|

市場調查報告書

商品編碼

1858963

人工智慧在藥物發現領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Artificial Intelligence in Drug Discovery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

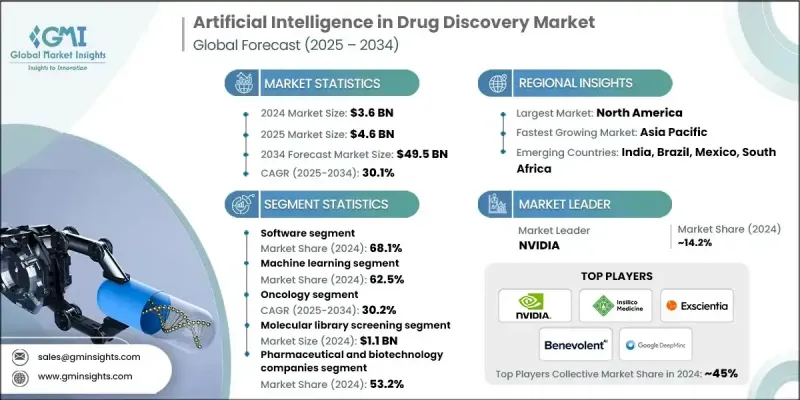

2024 年全球人工智慧藥物發現市場價值為 36 億美元,預計到 2034 年將以 30.1% 的複合年成長率成長至 495 億美元。

這一非凡的成長是由複雜慢性疾病發病率的上升以及製藥公司對利用人工智慧驅動平台簡化藥物研發流程日益濃厚的興趣共同推動的。對更快、更精準的藥物發現流程的需求正促使生物技術公司和研究機構將深度學習和預測分析等先進技術整合到其研發工作流程中。此外,資料整合的持續創新、不斷完善的數位基礎設施以及利害關係人意識的提高也加速了這些技術的應用。人工智慧新創公司與製藥企業之間日益密切的合作,尤其是在技術先進的地區,正在重塑治療藥物的發現和開發方式,為整個醫療保健生態系統開闢了新的可能性。人工智慧在藥物發現領域的作用在於利用自然語言處理、生成演算法和深度學習工具等尖端技術來增強標靶驗證、最佳化先導化合物並支援高效的臨床試驗計劃。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 36億美元 |

| 預測值 | 495億美元 |

| 複合年成長率 | 30.1% |

到了2024年,軟體領域佔68.1%的市場。這一主導地位主要歸功於其在早期藥物研發階段(例如化合物篩選和構效關係預測)的廣泛應用。基於軟體的人工智慧工具如今已成為實現自動化、提高準確性和可擴展性的關鍵,滿足了製藥公司對高效研發工作流程日益成長的需求。自然語言處理(NLP)和神經網路等核心技術的快速發展,正持續拓展軟體在精準醫療領域的應用範圍。

由於機器學習在藥物研發的各個階段都具有廣泛的應用前景,預計到2024年,其市佔率將達到62.5%。該領域涵蓋監督學習和非監督學習模型以及其他機器學習演算法。雲端運算技術的進步和開源框架的普及,使得模型訓練和部署更加靈活、快速且可擴展。製藥巨頭與人工智慧公司之間的持續合作,不斷激發模型設計的創新,並加速預測工具和即時分析技術在藥物研發流程中的應用。

2024年,北美人工智慧藥物研發市場預計將佔據47.6%的佔有率,這主要得益於強勁的研發投入、廣泛的數位基礎設施以及有利於人工智慧整合的監管框架。政府支持的措施和數位療法監管政策的明朗化也推動了市場成長。美國和加拿大的科技公司與製藥公司之間的重要合作,正在推動先進藥物研發解決方案的開發,並深化人工智慧平台在該地區的業務佈局。

全球人工智慧藥物研發市場的主要參與者包括Exscientia、BenevolentAI、Orakl Oncology、AVAYL、Atomwise、Aevai Health、Cyclica、Examol、IBM Corporation、NVIDIA Corporation、Microsoft、Insilico Medicine、Deep Genomics、DenovAI Biotech、NVIDIA Corporation、Microsoft、Insilico Medicine、Deep Genomics. Therapeutics、Helical、Google(DeepMind)和Deargen。為了在全球人工智慧藥物研發市場中保持競爭優勢,各公司正專注於技術創新、策略合作和數據驅動的產品開發。領先企業正在投資開發專有的人工智慧演算法,以提高標靶識別、分子生成和臨床成功率。生物技術新創公司與製藥巨頭之間的合作日益普遍,從而能夠獲取大型資料集、領域知識和可擴展的計算資源。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 每個階段的價值增加

