|

市場調查報告書

商品編碼

1871209

植物性蛋清蛋白分離物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Plant-Based Egg Protein Isolates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

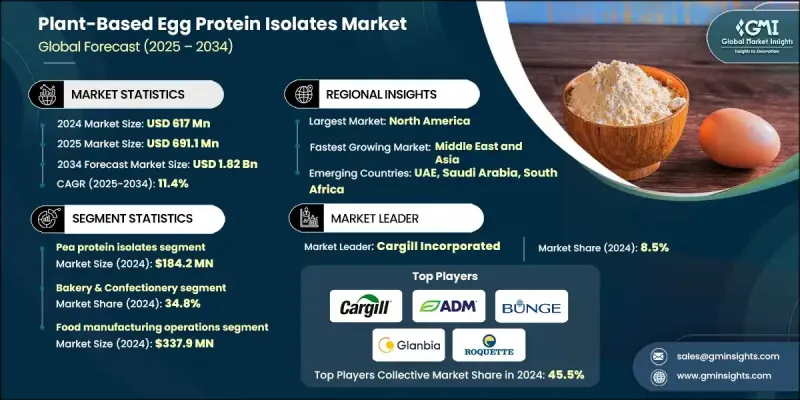

2024 年全球植物性蛋白分離物市場價值為 6.17 億美元,預計到 2034 年將以 11.4% 的複合年成長率成長至 18.2 億美元。

隨著消費者擴大轉向純素、素食和彈性素食飲食,市場正在迅速擴張。以鷹嘴豆、綠豆和藻類等原料製成的植物性蛋蛋白,因其符合倫理、環保且健康,被廣泛接受為傳統雞蛋的替代品。這些產品不含膽固醇,且永續,符合現代消費者注重健康和環境責任的價值。人們對動物福利的日益關注,以及全球對減少食品生產環境足跡的重視,都在推動市場需求。製造商正大力投資先進的加工技術,包括蛋白質工程和人工智慧驅動的最佳化,以複製傳統雞蛋的口感、質地和營養價值。此外,混合蛋白混合物和微膠囊化等創新技術有助於提高產品的穩定性、保存期限和風味保持性,使植物性蛋蛋白對全球消費者和食品製造商的吸引力與日俱增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6.17億美元 |

| 預測值 | 18.2億美元 |

| 複合年成長率 | 11.4% |

2024年,豌豆分離蛋白市場規模預計將達到1.842億美元。在植物性蛋蛋白中,豌豆分離蛋白和大豆分離蛋白憑藉其成本效益、加工穩定性以及與多種食品體系的兼容性,佔據市場主導地位。這些蛋白能夠很好地融入乾粉和液體配方中,從而順利地添加到烘焙混合料、醬汁和即食食品中。豌豆蛋白因其不含致敏物質和中性口味而備受青睞,而大豆蛋白則因其強大的乳化和粘合能力而備受推崇,其功能與傳統雞蛋類似。

2024年,烘焙和糖果產業創造了2.145億美元的收入,佔34.8%的市場。隨著植物蛋白能夠提供烘焙所需的關鍵特性,例如蓬鬆度、結構性和保水性,該行業的需求正在加速成長,這些特性對於生產高品質的純素和無過敏原烘焙食品至關重要。同樣,蛋黃醬和乳化產品生產商也擴大使用植物蛋白,利用其乳化和穩定特性,幫助品牌滿足日益成長的「清潔標籤」趨勢,同時保持理想的質地和貨架穩定性。

2024年,美國植物性蛋蛋白分離物市場規模預估為2.219億美元。北美地區持續引領全球市場成長,消費者越來越重視永續性、無過敏原營養和以植物為主的飲食。在美國,零售和餐飲服務的創新共同推動了市場需求,餐廳和速食連鎖店紛紛將植物性蛋蛋白融入菜單。健康食品替代品的流行趨勢以及富含蛋白質的飲料和烘焙食品的日益普及,正進一步推動該地區市場的成長。

全球植物性蛋白分離物市場的主要參與者包括 Roquette Freres、Axiom Foods Inc.、Beneo GmbH、Aminola BV、Motif FoodWorks、Glanbia PLC、PURIS Holdings LLC、Archer Daniels Midland Company (ADM)、Cargill Incorporated、AGT Food and Ingreds Inc.、Bunge、Coates Inc. SA、煙台雙塔食品有限公司、FUJI Plant Protein Labs、VW Ingredients、Verdient Foods、Laybio Natural Ingredients、ETprotein Co. Ltd.、Organicway Inc.、Burcon NutraScience Corporation 和 Vestkorn Milling AS。領先企業正透過持續創新、合作和以永續發展為中心的策略來鞏固其市場地位。主要生產商正投資先進的研發,以提升植物性蛋白的感官品質和營養成分,使其更接近傳統雞蛋。與食品生產商和科技公司的合作正在幫助拓展產品在烘焙、飲料和簡便食品等領域的應用。各公司也正在擴大永續採購實踐,並實現原料來源多元化,以確保成本效益和供應穩定性。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 消費者對植物性替代品的需求不斷成長

