|

市場調查報告書

商品編碼

1876537

自願性農業碳權市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Voluntary Agriculture Carbon Credit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

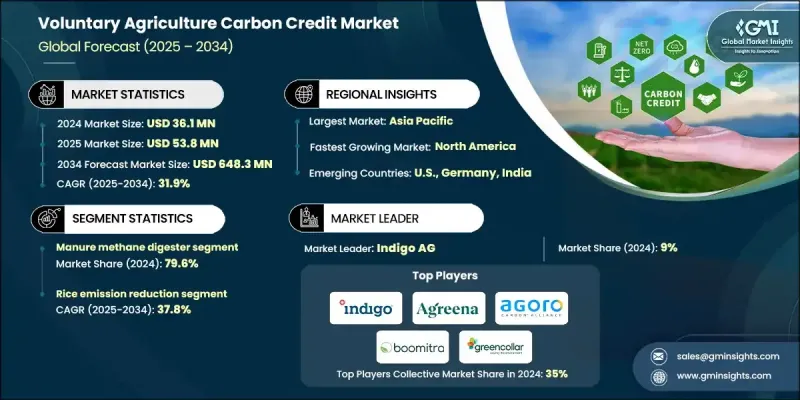

2024 年全球自願性農業碳權市場價值為 3,610 萬美元,預計到 2034 年將以 31.9% 的複合年成長率成長至 6.483 億美元。

企業淨零排放承諾的激增推動了市場成長,因為企業越來越希望抵消其供應鏈產生的範圍3排放。農業碳權額提供了一種可衡量的方式來展現企業的環境責任,同時支持永續農業實踐。從零星購買碳抵銷金額到整合永續發展融資的轉變,已將碳權納入企業投資策略。由企業主導的經核實的農業碳專案進一步創造了巨大的機會。私部門的參與正在重塑市場格局,企業不僅購買碳權額,還設計和管理自己的專案。強調高品質、經核實的碳權有助於規範實踐並增強買家信心。數位化平台和第三方驗證確保了透明度和可追溯性,而簡化的註冊流程和穩定的收入來源使碳權專案對農民越來越有吸引力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3610萬美元 |

| 預測值 | 6.483億美元 |

| 複合年成長率 | 31.9% |

2024年,糞便甲烷消化器市佔率達到79.6%,預計到2034年將以30.6%的複合年成長率成長。成長的主要驅動力是可再生天然氣生產方式的轉變,以及與營養物回收和共消化製程的融合。甲烷捕集和轉化為燃料的強勁市場誘因進一步加速了這些項目在全球的推廣應用。

預計到2034年,水稻減量措施將以37.8%的速度成長,這主要得益於交替乾濕灌溉方式的推廣以及經核證碳權計畫的擴展。透過在生長季期間控制排水期,農民可以顯著降低水稻田的甲烷排放量。這些項目通常整合了高效施肥和永續灌溉技術等措施,從而增強土壤固碳能力並減少一氧化二氮排放,進而擴大碳權的產生範圍。

2024年,美國自願性農業碳權市場創造了690萬美元的收入。該國的企業氣候計劃正將碳權從可選的抵銷手段轉變為策略性金融工具。企業正將農業碳權納入資本配置和永續發展掛鉤的金融機制,尤其針對範圍3排放。這一趨勢正在推動美國市場對經核實的高品質碳權的需求不斷成長。

全球自願性農業碳權市場的主要參與者包括Agoro Carbon Alliance、AgriCapture、Agreena、Boomitra、Carbon Asset Solutions、CarbonSink、CIBO Technologies、Climate Action Reserve、Cultivo、eAgronom、EverCarbon、Green Carbon Inc.、GreenCollar、Indigo Ag、Landkmate、Phak Ag Private Limited。這些公司正採取多種策略來鞏固其市場地位並擴大市場佔有率。他們大力投資於專案開發和驗證系統,以確保高品質、可信賴的信用額度。與農民、技術提供者和企業買家建立策略合作夥伴關係,有助於提高專案的普及率和覆蓋範圍。各公司正在利用數位化平台和可追溯性工具來提高透明度、簡化註冊流程,並確保參與者獲得穩定的收入。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 監管環境

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

- 新興機會與趨勢

- 數位化和物聯網整合

- 新興市場滲透

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 策略舉措

- 競爭性標竿分析

- 戰略儀錶板

- 創新與技術格局

第5章:市場規模及預測:依專案類型分類,2021-2034年

- 主要趨勢

- 糞便甲烷消化器

- 水稻減量

- 永續農業

- 改進的灌溉管理

- 其他

第6章:市場規模及預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 瑞士

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 台灣

- 世界其他地區

第7章:公司簡介

- AgriCapture

- Agoro Carbon Alliance

- Agreena

- Boomitra

- Carbon Asset Solutions

- CarbonSink

- CIBO Technologies

- Climate Action Reserve

- Cultivo

- eAgronom

- EverCarbon

- Green Carbon Inc.

- GreenCollar

- Indigo Ag

- Landbanking Group

- Loam Bio

- Nori

- Pachama

- South Pole

- TerraCarbon

- Varaha ClimateAg Private Limited

The Global Voluntary Agriculture Carbon Credit Market was valued at USD 36.1 million in 2024 and is estimated to grow at a CAGR of 31.9% to reach USD 648.3 million by 2034.

