|

市場調查報告書

商品編碼

1833650

自卸卡車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dump Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

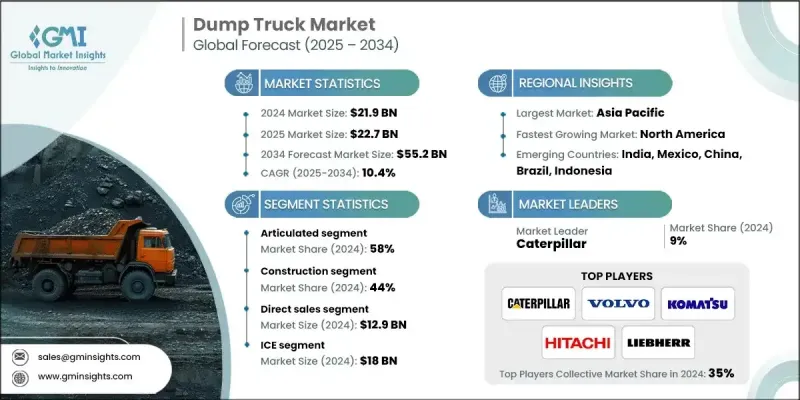

2024 年全球自卸卡車市場價值為 219 億美元,預計將以 10.4% 的複合年成長率成長,到 2034 年達到 552 億美元。

受人們對電氣化和自動駕駛技術日益成長的興趣推動,該行業正在經歷一場變革性的轉變。製造商面臨的減排和提高能源效率的壓力日益增大,這推動了電動自卸卡車的發展。同時,自動化技術也日益普及,其技術可減少操作失誤、降低成本,並實現遠端控制或完全自動駕駛車隊營運。這些進步正在重塑傳統的營運模式,為更清潔、更智慧、更經濟高效的運輸解決方案鋪路。儘管該行業曾經在線性供應鏈和傳統工作流程下營運,但在新冠疫情之後,情況發生了顯著變化。此前,該行業以穩步成長和最小中斷為特徵,如今,市場正在應對衛生、物流和員工互動方面的挑戰,推動數位轉型、車輛功能創新和永續生產的需求。不斷發展的生態系統需要更敏捷的方法,迫使製造商從傳統的設計和生產模式轉向以技術為驅動的整合式商業模式,以解決安全性、永續性和生產力問題。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 219億美元 |

| 預測值 | 552億美元 |

| 複合年成長率 | 10.4% |

2024年,鉸接式自卸卡車市場佔據58%的市場佔有率,預計2025年至2034年期間的複合年成長率將達到11%。鉸接式卡車的有效載荷能力和越野性能正在不斷提升。隨著對能夠承載更大載重量並能在崎嶇不平路面上保持靈活性的卡車的需求不斷成長,製造商正在大力投資設計創新。增強型傳動系統、底盤改裝和改進的懸吊系統正在實施,以滿足在惡劣條件下對穩定性、適應性和更高燃油經濟性的需求。隨著基礎設施項目日益複雜且環境日益嚴峻,鉸接式卡車提供了高效運輸物料的理想解決方案,同時最大限度地提高了安全性和耐用性。

建築業在2024年佔據了44%的市場佔有率,預計到2034年將以11.7%的複合年成長率成長。建築業對高度專業化的自卸卡車的需求日益成長,這正在重塑產品開發。製造商正專注於打造能夠滿足各種建築需求的車型,從適合城市發展的緊湊型車型到專為大型基礎設施項目設計的大型越野車型。隨著應用範圍的不斷擴大,企業越來越重視多功能性、燃油效率以及與遠端資訊處理和負載監控系統的整合。隨著建築公司尋求針對特定任務和環境量身定做的設備,對客製化高性能自卸卡車的需求持續激增。

中國自卸卡車市場佔45%的市場佔有率,2024年市場規模達42億美元。中國積極推動擴大採礦業務,並擴大國內煤炭產量以減少對進口的依賴,這導致對大容量自卸卡車的需求持續成長。中國在全球鋼鐵製造業的主導地位以及在稀土金屬生產中的主導地位(控制全球大部分產量)進一步加速了對強大自卸卡車車隊的需求。為了支持這些產業,中國加大了對耐用重型車輛的投資,這些車輛能夠長時間維持大容量作業,尤其是在具有挑戰性的地形條件下。

