle, Grammer, ISRI Seats, Lear, Milsco, Recaro Automotive Seating, Sears Seating, TS Tech, and UnitedSeats. Companies in the off-road vehicle seats market are strengthening their presence through continuous innovation in ergonomic and vibration-reducing technologies, expanding their product portfolios for both industrial and recreational vehicles, and investing in advanced materials for durability and comfort. Manufacturers are establishing strategic partnerships with OEMs, focusing on aftermarket solutions to capture recurring demand, and optimizing distribution networks for wider regional penetration. Additionally, companies are leveraging regulatory compliance and certification standards to differentiate products, while offering customizable seating solutions to meet specific end-user requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Seat

- 2.2.3 Vehicle

- 2.2.4 Distribution Channel

- 2.2.5 Material

- 2.2.6 End Use

- 2.2.7 Actuation Mechanism

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in agricultural and construction mechanization

- 3.2.1.3 Rising focus on operator comfort and safety standards

- 3.2.1.4 Expansion of recreational off road vehicle usage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced suspension seats

- 3.2.2.2 Exposure to harsh operating conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of suspension and air ride seating systems

- 3.2.3.2 Rising replacement and aftermarket demand

- 3.2.3.3 Customization for application specific needs

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Occupational Safety and Equipment Standards

- 3.4.1.2 OSHA Seating and Operator Safety Guidelines

- 3.4.1.3 Agricultural and Construction Equipment Compliance

- 3.4.1.4 Canada Machinery Safety Regulations

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Directive and Seating Requirements

- 3.4.2.2 EN Standards for Operator Seats

- 3.4.2.3 Country Level Agricultural Equipment Compliance

- 3.4.2.4 Workplace Ergonomics and Vibration Exposure Rules

- 3.4.3 Asia Pacific

- 3.4.3.1 China Agricultural and Construction Equipment Regulations

- 3.4.3.2 India Operator Safety and Machinery Standards

- 3.4.3.3 Japan Industrial Equipment Seating Guidelines

- 3.4.3.4 South Korea Machinery Safety Compliance

- 3.4.3.5 ASEAN Regional Equipment Safety Frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil Agricultural Machinery Standards

- 3.4.4.2 Argentina Equipment Safety Compliance

- 3.4.4.3 Mexico Industrial Machinery Regulations

- 3.4.4.4 Regional Operator Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Equipment Safety and Operator Guidelines

- 3.4.5.2 Saudi Arabia Industrial Machinery Compliance

- 3.4.5.3 South Africa Occupational Safety Standards

- 3.4.5.4 Regional Equipment Safety Frameworks

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Seat frame and material costs

- 3.10.2 Cushioning suspension and upholstery costs

- 3.10.3 Assembly and quality control costs

- 3.10.4 Testing and certification costs

- 3.10.5 Regulatory compliance costs

- 3.10.6 Distribution service and replacement costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Operator Ergonomics & Health Impact Analysis

- 3.14 Whole Body Vibration (WBV) & Suspension Performance Benchmarking

- 3.15 Seat Safety & Restraint Integration Analysis

- 3.16 Customization & Application-Specific Seat Design

- 3.17 Material Durability & Lifecycle Performance

- 3.18 Electrification & Smart Seat Readiness

- 3.19 Future Disruption & Design Substitution Risks

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Seat, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Bucket seat

- 5.3 Bench seat

- 5.4 Suspension seats

- 5.5 Foldable/Adjustable seats

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 ATV

- 6.3 UTV

- 6.4 Snowmobile

- 6.5 Off-Road Motorcycle

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Fabric seats

- 8.3 Vinyl seats

- 8.4 Leather seats

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Individual consumers

- 9.3 Commercial users

- 9.4 Motorsports and racing teams

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Actuation Mechanism, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 Electric seat actuation system (ESAS)

- 10.3 Manual seat actuation system (MSAS)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Norway

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 CVG Commercial Vehicle

- 12.1.2 Grammer

- 12.1.3 ISRI Seats

- 12.1.4 Lear

- 12.1.5 Milsco

- 12.1.6 Recaro Automotive Seating

- 12.1.7 TS Tech

- 12.1.8 Ultra Seat

- 12.1.9 KL Seating

- 12.1.10 Knoedler

- 12.2 Regional Players

- 12.2.1 Bestop

- 12.2.2 KAB Seating

- 12.2.3 National Seating

- 12.2.4 Pilot Seating

- 12.2.5 Sears Seating

- 12.2.6 UnitedSeats

- 12.3 Emerging Players and Niche Specialists

- 12.3.1 Beard Seats

- 12.3.2 Corbeau Seats

- 12.3.3 MasterCraft Safety

- 12.3.4 OMP Racing

- 12.3.5 PRP Seats

- 12.3.6 Simpson race products

汽車皮革座椅市場:2026-2032年全球市場預測(按材料、價格範圍、座椅覆蓋率、座椅類別、應用和分銷管道分類)汽車座椅通風系統市場:按組件、冷卻能力、安裝類型、控制方式、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測

汽車皮革座椅市場:2026-2032年全球市場預測(按材料、價格範圍、座椅覆蓋率、座椅類別、應用和分銷管道分類)汽車座椅通風系統市場:按組件、冷卻能力、安裝類型、控制方式、應用、最終用戶和銷售管道分類-2026-2032年全球市場預測 2026年全球汽車座椅框架市場報告汽車座椅馬達市場:2026-2032年全球市場預測(按馬達類型、電壓、功能領域、應用、最終用戶和分銷管道分類)電動汽車座椅馬達市場:按馬達類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測

2026年全球汽車座椅框架市場報告汽車座椅馬達市場:2026-2032年全球市場預測(按馬達類型、電壓、功能領域、應用、最終用戶和分銷管道分類)電動汽車座椅馬達市場:按馬達類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測 汽車座椅市場規模、佔有率、趨勢和預測:按材料、座椅類型、車輛類型、車輛動力來源和地區分類,2026-2034年

汽車座椅市場規模、佔有率、趨勢和預測:按材料、座椅類型、車輛類型、車輛動力來源和地區分類,2026-2034年 汽車座椅:市佔率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球汽車座椅及配件市場報告

汽車座椅:市佔率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球汽車座椅及配件市場報告 汽車座椅市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、技術、銷售管道、地區和競爭格局分類,2021-2031年寵物汽車座椅套市場:依材質、寵物類型、寵物體型、防水等級、價格範圍、應用和銷售管道,全球預測,2026-2032年

汽車座椅市場-全球產業規模、佔有率、趨勢、機會和預測:按材料類型、技術、銷售管道、地區和競爭格局分類,2021-2031年寵物汽車座椅套市場:依材質、寵物類型、寵物體型、防水等級、價格範圍、應用和銷售管道,全球預測,2026-2032年