The market's growth is driven by the surge in corporate net-zero commitments, as companies increasingly look to offset their Scope 3 emissions originating from their supply chains. Agriculture-based carbon credits provide a measurable way to showcase environmental responsibility while supporting sustainable farming practices. The transition from occasional carbon offset purchases to integrated sustainability financing has embedded carbon credits into corporate investment strategies. Verified agriculture carbon projects led by companies are further creating significant opportunities. Private sector participation is reshaping the landscape, with organizations not only buying credits but also designing and managing their own programs. Emphasizing high-quality, verified credits standardizes practices and builds buyer confidence. Digital platforms and third-party verification ensure transparency and traceability, while streamlined enrollment and consistent revenue streams make carbon credit programs increasingly attractive to farmers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $36.1 Million |

| Forecast Value | $648.3 Million |

| CAGR | 31.9% |

The manure methane digester segment held 79.6% share in 2024 and is expected to grow at a CAGR of 30.6% through 2034. Growth is driven by the shift toward renewable natural gas production and integration with nutrient recovery and codigestion processes. Strong market incentives for methane capture and conversion into fuel further accelerate the adoption of these projects worldwide.

The rice emission reduction initiatives are anticipated to grow at a rate of 37.8% through 2034, fueled by the adoption of alternate wetting and drying practices combined with the expansion of verified carbon credit programs. By incorporating controlled drainage periods during the growing season, farmers can significantly lower methane emissions from flooded fields. These projects often integrate practices such as efficient fertilizer use and sustainable irrigation techniques, enhancing soil carbon sequestration and reducing nitrous oxide emissions, thereby broadening the scope of carbon credit generation.

U.S. Voluntary Agriculture Carbon Credit Market generated USD 6.9 million in 2024. Corporate climate initiatives in the country are transforming carbon credits from optional offsets into strategic financial instruments. Companies are embedding agriculture-based credits into capital allocation and sustainability-linked financial mechanisms, particularly targeting Scope 3 emissions. This trend is driving heightened demand for verified and high-quality credits in the U.S. market.

Key players in the Global Voluntary Agriculture Carbon Credit Market include Agoro Carbon Alliance, AgriCapture, Agreena, Boomitra, Carbon Asset Solutions, CarbonSink, CIBO Technologies, Climate Action Reserve, Cultivo, eAgronom, EverCarbon, Green Carbon Inc., GreenCollar, Indigo Ag, Landbanking Group, Loam Bio, Nori, Pachama, South Pole, TerraCarbon, and Varaha ClimateAg Private Limited. Companies in the Global Voluntary Agriculture Carbon Credit Market are employing several strategies to strengthen their market presence and expand their foothold. They are investing heavily in project development and verification systems to ensure high-quality, credible credits. Strategic partnerships with farmers, technology providers, and corporate buyers enhance program adoption and reach. Firms are leveraging digital platforms and traceability tools to provide transparency, simplify enrollment, and ensure consistent revenue for participants.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Project type trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Project Type, 2021 - 2034 (USD Million, Million Credit)

- 5.1 Key trends

- 5.2 Manure methane digester

- 5.3 Rice emission reduction

- 5.4 Sustainable agriculture

- 5.5 Improved irrigation management

- 5.6 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, Million Credit)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 UK

- 6.3.2 Germany

- 6.3.3 Switzerland

- 6.3.4 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 Taiwan

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 AgriCapture

- 7.2 Agoro Carbon Alliance

- 7.3 Agreena

- 7.4 Boomitra

- 7.5 Carbon Asset Solutions

- 7.6 CarbonSink

- 7.7 CIBO Technologies

- 7.8 Climate Action Reserve

- 7.9 Cultivo

- 7.10 eAgronom

- 7.11 EverCarbon

- 7.12 Green Carbon Inc.

- 7.13 GreenCollar

- 7.14 Indigo Ag

- 7.15 Landbanking Group

- 7.16 Loam Bio

- 7.17 Nori

- 7.18 Pachama

- 7.19 South Pole

- 7.20 TerraCarbon

- 7.21 Varaha ClimateAg Private Limited

碳抵銷/排碳權市場:按市場類型、信用類型、計劃區域、交付機制和最終用戶分類-2026-2032年全球市場預測

碳抵銷/排碳權市場:按市場類型、信用類型、計劃區域、交付機制和最終用戶分類-2026-2032年全球市場預測 2026年全球農業、林業和土地利用排碳權市場報告排碳權驗證、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、計劃類型、標準、最終用戶和應用分類)

2026年全球農業、林業和土地利用排碳權市場報告排碳權驗證、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、計劃類型、標準、最終用戶和應用分類) 碳農業信貸市場預測至2034年-全球分析(按信貸類型、信貸機制、市場類型、檢驗方法、買方類型、農場規模、收入模式、平台類型、應用和地區分類)

碳農業信貸市場預測至2034年-全球分析(按信貸類型、信貸機制、市場類型、檢驗方法、買方類型、農場規模、收入模式、平台類型、應用和地區分類) 排碳權檢驗與認證市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

排碳權檢驗與認證市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 2026-2030年全球排碳權市場

2026-2030年全球排碳權市場 智慧碳交易平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類

智慧碳交易平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類 全球排碳權檢驗、驗證和認證市場(按類型、應用和地區分類)-預測至2030年

全球排碳權檢驗、驗證和認證市場(按類型、應用和地區分類)-預測至2030年 日本排碳權市場規模、佔有率、趨勢及預測(按類型、計劃類型、最終用途行業和地區分類,2026-2034年)

日本排碳權市場規模、佔有率、趨勢及預測(按類型、計劃類型、最終用途行業和地區分類,2026-2034年) 排碳權市場機會、成長要素、產業趨勢分析及2026年至2035年預測

排碳權市場機會、成長要素、產業趨勢分析及2026年至2035年預測