|

市場調查報告書

商品編碼

1844381

固定式離岸風能市場機會、成長動力、產業趨勢分析及2025-2034年預測Fixed Offshore Wind Energy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

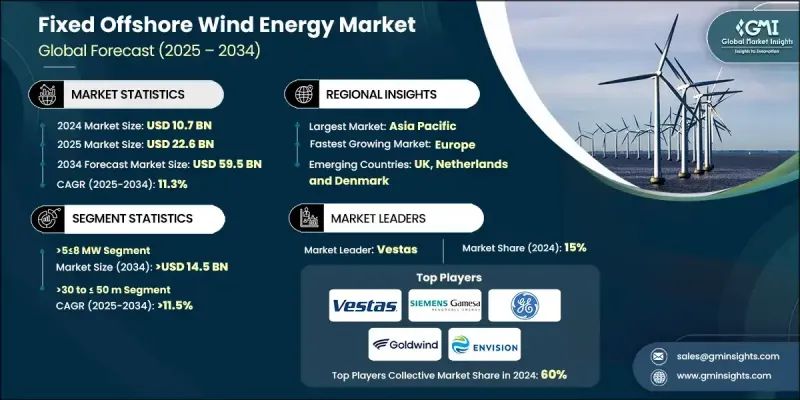

2024 年全球固定式離岸風能市場價值為 107 億美元,預計到 2034 年將以 11.3% 的複合年成長率成長至 595 億美元。

這一成長主要得益於政府的支持性舉措、沿海地區能源需求的不斷成長以及對減少碳排放的日益重視。多個地區的政策制定者正在推出再生能源強制規定、財政激勵措施和拍賣框架,以加速離岸風電的發展。由於人口稠密的沿海地區需要清潔高效的能源,強勁且穩定的離岸風電資源使這項技術成為切實可行的選擇。這些項目也能減少輸電損耗,提高向城市和工業區的電力傳輸效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 107億美元 |

| 預測值 | 595億美元 |

| 複合年成長率 | 11.3% |

更高容量的渦輪機在提升營運產量方面發揮著重要作用,新技術則提升了可靠性和性能,並降低了維護成本。基礎結構、葉片設計和施工技術的創新正在最佳化安裝進度並降低資本支出。此外,主要市場參與者正在加大研發投入,以擴大生產規模,同時確保長期成本競爭力。旨在改善電網整合和最大限度提高產能利用率的策略性進步,正在為固定式離岸風電領域的持續成長奠定基礎。

預計到2034年,2兆瓦及以下風電市場規模將達到80億美元,這得益於其在島嶼、淺海沿岸地區以及電網基礎設施有限的低需求地區等小型項目中的適應性。這些風力渦輪機非常適合無法建造大型離岸風電場的市場。發展中國家對混合能源系統的興趣日益濃厚,以及相關激勵措施的訂定,將進一步推動該領域的成長。

預計30公尺以上至50公尺以下的市場規模將達到270億美元,這得益於技術進步,使得在更深的水域部署成為可能。沿海風電計畫正在深水區迅速擴張,以提高發電能力。此外,政府為推廣浮動平台和更深的離岸風電計畫提供的補貼正在重塑產業格局,在先前被認為不適合建造固定結構的海域釋放出新的機會。

2024年,美國固定式離岸風電市場規模達18億美元。作為離岸風電發展中心,美國持續實施激勵計劃和專案專屬框架,例如租賃和許可計劃,以促進主要沿海地區的離岸風電部署。能源巨頭正透過對東海岸地區的資本投資做出長期承諾,顯示該地區離岸風電產業發展勢頭強勁。

全球固定式離岸風電市場領導者包括Southwire公司、Impsa、Iberdrola、Enessere、Equinor、西門子歌美颯可再生能源、Vattenfall、金風科技、住友電工、耐克森、通用電氣、GE Vernova、中國長江三峽能源公司、RWESE能源、JLS、可再生能源集團、電纜、再生能源集團和古塔斯系統。為了鞏固其在固定式離岸風電市場的地位,各企業正專注於建立長期合資企業、擴大製造能力和本地化供應鏈以改善成本結構。許多企業正在投資大型海上樞紐,並與政府和區域公用事業公司建立策略合作夥伴關係,以確保長期合約。多樣化風機組合、改進模組化設計以及整合智慧監控技術也已成為其策略的核心。這些企業更加重視風扇效率、基礎類型和數位資產管理方面的創新,從而能夠提高能源產量和營運效率,最終增強其在離岸風電部署方面的全球競爭力。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統

