|

市場調查報告書

商品編碼

1871135

生物分解電子產品包裝市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Biodegradable Electronics for Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

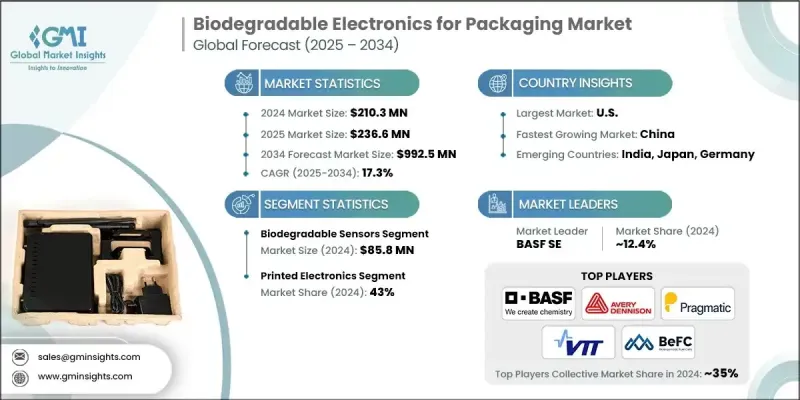

2024 年全球可生物分解電子產品包裝市場價值為 2.103 億美元,預計到 2034 年將以 17.3% 的複合年成長率成長至 9.925 億美元。

該市場代表環保材料、先進電子技術和永續發展驅動創新的突破性融合,其發展動力源於嚴格的監管要求和企業減少環境影響的承諾。可生物分解電子產品採用有機半導體、生物基材和瞬態元件,這些材料在使用壽命結束後可自然分解,從而有效應對包裝中日益嚴重的電子垃圾問題。絲蛋白、纖維素薄膜和有機光伏電池等核心材料可在數週至數月內生物分解,同時保持其功能性。該市場擁有一個充滿活力的生態系統,由新創公司、材料公司、電子產品製造商和包裝公司組成,它們跨領域合作。新興技術路徑包括可根據環境條件調整性能和分解時間的自組裝系統,展現了智慧、永續包裝解決方案的巨大潛力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.103億美元 |

| 預測值 | 9.925億美元 |

| 複合年成長率 | 17.3% |

2024年,可生物分解感測器市場規模達到8,580萬美元,預計到2034年將以17.3%的複合年成長率成長。這些感測器被廣泛應用於各行各業,用於監測易腐爛和敏感商品的溫度、濕度、新鮮度和污染情況等。由於其使用後可自然分解,無需收集或回收,因此非常適合一次性包裝,並使其成為可生物分解電子產品生態系統中最具商業化規模的組件。

預計到2024年,印刷電子產品市場規模將達到9,030萬美元,佔市場佔有率的43%。印刷電子產品與可生物分解基材結合使用時,可提供經濟高效且可擴展的解決方案。噴墨、絲網或凹版印刷等技術使製造商能夠直接在纖維素薄膜等可堆肥的軟性材料上生產電路,從而降低組裝複雜性並減少材料浪費。 2024年,印刷電子產品因其與高通量生產的兼容性以及滿足日益成長的永續包裝解決方案需求,成為優先發展領域。

2024年美國可生物分解包裝電子產品市場規模為3,660萬美元,預計2025年至2034年將以18.1%的複合年成長率成長。美國強勁的需求主要得益於各項旨在促進永續材料管理和減少包裝廢棄物的措施。由於回收率停滯不前且垃圾掩埋量居高不下,監管策略鼓勵採用可堆肥和可回收的包裝解決方案,包括整合電子產品。可生物分解的感測器和RFID標籤有助於減少對環境的影響,同時增強包裝功能,從而符合國家永續發展目標。