引領全球自卸卡車市場的領導企業包括日立、別拉斯、沃爾沃、斯堪尼亞、康明斯、三一、派克漢尼汾、Caterpillar、利勃海爾和小松。自卸卡車產業的頂尖企業正積極專注於創新、產品多元化和區域市場滲透,以增強其競爭地位。許多企業正透過開發電池驅動和混合動力車型,朝向電氣化邁進,以滿足全球排放標準。各公司也正在整合數位工具,包括GPS追蹤、自動裝載系統和車隊管理軟體,以提高營運效率。與當地經銷商和基礎設施公司的策略合作有助於提升品牌在新興市場的知名度和客戶忠誠度。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 製造商

- 經銷商

- 最終用途

- 成本結構

- 利潤率

- 每個階段的增值

- 影響供應鏈的因素

- 破壞者

- 供應商格局

- 對部隊的影響

- 成長動力

- 基礎設施擴張刺激自卸卡車需求

- 技術進步提高了自卸卡車的效率和安全性

- 政府對交通基礎設施的投資刺激了需求

- 採礦業的成長推動了自卸卡車的銷售

- 產業陷阱與挑戰

- 經濟衰退減少了建築和採礦活動

- 嚴格的排放法規增加了製造成本

- 市場機會

- 電動和混合動力自卸卡車的普及率不斷上升

- 智慧車隊管理和遠端資訊處理整合

- 成長動力

- 技術趨勢與創新生態系統

- 現有技術

- 自主系統開發與實施路線圖

- 電動和混合動力系統的演變和市場採用

- 遠端資訊處理及物聯網整合進展及資料分析

- 預測性維護和人工智慧應用開發

- 新興技術

- 網路安全解決方案與連接設備保護

- 區塊鏈整合和供應鏈透明度

- 擴增實境和虛擬培訓系統開發

- 5G連線與即時資料處理應用

- 現有技術

- 監管格局

- 全球排放標準與環境法規

- 採礦安全法規和 MSHA 合規性

- 自動駕駛汽車法規和標準

- 國際貿易和關稅影響

- 網路安全法規和資料保護

- 售後服務及支援生態系統

- 零件售後市場分析

- 維護和維修服務市場

- 培訓和認證項目市場

- 數位服務和軟體解決方案

- 融資租賃市場分析

- 設備融資市場動態

- 設備租賃市場分析

- 租賃市場和短期解決方案

- 替代融資解決方案

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 永續性和環境方面

- 環境影響評估與生命週期分析

- 社會影響力和社區關係

- 治理與企業責任

- 永續技術發展

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依產品,2021 - 2034

- 主要趨勢

- 鉸接式

- 50公噸以下

- 50公噸及以上

- 死板的

- 50公噸以下

- 50至100公噸

- 101 - 150公噸

- 151 - 200公噸

- 201 - 250公噸

- 251 - 300公噸

- 300公噸以上

第6章:市場估計與預測:依驅動配置,2021 - 2034 年

- 主要趨勢

- 前輪驅動(FWD)

- 後輪驅動(RWD)

- 全輪驅動(AWD)

第7章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 電的

- 混合

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 礦業

- 建造

- 其他

第9章:市場估計與預測:按分銷管道,2021 - 2034 年

- 主要趨勢

- 直銷

- 分銷商/經銷商

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- Caterpillar

- Komatsu

- Liebherr

- Hitachi

- Volvo

- Scania

- Cummins

- Parker Hannifin

- Regional Champions

- John Deere

- SANY

- BelAZ

- XCMG

- Doosan Infracore

- Hyundai Construction Equipment

- Bell Equipment

- MAN Truck & Bus

- Terex

- Tadano

- 新興企業和科技顛覆者

- Autonomous Solutions (ASI)

- Modular Mining Systems

- Epiroc

- Sandvik Mining & Rock Solutions

- Kuhn Schweiz

- Allison Transmission

- Rio Tinto Technology & Innovation

The Global Dump Truck Market was valued at USD 21.9 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 55.2 billion by 2034.

