|

市場調查報告書

商品編碼

1876549

胜肽合成試劑市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Peptide Synthesis Reagents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

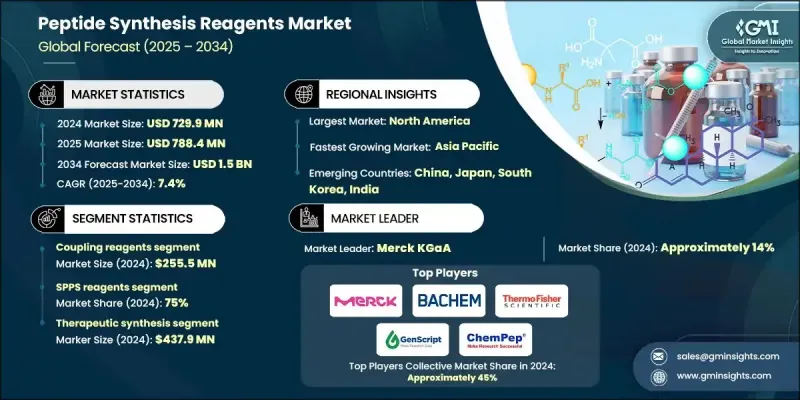

2024 年全球胜肽合成試劑市場價值為 7.299 億美元,預計到 2034 年將以 7.4% 的複合年成長率成長至 15 億美元。

基於Fmoc和碳二亞胺的偶聯試劑需求最為強勁,而脲化合物和混合系統則為更廣泛的市場應用鋪平了道路。肽類藥物的日益普及,加上生物基試劑替代品的出現以及自動化合成研究的大力投入,共同推動了這一成長。針對胜肽類藥物的監管指導,以及精準醫療在製藥、生物技術和診斷領域的日益廣泛應用,正在加速胜肽類藥物的商業化應用。個人化醫療計劃正在將肽類合成的應用拓展到商業規模和先進的治療性藥物生產領域。基於Fmoc和固相合成技術具有高度可擴展性和高效性,能夠支持下一代藥物的開發和生物活性胜肽的生產。創新的試劑配方和與製藥應用的無縫整合,使這些系統成為精準肽類藥物生產的理想選擇。試劑設計的進步如今能夠提供更高的效率、可擴展性和更廣泛的應用,尤其是在特殊藥物生產中。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.299億美元 |

| 預測值 | 15億美元 |

| 複合年成長率 | 7.4% |

混合合成和先進合成領域預計在2025年至2034年間將以7.1%的複合年成長率成長。其成長動力源自於該領域能夠支援技術精湛、合成結構複雜且針對特定應用客製化的產品。與傳統的固相合成技術相比,該領域憑藉連續流化學、匯聚合成和特種酶製劑等優勢,實現了卓越的差異化,從而佔據了高階市場地位。

預計2025年至2034年間,診斷與分析應用領域將以7.4%的複合年成長率成長。該領域對於開發針對分析應用最佳化的複雜生物標記結構產品至關重要。其重要性源自於生物標記胜肽合成、放射性藥物前驅物和特種免疫測定製劑等方面的先進技術要求和顯著差異化優勢,而這些優勢與傳統治療方法相比具有顯著優勢。

預計到2024年,北美胜肽合成試劑市場規模將達到2.674億美元。市場擴張主要得益於政府對藥物研發的大力支持、先進的胜肽合成基礎設施以及產業領導者的存在。北美市場的成長也受到嚴格的安全標準、監管合規以及胜肽合成技術持續創新的推動。精準治療和個人化醫療的需求持續推動下游企業對先進胜肽合成試劑系統的應用。