用於包裝的生物分解電子產品市場的主要參與者包括BeFC、斯道拉恩索、艾利丹尼森公司、大日本印刷株式會社、LG化學、英飛凌科技與Jiva Materials、PulpaTronics、漢高公司、EcoCortec、巴斯夫公司、PragmatIC Semiconductor、VTT技術研究中心、Emed Electronics Ltd.這些公司正採用創新驅動和協作策略來鞏固其市場地位。他們大力投資研發,以開發先進的有機半導體、生物分解基材和自分解電子系統。與包裝公司和電子產品製造商的合作有助於整合整個供應鏈的解決方案。各公司專注於可擴展的製造技術,例如印刷電子技術,以最佳化成本效益和產量。永續性認證和遵守環境法規是他們優先考慮的事項,以提升信譽和市場認可。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 2024年定價分析

- 按區域和組件

- 原料成本

- 未來市場趨勢

- 風險評估與緩解

- 監理合規風險

- 材料約束影響分析

- 技術轉型風險

- 價格波動和成本上漲風險

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 可生物分解感測器

- 可生物分解的RFID/NFC標籤

- 可生物分解印刷電子產品

- 可生物分解的能源

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 印刷電子

- 有機電子整合

- 混合無機-有機體系

第7章:市場估計與預測:依材料分類,2021-2034年

- 主要趨勢

- 聚合物基材

- 導電材料

- 封裝材料

- 功能材料

第8章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 食品和飲料

- 醫藥和醫療保健

- 消費品

- 電子商務與物流

第9章:市場估算與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 直銷

- 間接銷售

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- Avery Dennison Corporation

- BASF SE

- BeFC

- Dai Nippon Printing

- Eastman Chemical Company

- EcoCortec

- Empa

- Henkel AG

- Infineon Technologies & Jiva Materials

- LG Chem

- PragmatIC Semiconductor

- Printed Electronics Ltd

- PulpaTronics

- Stora Enso

- VTT Technical Research

The Global Biodegradable Electronics for Packaging Market was valued at USD 210.3 million in 2024 and is estimated to grow at a CAGR of 17.3% to reach USD 992.5 million by 2034.

The market represents a groundbreaking fusion of eco-friendly materials, advanced electronics, and sustainability-driven innovation, fueled by stringent regulatory mandates and corporate commitments to reduce environmental impact. Biodegradable electronics utilize organic semiconductors, bio-based substrates, and transient components that naturally decompose after their operational life, tackling the mounting challenge of electronic waste in packaging. Core materials such as silk proteins, cellulose-based films, and organic photovoltaic cells retain functionality while biodegrading within weeks to months. The market features a dynamic ecosystem of startups, materials firms, electronics manufacturers, and packaging companies collaborating across sectors. Emerging technological pathways include self-assembling systems that adapt performance and degradation timing based on environmental conditions, showcasing the potential of intelligent, sustainable packaging solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $210.3 Million |

| Forecast Value | $992.5 Million |

| CAGR | 17.3% |

In 2024, the biodegradable sensors segment generated USD 85.8 million and is expected to grow at a CAGR of 17.3% through 2034. These sensors are widely adopted across industries for monitoring conditions like temperature, humidity, freshness, and contamination in perishable and sensitive goods. Their ability to naturally degrade after use eliminates the need for collection or recycling, making them ideal for single-use packaging and positioning them as the most commercially scalable component of the biodegradable electronics ecosystem.

The printed electronics segment reached USD 90.3 million, representing a 43% share in 2024. Printed electronics provide cost-effective and scalable solutions when integrated with biodegradable substrates. Techniques such as inkjet, screen, or gravure printing allow manufacturers to directly produce circuits on compostable, flexible materials like cellulose films, reducing assembly complexity and material waste. In 2024, printed electronics were prioritized for their compatibility with high-throughput production while meeting the growing demand for sustainable packaging solutions.

U.S. Biodegradable Electronics for Packaging Market was valued at USD 36.6 million in 2024 and is anticipated to grow at a CAGR of 18.1% from 2025 to 2034. The strong U.S. demand is driven by initiatives promoting sustainable materials management and reducing packaging waste. With stagnant recycling rates and high landfill contributions, regulatory strategies encourage the adoption of compostable and recyclable packaging solutions, including integrated electronics. Biodegradable sensors and RFID tags help reduce environmental impact while enhancing packaging functionality, aligning with national sustainability goals.