- 食品科技的進步

- 消費者越來越重視健康和保健

- 成長促進因素

- 產業陷阱與挑戰

- 高昂的生產成本限制了市場擴張。

- 關鍵植物原料供應不穩定會擾亂生產。

- 市場機遇

- 對永續蛋白質來源的需求日益成長

- 技術進步促進產品改進

- 消費者越來越傾向於彈性素食飲食

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 植物來源

- 未來市場趨勢

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依植物來源分類,2021-2034年

- 主要趨勢

- 豌豆蛋白分離物

- 大豆分離蛋白

- 綠豆分離蛋白

- 鷹嘴豆/豆類蛋白質分離物

- 混合植物性蛋白質分離物

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 烘焙食品和糖果

- 蛋黃醬和乳液產品

- 飲料和營養應用

- 植物肉和植物乳製品替代品

- 餐飲服務與工業應用

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 食品製造

- 餐飲服務經營

- 零售及消費品

- 營養補充品

第8章:市場估算與預測:依加工技術分類,2021-2034年

- 主要趨勢

- 傳統萃取分離物

- 酵素修飾分離物

- 發酵衍生分離物

- 天然/冷加工分離物

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- AGT Food and Ingredients Inc.

- Aminola BV

- Archer Daniels Midland Company (ADM)

- Axiom Foods Inc.

- Beneo GmbH

- Bunge Limited

- Burcon NutraScience Corporation

- Cargill, Incorporated

- Cosucra Groupe Warcoing SA

- Eat Just, Inc.

- Equinom Ltd.

- ETprotein Co., Ltd.

- FUJI Plant Protein Labs

- Glanbia PLC

- Laybio Natural Ingredients

- Motif FoodWorks

- Organicway Inc.

- PURIS Holdings LLC

- Roquette Freres

- Tate & Lyle

- Verdient Foods

- Vestkorn Milling AS

- VW Ingredients

- Yantai Shuangta Food Co., Ltd

The Global Plant-Based Egg Protein Isolates Market was valued at USD 617 million in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 1.82 Billion by 2034.

The market is expanding rapidly as consumers increasingly shift toward vegan, vegetarian, and flexitarian diets. Plant-based egg proteins, produced from ingredients such as chickpeas, mung beans, and algae, are widely adopted as ethical, eco-friendly, and health-conscious alternatives to conventional eggs. These products provide a cholesterol-free and sustainable option that aligns with modern consumer values focused on wellness and environmental responsibility. Rising awareness of animal welfare, coupled with the global emphasis on reducing the environmental footprint of food production, is fueling demand. Manufacturers are investing heavily in advanced processing technologies, including protein engineering and AI-driven optimization, to replicate the taste, texture, and nutritional quality of traditional eggs. Additionally, innovations like hybrid protein blends and microencapsulation are helping improve product stability, shelf life, and flavor retention, making plant-based egg proteins increasingly appealing to both consumers and food manufacturers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $617 Million |

| Forecast Value | $1.82 Billion |

| CAGR | 11.4% |

The pea protein isolates segment generated USD 184.2 million in 2024. Among plant-based egg proteins, pea and soy isolates lead the market due to their cost-effectiveness, processing stability, and compatibility with diverse food systems. These proteins blend well into both dry and liquid formulations, allowing smooth incorporation into bakery mixes, sauces, and ready-to-eat meals. Pea protein remains preferred for its allergen-free nature and neutral taste, while soy protein is valued for its strong emulsifying and binding capabilities, offering functionality similar to that of conventional eggs.

The bakery and confectionery segment generated USD 214.5 million in 2024 and held a 34.8% share. Demand from this segment is accelerating as plant-based egg proteins provide essential baking characteristics such as aeration, structure, and moisture retention, essential for producing high-quality vegan and allergen-free baked goods. Similarly, mayonnaise and emulsion product manufacturers are increasingly incorporating plant-based proteins for their emulsifying and stabilizing properties, helping brands meet the growing clean-label trend while maintaining desirable texture and shelf stability.

U.S. Plant-Based Egg Protein Isolates Market was valued at USD 221.9 million in 2024. North America continues to lead global adoption as consumers prioritize sustainability, allergen-free nutrition, and plant-forward diets. In the U.S., demand is being driven by both retail and foodservice innovation, with restaurants and quick-service chains integrating plant-based eggs into menus. The trend toward health-driven food alternatives and the growing presence of protein-enriched beverages and baked goods are propelling further growth across the region.

