|

市場調查報告書

商品編碼

1858864

軟體機器人用液晶彈性體市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Liquid Crystal Elastomers for Soft Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

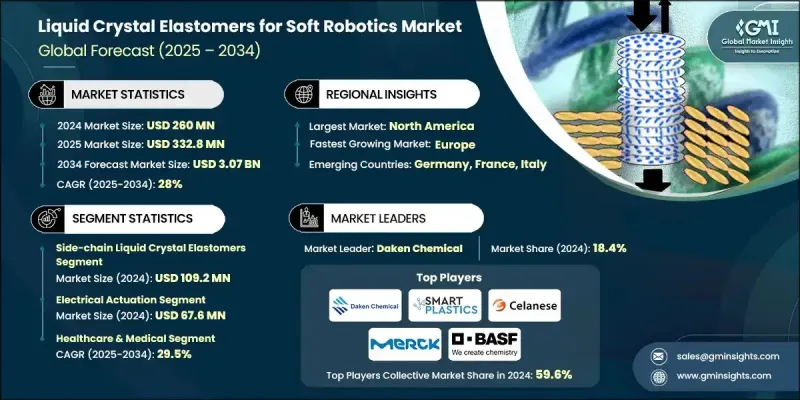

2024 年全球軟體機器人用液晶彈性體市場價值為 2.6 億美元,預計到 2034 年將以 28% 的複合年成長率成長至 30.7 億美元。

在醫療保健、消費科技和自動化等領域,對液晶彈性體的需求正日益成長,性能和整合度的提升發揮著至關重要的作用。其應用趨勢與其他顛覆性致動器技術的發展趨勢相符,尤其是在液晶彈性體纖維的功率密度達到 293 W/kg、做功能力高達 650 J/kg 時,其性能已超越天然肌肉。隨著纖維基和編織系統在實際負載條件下持續實現多功能運動,人們對其可擴展性和工業可靠性的信心也在不斷增強。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.6億美元 |

| 預測值 | 30.7億美元 |

| 複合年成長率 | 28% |

由於需要客製化液晶基元、取向層和交聯劑,材料成本約佔總成本的35-40%;而製造成本則佔25-30%,這主要是由於精確交聯、分子取向和高保真加工等技術要求。然而,隨著直接墨水書寫和先進纖維擠出等積層製造技術的普及,這種成本結構正在發生變化,這些技術降低了資本投入,並擴大了設計自由度。現在無需客製化模具即可實現複雜的幾何形狀和特定位置的材料取向,從而加快原型製作速度並實現多樣化的終端產品線。

到2024年,製造服務板塊將佔據25%的市場佔有率,這反映了高階製造技術在交付成品液晶元件方面的重要作用。以性能為導向的採購方式正日益取代以材料為中心的採購方式,整合系統和可程式驅動技術正日益受到重視。

2024年,側鏈液晶彈性體(LCE)市場規模達到1.092億美元,憑藉其適應性強、成本效益高且易於加工等優勢,佔據了市場主導地位。側鏈型液晶彈性體在紡織品和軟性穿戴設備領域表現出色,而主鏈型和混合型液晶彈性體則因其強度和熱穩定性,在航太、機器人和精密應用領域日益普及。隨著4D列印技術的進步,能夠實現具有高方向控制的多層、多材料構建,預計這些不同結構之間的競爭優勢將進一步縮小,市場細分將更多地基於功能而非結構。

2024年,北美軟體機器人用液晶彈性體市佔率達45%。該地區的領先地位得益於強大的研究生態系統、國防主導的計劃以及醫療創新。政府支持的研發活動推動了金屬化液晶彈性體薄膜和可編程熱性能的突破,這些技術目前正應用於穿戴式壓縮系統和臨床級義肢。美國市場正隨著國防和醫療保健需求的成長而擴張,而加拿大的貢獻則主要來自大學機器人項目,這些項目正在試點用於人機互動的軟驅動技術。目前的臨床試驗表明,該技術可在20-60 mmHg範圍內調節驅動,並可重複使用,這增強了人們對醫療級應用的信心。