全球胜肽合成試劑市場的主要參與者包括默克集團(Merck KGaA)、巴赫姆股份公司(Bachem AG)、賽默飛世爾科技(Thermo Fisher Scientific)、金斯瑞生物科技(GenScript Biotech)、ChemPep Inc.、AAPPTec / Advanced ChemTech、CSBio Company、Iris Biotech)、ChemPep Inc.、AAPPTec / Advanced ChemTech、CSBio Company、Iris Biotech)、ChemPep Inc.、AAPPTec / Advanced ChemTech、CSBio Company、Iris Biotech)、ChemPep Inc.、AAPPTec / Advanced ChemTech、CSBio Company、Iris Biotech)、ChemPep Inc.、AAPPTec / Advanced ChemTech、CSBio Company、Iris Biotech)、ChemPep . (Biosynth/vivitide)、Biosynth (vivitide、Pepscan、CRB、Pepceuticals)、AmbioPharm Inc.、Creative Peptides、Peptide Institute, Inc. 和 CEM Corporation。肽合成試劑市場企業採取的關鍵策略包括投資研發,以提高試劑效率、可擴展性以及與自動化合成平台的整合。各公司正在建立策略合作夥伴關係和合作,以擴大地域覆蓋範圍和產品供應。此外,各公司也專注於收購小型企業,以鞏固市場佔有率並獲得創新技術。進入新興市場是抓住新成長機會的首要任務。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 陷阱與挑戰

- 機會

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按產品規格

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼說明:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依試劑產品類型分類,2021-2034年

- 主要趨勢

- 偶聯試劑

- 基於碳二亞胺的

- 基於鏻的

- 鈾基

- 基於亞胺的

- 下一代綠色

- 保護基試劑

- Fmoc試劑及衍生物

- Boc試劑及其衍生物

- 側鏈保護

- 正交系統

- 固體支撐材料

- 聚苯乙烯基樹脂

- 基於聚乙二醇和化學基質

- 特種樹脂

- 可生物分解材料

- 去保護和裂解

- 基本系統

- 酸裂解試劑

- 清掃系統

- 乳汁分泌雞尾酒配方

- 溶劑和反應介質

- 傳統溶劑

- 綠色溶劑替代品

- 離子液體和低共熔晶體

- 水性且生物相容性

- 分析及品管試劑

- 高效液相層析標準品及參考品

- 凱撒試驗和茚三酮

- 質譜標準品

- 純度評估試劑

第6章:市場估計與預測:綜合法,2021-2034年

- 主要趨勢

- SPPS試劑

- Fmoc SPPS系統

- Boc SPPS系統

- 微波 SPPS

- 自動相容

- LPPS試劑

- 溶液相系統

- 碎片凝聚

- 與純化相容

- 混合型及先進型

- 連續流動化學

- 收斂合成

- 酶促連接

- 點擊化學系統

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 治療合成

- 符合GMP標準的生產

- 臨床級(I-III期)

- 長胜肽特化

- 修飾胜肽試劑

- 研發應用

- 高通量篩選

- 文庫合成

- 概念驗證和領先選擇

- 學術研究等級

- 診斷與分析

- 生物標記胜肽合成

- 放射性藥物前驅

- 免疫測定標準

- 特殊應用

- 化妝品胜肽合成

- 食品級及營養保健品級

- 農業胜肽合成

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Merck KGaA

- Bachem AG

- Thermo Fisher Scientific

- GenScript Biotech

- ChemPep Inc.

- AAPPTec / Advanced ChemTech

- CSBio Company

- Iris Biotech GmbH

- GL Biochem (Shanghai) Ltd

- Peptides International (Biosynth/vivitide)

- Biosynth (vivitide, Pepscan, CRB, Pepceuticals)

- AmbioPharm Inc.

- Creative Peptides

- Peptide Institute, Inc.

- CEM Corporation

The Global Peptide Synthesis Reagents Market was valued at USD 729.9 million in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 1.5 billion by 2034.