- 監管格局

- 2021-2034年價格趨勢分析

- 按渦輪額定功率

- 按地區

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL分析

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

- 戰略儀表板

- 策略舉措

- 公司標竿分析

- 創新與技術格局

第5章:市場規模及預測:以渦輪機額定功率,2021 - 2034

- 主要趨勢

- ≤2兆瓦

- >2≤5兆瓦

- >5≤8兆瓦

- >8≤10兆瓦

- >10≤12兆瓦

- > 12 兆瓦

第6章:市場規模及預測:按軸,2021 - 2034

- 主要趨勢

- 水平的

- 逆風

- 順風

- 垂直的

第7章:市場規模及預測:依組件分類,2021 - 2034

- 主要趨勢

- 刀片

- 塔樓

- 其他

第8章:市場規模及預測:依深度,2021 - 2034

- 主要趨勢

- >0 ≤ 30 米

- >30 ≤ 50 米

- > 50米

第9章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 西班牙

- 英國

- 法國

- 義大利

- 瑞典

- 波蘭

- 丹麥

- 葡萄牙

- 荷蘭

- 愛爾蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 韓國

- 越南

- 菲律賓

- 台灣

第10章:公司簡介

- China Three Gorges

- Enessere

- Equinor

- Furukawa Electric

- General Electric

- GE Vernova

- Goldwind

- Impsa

- Iberdrola

- JERA

- Ls Cable & System

- Nexans

- Prysmian Group

- RWE Renewables

- SSE Renewables

- Sumitomo Electric Industries

- Southwire Company

- Siemens Gamesa Renewable Energy

- Vestas

- Vattenfall

The Global Fixed Offshore Wind Energy Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 59.5 billion by 2034.

The growth is primarily driven by a combination of supportive government initiatives, rising energy demand in coastal zones, and heightened focus on cutting carbon emissions. Policymakers across several regions are rolling out renewable energy mandates, financial incentives, and auction frameworks to accelerate offshore wind development. With densely populated coastal regions requiring clean and efficient energy sources, the availability of strong and consistent offshore wind resources continues to make this technology a practical choice. These projects also reduce transmission losses and improve electricity delivery efficiency to urban and industrial zones.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $59.5 Billion |

| CAGR | 11.3% |

Higher-capacity turbines are playing a major role in pushing operational output, with newer technologies enhancing reliability, performance, and lowering maintenance costs. Innovations in foundation structures, blade design, and construction techniques are optimizing installation timelines and reducing capital expenditure. Moreover, major market players are channeling investments into R&D to scale up production while ensuring long-term cost competitiveness. Strategic advancements, aimed at improving grid integration and maximizing capacity utilization, are laying the foundation for sustained growth in the fixed offshore wind energy space.

The <= 2 MW segment is expected to reach USD 8 billion by 2034, supported by its adaptability in smaller-scale projects such as island installations, shallow coastal zones, and low-demand areas with limited grid infrastructure. These turbines are ideal for markets where full-scale offshore farms are not viable. Increased interest in hybrid energy systems and incentives across developing countries will add further momentum to this segment's growth trajectory.

The >30 to <=50 m segment is forecast to reach USD 27 billion, fueled by technological advancements that allow for deployment at greater water depths. Coastal wind projects are expanding rapidly in deeper waters to increase power generation capacity. Additionally, government-backed subsidies aimed at promoting floating platforms and deeper offshore turbine projects are reshaping the industry, unlocking opportunities in areas previously considered non-viable for fixed structures.

U.S. Fixed Offshore Wind Energy Market was valued at USD 1.8 billion in 2024. As a growing hub for offshore wind, the U.S. continues to implement incentive schemes and project-specific frameworks, such as leasing and permitting initiatives, that are bolstering deployment along key coastal regions. Energy giants are making long-term commitments through capital investments along the East Coast, signaling strong forward momentum in the regional industry.