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 複雜慢性疾病盛行率不斷上升

- 醫療保健領域的數據爆炸和數位化

- 人工智慧演算法和運算能力的進步

- 科技公司與製藥公司日益密切的合作

- 產業陷阱與挑戰

- 數據品質和整合問題

- 監理和倫理問題

- 市場機遇

- 個性化和精準醫療的擴展

- 生成式人工智慧在分子設計中的興起

- 成長促進因素

- 成長潛力分析

- 監管環境

- 未來市場趨勢

- 技術格局

- 目前技術

- 新興技術

- 專利分析

- 投資和融資環境

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 軟體

- 現場

- 基於雲端的

- 服務

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 機器學習

- 深度學習

- 監督式學習

- 無監督學習

- 其他機器學習技術

- 其他技術

第7章:市場估算與預測:依應用類型分類,2021-2034年

- 主要趨勢

- 分子庫篩選

- 目標識別

- 藥物最佳化和再利用

- 從頭開始的藥物設計

- 臨床前試驗

- 其他應用

第8章:市場估計與預測:依治療領域分類,2021-2034年

- 主要趨勢

- 腫瘤學

- 神經退化性疾病

- 發炎

- 傳染病

- 代謝性疾病

- 罕見疾病

- 心血管疾病

- 其他治療領域

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 製藥和生物技術公司

- 合約研究組織(CRO)

- 其他用途

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 9Bio Therapeutics

- Aevai Health

- Atomwise

- Aureka Biotechnologies

- AVAYL

- BenevolentAI

- chAIron

- Cyclica

- Deargen

- Deep Genomics

- DenovAI Biotech

- Examol

- Exscientia

- Google (DeepMind)

- Helical

- IBM Corporation

- Insilico Medicine

- LinkGevity

- Microsoft

- NVIDIA Corporation

- Orakl Oncology

The Global Artificial Intelligence in Drug Discovery Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 30.1% to reach USD 49.5 billion by 2034.

This exceptional growth is being driven by the rising incidence of complex and chronic health conditions, combined with increasing interest from pharmaceutical companies in streamlining the drug development process using AI-driven platforms. The demand for faster, more accurate discovery processes is pushing biotech firms and research institutions to integrate advanced technologies like deep learning and predictive analytics into their R&D workflows. Additionally, ongoing innovation in data integration, growing digital infrastructure, and greater awareness among stakeholders are accelerating adoption. Expanding collaboration between AI startups and pharmaceutical manufacturers, particularly in technologically advanced regions, is reshaping how therapeutics are identified and developed, opening new possibilities across the healthcare ecosystem. AI's role in the drug discovery space involves using sophisticated technologies such as natural language processing, generative algorithms, and deep learning tools to enhance target validation, optimize lead compounds, and support efficient clinical trial planning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $49.5 Billion |

| CAGR | 30.1% |

The software segment held 68.1% share in 2024. This dominance is primarily due to widespread adoption during early drug development stages such as compound screening and structure-activity predictions. Software-based AI tools are now integral in providing automation, accuracy, and scalability, meeting the growing demand among pharma companies for efficient R&D workflows. Rapid advancements in core technologies like NLP and neural networks are pushing the boundaries of what software can deliver in precision medicine.

The machine learning segment held a 62.5% share in 2024, owing to its extensive utility across various stages of drug discovery. This segment encompasses supervised and unsupervised learning models along with other ML algorithms. Cloud computing improvements and the availability of open-source frameworks are enabling more flexible, fast, and scalable model training and deployment. Ongoing collaborations between pharmaceutical giants and AI-focused firms continue to spark innovation in model design and accelerate the development of predictive tools and real-time analytics across discovery pipelines.

North America Artificial Intelligence in Drug Discovery Market held 47.6% share in 2024, propelled by strong R&D investments, broad digital infrastructure, and favorable regulatory frameworks supporting AI integration. Government-backed initiatives and regulatory clarity around digital therapeutics are encouraging market growth. Major collaborations between tech firms and pharma companies in the U.S. and Canada are driving progress in the creation of advanced drug discovery solutions and deepening the regional footprint of AI platforms.

Key players in the Global Artificial Intelligence in Drug Discovery Market are Exscientia, BenevolentAI, Orakl Oncology, AVAYL, Atomwise, Aevai Health, Cyclica, Examol, IBM Corporation, NVIDIA Corporation, Microsoft, Insilico Medicine, Deep Genomics, DenovAI Biotech, chAIron, Aureka Biotechnologies, LinkGevity, 9Bio Therapeutics, Helical, Google (DeepMind), and Deargen. To secure a competitive edge in the Global Artificial Intelligence in Drug Discovery Market, companies are focusing on technology innovation, strategic collaborations, and data-driven product development. Leading players are investing in the development of proprietary AI algorithms that enhance target identification, molecule generation, and clinical success rates. Partnerships between biotech startups and pharma leaders are becoming more prevalent, enabling access to large datasets, domain knowledge, and scalable computing resources.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Technology trends