活躍於軟體機器人液晶彈性體市場的主要企業包括默克集團(Merck KGaA)、巴斯夫公司(BASF SE)、塞拉尼斯公司(Celanese Corporation)、Beam公司、達肯化學公司(Daken Chemical)、Smart-Plastics Ltd、Synthon Chemicals、Wilshire Technologies和TCI America。這些企業正利用創新、策略合作和材料工程技術來確保長期成長。研發重點在於改進液晶彈性體的分子設計、耐久性和溫度穩定性,同時拓展其合成能力,以實現可擴展的生產規模。企業正投資於精密製造技術,例如4D列印和先進擠出技術,以支援客製化幾何形狀和精確的對準控制。與學術機構和醫療器材開發商的合作,正幫助企業根據醫療保健、航太和穿戴式科技等領域的需求來定製材料。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 刺激反應驅動能力

- 積層製造技術的進步

- 對自主和自持機器人的需求

- 整合到智慧紡織品和穿戴式設備中

- 產業陷阱與挑戰

- 執行速度慢

- 複雜的製造技術

- 功率密度有限

- 市場機遇

- 有助於開發具有更高靈活性和精確性的下一代生物醫學設備

- 促進智慧穿戴裝置和響應式紡織品的創新

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依材料類型分類,2021-2034年

- 主要趨勢

- 主鏈液晶彈性體

- 聚矽氧烷基液晶彈性體

- 基於聚丙烯酸酯的液晶彈性體

- 聚酯基液晶彈性體

- 聚氨酯基液晶彈性體

- 側鏈液晶彈性體

- 端基側鏈LCE

- 側鏈液晶彈性體

- 側向連接的液晶彈性體

- 離子液晶彈性體(iLCEs)

- 陽離子型液晶彈性體

- 陰離子型液晶彈性體

- 兩性離子液晶彈性體

- 複合型和混合型液晶彈性體

- 碳基複合材料(碳奈米管、石墨烯、氧化石墨烯)

- 金屬奈米顆粒複合材料(Au、Ag、Fe3O4)

- 液態金屬嵌入式液晶彈性體

- 陶瓷填充液晶彈性體

第6章:市場估算與預測:以驅動方式分類,2021-2034年

- 主要趨勢

- 熱驅動

- 直接熱加熱

- 焦耳熱(電熱)

- 感應加熱

- 光學驅動

- 光化學(偶氮苯基)

- 光熱(碳奈米管、金奈米粒子)

- 近紅外線響應

- 對可見光有響應

- 電動驅動

- 介電驅動

- 靜電驅動

- 離子驅動

- 磁場驅動

- 磁熱

- 直接磁扭矩

- 多模態驅動

- 熱光組合

- 電熱組合

- 射頻控制系統

第7章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 醫療保健

- 醫療器材及植入物

- 義肢和矯形器

- 藥物輸送系統

- 手術機器人

- 復健設備

- 生物醫學研究工具

- 航太與國防

- 變形飛機結構

- 自適應偽裝系統

- 可展開式空間結構

- 自主軍用機器人

- 監視與偵察

- 導彈和火箭部件

- 製造與工業自動化

- 軟體機器人抓手

- 裝配線自動化

- 物料搬運系統

- 品質控制與檢驗

- 包裝與加工

- 維護和維修機器人

- 消費性電子產品和穿戴式裝置

- 智慧紡織品和服裝

- 穿戴式健康監測器

- 觸覺回饋設備

- 軟性顯示器

- 個人輔助設備

- 遊戲與娛樂

- 汽車

- 自適應座椅系統

- 主動空氣動力學

- 振動阻尼

- 車內舒適系統

- 安全防護系統

- 研發

- 學術研究機構

- 政府研究實驗室

- 材料測試與表徵

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Smart-Plastics Ltd

- Celanese Corporation

- Merck KGaA

- Synthon Chemicals

- Beam Co

- Wilshire Technologies

- TCI America

- BASF Corporation

- Daken Chemical

The Global Liquid Crystal Elastomers for Soft Robotics Market was valued at USD 260 million in 2024 and is estimated to grow at a CAGR of 28% to reach USD 3.07 billion by 2034.