Fmoc-based and carbodiimide-based coupling reagents are experiencing the strongest demand, while uronium compounds and hybrid systems are paving the way for broader market applications. Rising adoption of peptide drugs, coupled with bio-based reagent alternatives and strong funding for automated synthesis research, drives this growth. Regulatory guidance on peptides, along with the increasing application of precision medicine in pharmaceutical, biotech, and diagnostic sectors, is accelerating commercial adoption. Personalized medicine initiatives are expanding peptide synthesis applications into commercial-scale and advanced therapeutic processing. Fmoc-based and solid-phase synthesis technologies are highly scalable and efficient, enabling next-generation drug development and bioactive peptide production. Innovative reagent formulations and seamless integration for pharmaceutical applications make these systems ideal for precision peptide manufacturing. Advancements in reagent design now offer higher efficiency, scalability, and broader applications in specialty pharmaceutical operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $729.9 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 7.4% |

The hybrid and advanced synthesis segment is expected to grow at a CAGR of 7.1% from 2025 to 2034. Growth is driven by their ability to support technologically sophisticated products with complex synthetic architectures tailored for specialized applications. Their premium positioning reflects superior differentiation through continuous flow chemistry, convergent synthesis, and specialty enzymatic formulations compared to traditional solid-phase techniques.

The diagnostic and analytical application segment is projected to grow at a 7.4% CAGR from 2025 to 2034. This segment is critical for developing products with complex biomarker architectures optimized for analytical applications. Its prominence stems from the advanced technology requirements and exceptional differentiation offered in biomarker peptide synthesis, radiopharmaceutical precursors, and specialty immunoassay formulations relative to conventional therapeutic approaches.

North America Peptide Synthesis Reagents Market reached USD 267.4 million in 2024. Market expansion is fueled by robust government support for pharmaceutical research, advanced peptide synthesis infrastructure, and the presence of key industry players. North American growth is influenced by stringent safety standards, regulatory compliance, and ongoing innovation in peptide synthesis technologies. The demand for precision therapeutics and personalized medicine continues to sustain downstream adoption of advanced peptide synthesis reagent systems.

Leading players in the Global Peptide Synthesis Reagents Market include Merck KGaA, Bachem AG, Thermo Fisher Scientific, GenScript Biotech, ChemPep Inc., AAPPTec / Advanced ChemTech, CSBio Company, Iris Biotech GmbH, GL Biochem (Shanghai) Ltd, Peptides International (Biosynth/vivitide), Biosynth (vivitide, Pepscan, CRB, Pepceuticals), AmbioPharm Inc., Creative Peptides, Peptide Institute, Inc., and CEM Corporation. Key strategies adopted by companies in the Peptide Synthesis Reagents Market include investing in research and development to improve reagent efficiency, scalability, and integration into automated synthesis platforms. Firms are forming strategic partnerships and collaborations to expand geographic reach and product offerings. Companies also focus on acquiring smaller players to consolidate market presence and gain access to innovative technologies. Entry into emerging markets is a priority to capture new growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Reagent product type trends

- 2.2.2 Synthesis method trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product format

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Reagent Product Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Coupling reagents

- 5.2.1 Carbodiimide-based

- 5.2.2 Phosphonium-based

- 5.2.3 Uronium-based

- 5.2.4 Immonium-based

- 5.2.5 Next-gen green

- 5.3 Protecting group reagents

- 5.3.1 Fmoc reagents & derivatives

- 5.3.2 Boc reagents & derivatives

- 5.3.3 Side-chain protecting

- 5.3.4 Orthogonal systems

- 5.4 Solid support materials

- 5.4.1 Polystyrene-based resins

- 5.4.2 Peg-based & chemmatrix

- 5.4.3 Specialty resins

- 5.4.4 Biodegradable materials

- 5.5 Deprotection & cleavage

- 5.5.1 Base systems

- 5.5.2 Acid cleavage reagents

- 5.5.3 Scavenger systems

- 5.5.4 Cleavage cocktail formulations

- 5.6 Solvents & reaction media

- 5.6.1 Traditional solvents

- 5.6.2 Green solvent alternatives

- 5.6.3 Ionic liquids & deep eutectic

- 5.6.4 Aqueous & bio-compatible

- 5.7 Analytical & QC reagents

- 5.7.1 HPLC Standards & reference

- 5.7.2 Kaiser test & ninhydrin

- 5.7.3 Mass spectrometry standards

- 5.7.4 Purity assessment reagents

Chapter 6 Market Estimates and Forecast, By Synthesis Method, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 SPPS Reagents