- 2.2.4 Application type trends

- 2.2.5 Therapeutic area trends

- 2.2.6 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of complex and chronic diseases

- 3.2.1.2 Data explosion and digitization in healthcare

- 3.2.1.3 Advancements in AI algorithms and computing power

- 3.2.1.4 Growing collaboration between tech and pharma companies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data quality and integration issues

- 3.2.2.2 Regulatory and ethical concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized and precision medicine

- 3.2.3.2 Emergence of generative AI in molecule design

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Investment and funding landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.3 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Machine learning

- 6.3 Deep learning

- 6.3.1 Supervised learning

- 6.3.2 Unsupervised learning

- 6.3.3 Other machine learning technologies

- 6.4 Other technology

Chapter 7 Market Estimates and Forecast, By Application Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Molecular library screening

- 7.3 Target Identification

- 7.4 Drug optimization and repurposing

- 7.5 De novo drug designing

- 7.6 Preclinical testing

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By Therapeutic Area, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oncology

- 8.3 Neurodegenerative diseases

- 8.4 Inflammatory

- 8.5 Infectious diseases

- 8.6 Metabolic diseases

- 8.7 Rare diseases

- 8.8 Cardiovascular diseases

- 8.9 Other therapeutic areas

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Pharmaceutical and biotechnology companies

- 9.3 Contract research organization (CROs)

- 9.4 Other End uses

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 9Bio Therapeutics

- 11.2 Aevai Health

- 11.3 Atomwise

- 11.4 Aureka Biotechnologies

- 11.5 AVAYL

- 11.6 BenevolentAI

- 11.7 chAIron

- 11.8 Cyclica

- 11.9 Deargen

- 11.10 Deep Genomics

- 11.11 DenovAI Biotech

- 11.12 Examol

- 11.13 Exscientia

- 11.14 Google (DeepMind)

- 11.15 Helical

- 11.16 IBM Corporation

- 11.17 Insilico Medicine

- 11.18 LinkGevity

- 11.19 Microsoft

- 11.20 NVIDIA Corporation

- 11.21 Orakl Oncology

人工智慧浪潮席捲夏威夷——電力和光纖瓶頸:

人工智慧浪潮席捲夏威夷——電力和光纖瓶頸: 2026-2034年人工智慧(AI)驅動藥物發現全球市場規模、佔有率、趨勢和成長分析報告

2026-2034年人工智慧(AI)驅動藥物發現全球市場規模、佔有率、趨勢和成長分析報告 日本人工智慧藥物發現市場規模、市場佔有率、趨勢和預測:按服務提供、應用、治療領域、最終用戶和地區分類(2026-2034 年)

日本人工智慧藥物發現市場規模、市場佔有率、趨勢和預測:按服務提供、應用、治療領域、最終用戶和地區分類(2026-2034 年) AI蛋白質設計市場:按蛋白質類型、技術平台、方法、應用、最終用戶和部署類型分類-2026-2032年全球預測基於人工智慧的胜肽類藥物發現平台市場(按技術類型、治療用途、胜肽和最終用戶分類)—2026-2032年全球預測

AI蛋白質設計市場:按蛋白質類型、技術平台、方法、應用、最終用戶和部署類型分類-2026-2032年全球預測基於人工智慧的胜肽類藥物發現平台市場(按技術類型、治療用途、胜肽和最終用戶分類)—2026-2032年全球預測 人工智慧藥物發現市場規模、佔有率和趨勢分析報告:按應用、治療領域、最終用途、地區和細分市場預測,2026-2033年

人工智慧藥物發現市場規模、佔有率和趨勢分析報告:按應用、治療領域、最終用途、地區和細分市場預測,2026-2033年 人工智慧在藥物研發領域的市場:產業趨勢及全球預測(至2040年)-按應用、影像處理類型和主要地區劃分

人工智慧在藥物研發領域的市場:產業趨勢及全球預測(至2040年)-按應用、影像處理類型和主要地區劃分 人工智慧藥物發現市場預測至2032年:按藥物類型、治療領域、技術、應用、最終用戶和地區分類的全球分析

人工智慧藥物發現市場預測至2032年:按藥物類型、治療領域、技術、應用、最終用戶和地區分類的全球分析 人工智慧在藥物研發中的應用:全球市場佔有率和排名、總收入和需求預測(2025-2031年)2032 年人工智慧藥物研發平台市場預測:按組件、治療領域、藥物類型、部署模式、最終用戶和地區進行的全球分析

人工智慧在藥物研發中的應用:全球市場佔有率和排名、總收入和需求預測(2025-2031年)2032 年人工智慧藥物研發平台市場預測:按組件、治療領域、藥物類型、部署模式、最終用戶和地區進行的全球分析