Key players active in the Global Plant-Based Egg Protein Isolates Market include Roquette Freres, Axiom Foods Inc., Beneo GmbH, Aminola BV, Motif FoodWorks, Glanbia PLC, PURIS Holdings LLC, Archer Daniels Midland Company (ADM), Cargill Incorporated, AGT Food and Ingredients Inc., Bunge Limited, Tate & Lyle, Equinom Ltd., Cosucra Groupe Warcoing SA, Yantai Shuangta Food Co. Ltd., FUJI Plant Protein Labs, VW Ingredients, Verdient Foods, Laybio Natural Ingredients, ETprotein Co. Ltd., Organicway Inc., Burcon NutraScience Corporation, and Vestkorn Milling AS. Leading companies are strengthening their presence through continuous innovation, partnerships, and sustainability-focused strategies. Major manufacturers are investing in advanced R&D to enhance the sensory qualities and nutritional profiles of plant-based egg proteins, ensuring closer parity with conventional eggs. Collaborations with food producers and technology firms are helping expand product applications across bakery, beverages, and convenience foods. Firms are also scaling up sustainable sourcing practices and diversifying raw material bases to ensure cost efficiency and supply stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Plant Source

- 2.2.2 Application

- 2.2.3 End use industry

- 2.2.4 Processing technology

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based alternatives

- 3.2.1.2 Advancements in food technology

- 3.2.1.3 Increasing consumer focus on health and wellness

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High production costs limit market expansion

- 3.3.2 Inconsistent supply of key plant ingredients disrupts manufacturing

- 3.4 Market opportunities

- 3.4.1 Growing demand for sustainable protein sources

- 3.4.2 Technological advancements enabling product improvement

- 3.4.3 Rising consumer shift towards flexitarian diets

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By plant source

- 3.11 Future market trends

- 3.12 Patent landscape

- 3.13 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.13.1 Major importing countries

- 3.13.2 Major exporting countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.15 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Plant Source, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pea protein isolates

- 5.3 Soy protein isolates

- 5.4 Mung bean protein isolates

- 5.5 Chickpea/legume protein isolates

- 5.6 Blended plant protein isolates

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Bakery & confectionery

- 6.2 Mayonnaise & emulsion products

- 6.3 Beverage & nutrition applications

- 6.4 Plant-based meat & dairy alternatives

- 6.5 Foodservice & industrial applications

Chapter 7 Market Estimates and Forecast, By End use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food manufacturing

- 7.3 Foodservice operations

- 7.4 Retail & consumer products

- 7.5 Nutritional supplements

Chapter 8 Market Estimates and Forecast, By Processing Technology, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Conventional extraction isolates

- 8.3 Enzymatically modified isolates

- 8.4 Fermentation-derived isolates

- 8.5 Native/cold-processed isolates

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGT Food and Ingredients Inc.

- 10.2 Aminola BV

- 10.3 Archer Daniels Midland Company (ADM)

- 10.4 Axiom Foods Inc.

- 10.5 Beneo GmbH

- 10.6 Bunge Limited

- 10.7 Burcon NutraScience Corporation

- 10.8 Cargill, Incorporated

- 10.9 Cosucra Groupe Warcoing SA

- 10.10 Eat Just, Inc.

- 10.11 Equinom Ltd.

- 10.12 ETprotein Co., Ltd.

- 10.13 FUJI Plant Protein Labs

- 10.14 Glanbia PLC

- 10.15 Laybio Natural Ingredients

- 10.16 Motif FoodWorks

- 10.17 Organicway Inc.

- 10.18 PURIS Holdings LLC

- 10.19 Roquette Freres

- 10.20 Tate & Lyle

- 10.21 Verdient Foods

- 10.22 Vestkorn Milling AS

- 10.23 VW Ingredients

- 10.24 Yantai Shuangta Food Co., Ltd

動物性蛋白質補充劑市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、產品、通路、應用、地區和競爭對手分類,2021-2031年

動物性蛋白質補充劑市場-全球產業規模、佔有率、趨勢、機會、預測:按原料、產品、通路、應用、地區和競爭對手分類,2021-2031年 植物來源蛋白質補充劑市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

植物來源蛋白質補充劑市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 植物蛋白補充劑市場:依類型、形式、應用、分銷管道和地區劃分 - 全球預測至 2036 年全球動物性蛋白質補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球植物蛋白補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球蛋白質補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)蛋白質飲品市場-全球產業規模、佔有率、趨勢、機會及預測(依包裝類型、產品功效、通路、地區及競爭格局分類,2021-2031年)

植物蛋白補充劑市場:依類型、形式、應用、分銷管道和地區劃分 - 全球預測至 2036 年全球動物性蛋白質補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球植物蛋白補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球蛋白質補充劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)蛋白質飲品市場-全球產業規模、佔有率、趨勢、機會及預測(依包裝類型、產品功效、通路、地區及競爭格局分類,2021-2031年) 植物蛋白補充劑市場規模、佔有率和成長分析(按來源、產品、通路、用途、形式、特性和地區分類)-2026-2033年產業預測

植物蛋白補充劑市場規模、佔有率和成長分析(按來源、產品、通路、用途、形式、特性和地區分類)-2026-2033年產業預測 蛋白質補充劑市場植物蛋白補充劑市場-全球產業規模、佔有率、趨勢、機會及預測,依原料、產品、應用、配銷通路、地區及競爭細分,2020-2030 年預測

蛋白質補充劑市場植物蛋白補充劑市場-全球產業規模、佔有率、趨勢、機會及預測,依原料、產品、應用、配銷通路、地區及競爭細分,2020-2030 年預測