The demand is gaining momentum across sectors like healthcare, consumer tech, and automation, with advancements in performance and integration playing a crucial role. The adoption curve mirrors trends observed in other disruptive actuator technologies, particularly as LCE fibers begin outperforming natural muscle with power density reaching 293 W/kg and work capacity up to 650 J/kg. As fiber-based and woven systems consistently deliver multifunctional motion under real load conditions, confidence in scalability and industrial reliability is accelerating.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $260 Million |

| Forecast Value | $3.07 Billion |

| CAGR | 28% |

Material costs account for approximately 35-40% of the total due to the need for tailored mesogens, alignment layers, and crosslinkers, while fabrication represents another 25-30% owing to technical demands like precise crosslinking, molecular alignment, and high-fidelity machining. However, this cost structure is evolving as additive manufacturing methods such as direct ink writing and advanced fiber extrusion gain traction, reducing capital requirements and expanding design freedom. Complex geometries and site-specific material alignment are now possible without custom molds, enabling quicker prototyping and diversified end-product lines.

The manufacturing services segment held 25% share in 2024, reflecting the role of high-end fabrication techniques in delivering finished LCE components. Performance-driven buying is increasingly replacing materials-focused procurement, with integrated systems and programmable actuation gaining priority.

In 2024, sidechain LCEs segment accounted for USD 109.2 million, capturing a dominant share due to their balance of adaptability, cost-efficiency, and ease of processing. While side-chain types excel in textiles and flexible wearables, main-chain and hybrid structures are gaining popularity in aerospace, robotics, and precision applications due to their strength and thermal stability. As 4D printing technologies evolve, allowing for multilayer, multimaterial builds with high directional control, the competitive edge between these formats is expected to tighten, leading to greater market segmentation based on function rather than format.

North America Liquid Crystal Elastomers for Soft Robotics Market held 45% share in 2024. The region's dominance is driven by strong research ecosystems, defense-led initiatives, and medical innovation. Government-backed R&D has led to breakthroughs in metallized LCE films and programmable thermal properties, which are now finding applications in wearable compression systems and clinical-grade prosthetics. The US market is expanding with defense and healthcare demand, while Canada's contribution is shaped by university-based robotics programs piloting soft actuation for human-machine interfaces. Current clinical pilots demonstrate adjustable actuation between 20-60 mmHg and reusable cycling, reinforcing confidence in healthcare-grade applications.

Key players active in the Liquid Crystal Elastomers for Soft Robotics Market include Merck KGaA, BASF SE, Celanese Corporation, Beam Co, Daken Chemical, Smart-Plastics Ltd, Synthon Chemicals, Wilshire Technologies, and TCI America. Companies competing in the Liquid Crystal Elastomers for Soft Robotics Market are leveraging innovation, strategic partnerships, and materials engineering to secure long-term growth. Focused R&D is being used to improve molecular design, durability, and temperature stability of LCEs while also expanding synthesis capabilities for scalable formats. Players are investing in precision manufacturing techniques such as 4D printing and advanced extrusion to support custom geometries and alignment control. Collaborations with academic institutions and medical device developers are helping firms tailor their materials to healthcare, aerospace, and wearable tech.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Admixtures

- 2.2.3 Application Methods

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stimuli-responsive actuation capabilities

- 3.2.1.2 Advancements in additive manufacturing

- 3.2.1.3 Demand for autonomous and self-sustained robotics

- 3.2.1.4 Integration into smart textiles and wearables

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Slow actuation speed

- 3.2.2.2 Complex fabrication techniques

- 3.2.2.3 Limited power density

- 3.2.3 Market opportunities

- 3.2.3.1 Enables development of next-gen biomedical devices with enhanced flexibility and precision

- 3.2.3.2 Facilitates innovation in smart wearables and responsive textiles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Main-chain liquid crystal elastomers

- 5.2.1 Polysiloxane-based LCEs

- 5.2.2 Polyacrylate-based LCEs

- 5.2.3 Polyester-based LCEs

- 5.2.4 Polyurethane-based LCEs

- 5.3 Side-chain liquid crystal elastomers

- 5.3.1 End-on Sidechain LCEs

- 5.3.2 Side-on Sidechain LCEs

- 5.3.3 Laterally Attached LCEs

- 5.4 Ionic liquid crystal elastomers (iLCEs)

- 5.4.1 Cationic iLCEs

- 5.4.2 Anionic iLCEs

- 5.4.3 Zwitterionic iLCEs

- 5.5 Composite & hybrid LCEs

- 5.5.1 Carbon-based Composites (CNT, Graphene, GO)