- 6.2.1 Fmoc SPPS systems

- 6.2.2 Boc SPPS systems

- 6.2.3 Microwave SPPS

- 6.2.4 Automated compatible

- 6.3 LPPS reagents

- 6.3.1 Solution-phase systems

- 6.3.2 Fragment condensation

- 6.3.3 Purification-compatible

- 6.4 Hybrid & advanced

- 6.4.1 Continuous flow chemistry

- 6.4.2 Convergent synthesis

- 6.4.3 Enzymatic ligation

- 6.4.4 Click chemistry systems

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Therapeutic synthesis

- 7.2.1 GMP-grade manufacturing

- 7.2.2 Clinical-grade (phase I-III)

- 7.2.3 Long peptide specialized

- 7.2.4 Modified peptide reagents

- 7.3 R&D applications

- 7.3.1 High-throughput screening

- 7.3.2 Library synthesis

- 7.3.3 Proof-of-concept & lead Opt

- 7.3.4 Academic research grade

- 7.4 Diagnostic & analytical

- 7.4.1 Biomarker peptide synthesis

- 7.4.2 Radiopharmaceutical precursor

- 7.4.3 Immunoassay standards

- 7.5 Specialty applications

- 7.5.1 Cosmetic peptide synthesis

- 7.5.2 Food & nutraceutical grade

- 7.5.3 Agricultural peptide synthesis

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Merck KGaA

- 9.2 Bachem AG

- 9.3 Thermo Fisher Scientific

- 9.4 GenScript Biotech

- 9.5 ChemPep Inc.

- 9.6 AAPPTec / Advanced ChemTech

- 9.7 CSBio Company

- 9.8 Iris Biotech GmbH

- 9.9 GL Biochem (Shanghai) Ltd

- 9.10 Peptides International (Biosynth/vivitide)

- 9.11 Biosynth (vivitide, Pepscan, CRB, Pepceuticals)

- 9.12 AmbioPharm Inc.

- 9.13 Creative Peptides

- 9.14 Peptide Institute, Inc.

- 9.15 CEM Corporation

胜肽合成市場:依產品類型、技術、應用和最終用戶分類-2026-2032年全球市場預測

胜肽合成市場:依產品類型、技術、應用和最終用戶分類-2026-2032年全球市場預測 2026-2030年全球胜肽合成市場

2026-2030年全球胜肽合成市場 胜肽合成市場分析及預測(至2035年):依類型、產品、服務、技術、應用、最終用戶、製程、材料及功能分類

胜肽合成市場分析及預測(至2035年):依類型、產品、服務、技術、應用、最終用戶、製程、材料及功能分類 全球胜肽合成市場規模、佔有率、趨勢和成長分析報告(2026-2034)胜肽合成市場規模、佔有率、成長及全球產業分析:依產品、方法、應用、最終用戶和地區劃分的洞察與預測(2026-2034)標籤胜肽市場:依產品類型、應用、終端用戶產業及通路分類-2026-2032年全球預測

全球胜肽合成市場規模、佔有率、趨勢和成長分析報告(2026-2034)胜肽合成市場規模、佔有率、成長及全球產業分析:依產品、方法、應用、最終用戶和地區劃分的洞察與預測(2026-2034)標籤胜肽市場:依產品類型、應用、終端用戶產業及通路分類-2026-2032年全球預測 胜肽合成市場規模、佔有率和成長分析(按產品/服務、技術、最終用戶和地區分類)—產業預測(2026-2033 年)

胜肽合成市場規模、佔有率和成長分析(按產品/服務、技術、最終用戶和地區分類)—產業預測(2026-2033 年) 全球胜肽合成市場-市場佔有率和排名、總收入和需求預測(2025-2031 年)

全球胜肽合成市場-市場佔有率和排名、總收入和需求預測(2025-2031 年) 2025年全球胜肽合成市場報告

2025年全球胜肽合成市場報告 胜肽合成市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、技術、應用、最終用戶、地區和競爭細分,2020-2030 年)

胜肽合成市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、技術、應用、最終用戶、地區和競爭細分,2020-2030 年)