Key players in the Biodegradable Electronics for Packaging Market include BeFC, Stora Enso, Avery Dennison Corporation, Dai Nippon Printing, LG Chem, Infineon Technologies & Jiva Materials, PulpaTronics, Henkel AG, EcoCortec, BASF SE, PragmatIC Semiconductor, VTT Technical Research, Printed Electronics Ltd, Eastman Chemical Company, and Empa. Companies in the Biodegradable Electronics for Packaging Market are employing innovation-driven and collaborative strategies to strengthen their market position. They are investing heavily in R&D to develop advanced organic semiconductors, biodegradable substrates, and self-degrading electronic systems. Partnerships with packaging firms and electronics manufacturers facilitate integration of solutions across supply chains. Firms focus on scalable manufacturing techniques like printed electronics to optimize cost-efficiency and throughput. Sustainability certifications and compliance with environmental regulations are prioritized to enhance credibility and market acceptance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Technology trends

- 2.2.3 Material trends

- 2.2.4 End Use Industry trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.5 Strategic recommendations

- 2.5.1 Supply chain diversification strategy

- 2.5.2 Product portfolio enhancement

- 2.5.3 Partnership and alliance opportunities

- 2.5.4 Cost management and pricing strategy

- 2.6 Decision framework

- 2.6.1 Investment priority matrix

- 2.6.2 Risk-adjusted ROI analysis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.4.1 By region and component

- 3.4.2 Raw material cost

- 3.5 Future market trends

- 3.6 Risk assessment and mitigation

- 3.6.1 Regulatory compliance risks

- 3.6.2 Material constraint impact analysis

- 3.6.3 Technology transition risks

- 3.6.4 Pricing volatility and cost escalation risks

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Biodegradable sensors

- 5.3 Biodegradable RFID/NFC tags

- 5.4 Biodegradable printed electronics

- 5.5 Biodegradable power sources

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Printed electronics

- 6.3 Organic electronics integration

- 6.4 Hybrid inorganic-organic systems

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Polymer substrate materials

- 7.3 Conductive materials

- 7.4 Encapsulation materials

- 7.5 Functional materials

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Food and beverages

- 8.3 Pharmaceutical and healthcare

- 8.4 Consumer goods

- 8.5 E-commerce & logistics

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 U.K.

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Avery Dennison Corporation

- 11.2 BASF SE

- 11.3 BeFC

- 11.4 Dai Nippon Printing

- 11.5 Eastman Chemical Company

- 11.6 EcoCortec

- 11.7 Empa

- 11.8 Henkel AG

- 11.9 Infineon Technologies & Jiva Materials

- 11.10 LG Chem

- 11.11 PragmatIC Semiconductor

- 11.12 Printed Electronics Ltd

- 11.13 PulpaTronics

- 11.14 Stora Enso

- 11.15 VTT Technical Research

生物分解電子產品市場:全球市場按產品類型、技術、材料、應用和最終用戶分類的預測——2026-2032年電子體積校正裝置市場:2026-2032年全球市場預測(依產品類型、技術、應用、最終用戶、安裝方式及功能分類)

生物分解電子產品市場:全球市場按產品類型、技術、材料、應用和最終用戶分類的預測——2026-2032年電子體積校正裝置市場:2026-2032年全球市場預測(依產品類型、技術、應用、最終用戶、安裝方式及功能分類) 生物可分解電子感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、製程、最終用戶、功能、安裝模式

生物可分解電子感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、製程、最終用戶、功能、安裝模式 2026年全球B2B電子交易市場報告永續半導體代工解決方案市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、材料類型、製程、最終用戶和解決方案分類生物分解電子產品市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類生物可分解感測器陣列市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類2026年全球小型光譜儀市場報告2026年全球小型電子產品市場報告

2026年全球B2B電子交易市場報告永續半導體代工解決方案市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、材料類型、製程、最終用戶和解決方案分類生物分解電子產品市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類生物可分解感測器陣列市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類2026年全球小型光譜儀市場報告2026年全球小型電子產品市場報告 永續通訊網路市場預測至2032年:按組件、網路類型、永續性重點、最終用戶和地區分類的全球分析

永續通訊網路市場預測至2032年:按組件、網路類型、永續性重點、最終用戶和地區分類的全球分析