- 5.5.2 Metal Nanoparticle Composites (Au, Ag, Fe3O4)

- 5.5.3 Liquid Metal Embedded LCEs

- 5.5.4 Ceramic-filled LCEs

Chapter 6 Market Estimates and Forecast, By Actuation Mode, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thermal actuation

- 6.2.1 Direct thermal heating

- 6.2.2 Joule heating (electrothermal)

- 6.2.3 Induction heating

- 6.3 Optical actuation

- 6.3.1 Photochemical (azobenzene-based)

- 6.3.2 Photothermal (CNT, gold nanoparticles)

- 6.3.3 Near-infrared responsive

- 6.3.4 Visible light responsive

- 6.4 Electrical actuation

- 6.4.1 Dielectric actuation

- 6.4.2 Electrostatic actuation

- 6.4.3 Ionic actuation

- 6.5 Magnetic field actuation

- 6.5.1 Magnetothermal

- 6.5.2 Direct magnetic torque

- 6.6 Multi-modal actuation

- 6.6.1 Thermal-optical combined

- 6.6.2 Electrical-thermal combined

- 6.6.3 Rf-controlled systems

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Healthcare & Medical

- 7.2.1 Medical devices & implants

- 7.2.2 Prosthetics & orthotics

- 7.2.3 Drug delivery systems

- 7.2.4 Surgical robotics

- 7.2.5 Rehabilitation equipment

- 7.2.6 Biomedical research tools

- 7.3 Aerospace & Defense

- 7.3.1 Morphing aircraft structures

- 7.3.2 Adaptive camouflage systems

- 7.3.3 Deployable space structures

- 7.3.4 Autonomous military robots

- 7.3.5 Surveillance & reconnaissance

- 7.3.6 Missile & rocket components

- 7.4 Manufacturing & Industrial Automation

- 7.4.1 Soft robotic grippers

- 7.4.2 Assembly line automation

- 7.4.3 Material handling systems

- 7.4.4 Quality control & inspection

- 7.4.5 Packaging & processing

- 7.4.6 Maintenance & repair robots

- 7.5 Consumer Electronics & Wearables

- 7.5.1 Smart textiles & clothing

- 7.5.2 Wearable health monitors

- 7.5.3 Haptic feedback devices

- 7.5.4 Flexible displays

- 7.5.5 Personal assistive devices

- 7.5.6 Gaming & entertainment

- 7.6 Automotive

- 7.6.1 Adaptive seating systems

- 7.6.2 Active aerodynamics

- 7.6.3 Vibration damping

- 7.6.4 Interior comfort systems

- 7.6.5 Safety & protection systems

- 7.7 Research & Development

- 7.7.1 Academic research institutions

- 7.7.2 Government research labs

- 7.7.3 Material testing & characterization

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Smart-Plastics Ltd

- 9.2 Celanese Corporation

- 9.3 Merck KGaA

- 9.4 Synthon Chemicals

- 9.5 Beam Co

- 9.6 Wilshire Technologies

- 9.7 TCI America

- 9.8 BASF Corporation

- 9.9 Daken Chemical

軟性機器人市場:按類型、材料、技術和應用分類-2026-2032年全球市場預測

軟性機器人市場:按類型、材料、技術和應用分類-2026-2032年全球市場預測 2026年全球軟體機器人控制電子設備市場報告

2026年全球軟體機器人控制電子設備市場報告 軟體機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類2026年全球軟體機器人市場報告

軟體機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、功能、安裝類型分類2026年全球軟體機器人市場報告 軟體機器人市場規模、佔有率和成長分析(按類型、組件、材料、應用和地區分類)-2026-2033年產業預測

軟體機器人市場規模、佔有率和成長分析(按類型、組件、材料、應用和地區分類)-2026-2033年產業預測 全球軟體機器人市場

全球軟體機器人市場 全球軟機器人市場:市場規模(按類型、應用和地區)、未來預測

全球軟機器人市場:市場規模(按類型、應用和地區)、未來預測 軟體機器人市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

軟體機器人市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 軟機器人-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

軟機器人-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2030 年軟機器人市場預測:按類型、組件、材料、應用、最終用戶和地區進行的全球分析

2030 年軟機器人市場預測:按類型、組件、材料、應用、最終用戶和地區進行的全球分析