Leading companies in the Global Fixed Offshore Wind Energy Market include Southwire Company, Impsa, Iberdrola, Enessere, Equinor, Siemens Gamesa Renewable Energy, Vattenfall, Goldwind, Sumitomo Electric Industries, Nexans, General Electric, GE Vernova, China Three Gorges, RWE Renewables, JERA, Prysmian Group, LS Cable & System, Furukawa Electric, SSE Renewables, and Vestas. To strengthen their position in the fixed offshore wind energy market, companies are focusing on long-term joint ventures, expanding manufacturing capabilities, and localizing supply chains to improve cost structures. Many are investing in large-scale offshore hubs and building strategic partnerships with governments and regional utilities to secure long-term contracts. Diversifying turbine portfolios, improving modular design, and integrating smart monitoring technologies have also become central to their strategy. Enhanced focus on innovation in turbine efficiency, foundation types, and digital asset management allows these firms to improve energy yield and operational efficiency, ultimately reinforcing their global competitiveness in offshore wind deployment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Turbine rating trends

- 2.4 Axis trends

- 2.5 Component trends

- 2.6 Depth trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Price trend analysis, 2021-2034

- 3.3.1 By turbine rating

- 3.3.2 By region

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Turbine rating, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 2 MW

- 5.3 >2≤ 5 MW

- 5.4 >5≤ 8 MW

- 5.5 >8≤10 MW

- 5.6 >10≤ 12 MW

- 5.7 > 12 MW

Chapter 6 Market Size and Forecast, By Axis, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Horizontal

- 6.2.1 Up-wind

- 6.2.2 Down-wind

- 6.3 Vertical

Chapter 7 Market Size and Forecast, By Component, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Blades

- 7.3 Towers

- 7.4 Others

Chapter 8 Market Size and Forecast, By Depth, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 >0 ≤ 30 m

- 8.3 >30 ≤ 50 m

- 8.4 > 50 m

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Spain

- 9.3.3 UK

- 9.3.4 France

- 9.3.5 Italy

- 9.3.6 Sweden

- 9.3.7 Poland

- 9.3.8 Denmark

- 9.3.9 Portugal

- 9.3.10 Netherlands

- 9.3.11 Ireland

- 9.3.12 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Australia

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Vietnam

- 9.4.7 Philippines

- 9.4.8 Taiwan

Chapter 10 Company Profiles

- 10.1 China Three Gorges

- 10.2 Enessere

- 10.3 Equinor

- 10.4 Furukawa Electric

- 10.5 General Electric

- 10.6 GE Vernova

- 10.7 Goldwind

- 10.8 Impsa

- 10.9 Iberdrola

- 10.10 JERA

- 10.11 Ls Cable & System

- 10.12 Nexans

- 10.13 Prysmian Group

- 10.14 RWE Renewables

- 10.15 SSE Renewables

- 10.16 Sumitomo Electric Industries

- 10.17 Southwire Company

- 10.18 Siemens Gamesa Renewable Energy

- 10.19 Vestas

- 10.20 Vattenfall

離岸風力發電市場:按組件、基礎類型、渦輪機功率、應用和最終用戶分類-2026-2032年全球市場預測

離岸風力發電市場:按組件、基礎類型、渦輪機功率、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球離岸風電市場報告

2026年全球離岸風電市場報告 離岸風力發電市場報告:按組件、基礎類型、容量、位置和地區分類(2026-2034 年)離岸風力發電單樁市場依結構類型、水深等級、風扇容量等級及最終用戶分類,2026-2032年預測

離岸風力發電市場報告:按組件、基礎類型、容量、位置和地區分類(2026-2034 年)離岸風力發電單樁市場依結構類型、水深等級、風扇容量等級及最終用戶分類,2026-2032年預測 離岸風力發電市場機會、成長要素、產業趨勢分析及2026年至2035年預測

離岸風力發電市場機會、成長要素、產業趨勢分析及2026年至2035年預測 近期技術發展及電力製X路徑的技術經濟評估離岸風力發電貫入試驗市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

近期技術發展及電力製X路徑的技術經濟評估離岸風力發電貫入試驗市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 全球離岸風電電氣基礎設施市場:預測(至2034年)-按組件、電纜、輸電技術、安裝方式、併網/整合、安裝/試運行服務和區域進行分析日本離岸風力發電市場規模、佔有率、趨勢及預測(按安裝方式、水深、容量和地區分類,2026-2034年)日本離岸風力發電市場規模、佔有率、趨勢和預測:按組件、基礎類型、容量、水域面積和地區分類,2026-2034年

全球離岸風電電氣基礎設施市場:預測(至2034年)-按組件、電纜、輸電技術、安裝方式、併網/整合、安裝/試運行服務和區域進行分析日本離岸風力發電市場規模、佔有率、趨勢及預測(按安裝方式、水深、容量和地區分類,2026-2034年)日本離岸風力發電市場規模、佔有率、趨勢和預測:按組件、基礎類型、容量、水域面積和地區分類,2026-2034年