The industry is undergoing a transformative shift fueled by growing interest in electrification and autonomous technologies. Rising pressure on manufacturers to reduce emissions and improve energy efficiency is pushing the development of electric dump trucks. At the same time, automation is gaining ground, with technologies that reduce operational errors, lower costs, and enable remote-controlled or fully autonomous fleet operations. These advances are reshaping traditional operating models, making way for cleaner, more intelligent, and cost-efficient transport solutions. While the industry once operated under linear supply chains and conventional workflows, the landscape shifted significantly after the COVID-19 pandemic. Previously marked by steady, incremental growth and minimal disruption, the market now responds to challenges in health, logistics, and workforce interaction, driving the need for digital transformation, innovation in vehicle functionality, and sustainable production. The evolving ecosystem demands a more agile approach, compelling manufacturers to shift from traditional design and production toward integrated, technology-driven business models that address safety, sustainability, and productivity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.9 Billion |

| Forecast Value | $55.2 billion |

| CAGR | 10.4% |

The articulated dump truck segment held a 58% share in 2024 and is expected to grow at a CAGR of 11% between 2025 and 2034. Articulated trucks are seeing continuous upgrades in payload capacity and off-road performance. With demand rising for trucks that can handle larger loads while maintaining flexibility across rugged and uneven surfaces, manufacturers are heavily investing in design innovation. Enhanced drivetrains, chassis modifications, and improved suspension systems are being implemented to accommodate the need for stability, adaptability, and better fuel economy under tough conditions. As infrastructure projects become more complex and are in challenging environments, articulated trucks offer the ideal solution for moving materials efficiently while maximizing safety and durability.

The construction segment held a 44% share in 2024 and is forecasted to grow at a CAGR of 11.7% through 2034. The construction industry's growing demand for highly specialized dump trucks is reshaping product development. Manufacturers are focusing on building models that address a wide range of construction needs, from compact units suited for urban developments to large-scale off-road models designed for expansive infrastructure projects. With the increasing variety of applications, companies are prioritizing versatility, fuel efficiency, and integration with telematics and load monitoring systems. As construction firms look for equipment tailored to specific tasks and environments, the demand for customized and high-performance dump trucks continues to surge.

China Dump Truck Market held a 45% share and generated USD 4.2 billion in 2024. China's aggressive push to expand its mining operations and scale domestic coal production to reduce import dependence has led to consistent demand for high-capacity dump trucks. The country's dominance in global steel manufacturing and its commanding role in rare earth metals production, where it controls most global output, have further accelerated the requirement for robust dump truck fleets. To support these industries, there has been increased investment in durable and heavy-duty vehicles capable of sustaining high-volume operations over prolonged periods, especially in challenging terrain.

Leading companies shaping the Global Dump Truck Market include Hitachi, BelAZ, Volvo, Scania, Cummins, SANY, Parker Hannifin, Caterpillar, Liebherr, and Komatsu. Top players in the dump truck industry are actively focusing on innovation, product diversification, and regional market penetration to strengthen their competitive position. Many are advancing toward electrification by developing battery-powered and hybrid models to meet global emission standards. Companies are also integrating digital tools, including GPS tracking, automated loading systems, and fleet management software, to enhance operational efficiency. Strategic collaborations with local distributors and infrastructure firms help increase brand presence and customer loyalty in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Drive Configuration

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Distribution Channels

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Manufacturer

- 3.1.1.3 Distributor

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure expansion fuels demand for dump trucks

- 3.2.1.2 Technological advancements enhance dump truck efficiency and safety

- 3.2.1.3 Government investments in transportation infrastructure spur demand

- 3.2.1.4 Mining sector growth boosts dump truck sales

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Economic downturns reduce construction and mining activities

- 3.2.2.2 Stringent emissions regulations increase manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric and hybrid dump trucks

- 3.2.3.2 Smart fleet management and telematics integration

- 3.2.1 Growth drivers

- 3.3 Technology Trends & Innovation Ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Autonomous systems development & implementation roadmap

- 3.3.1.2 Electric & hybrid powertrain evolution & market adoption

- 3.3.1.3 Telematics & IoT integration advances & data analytics

- 3.3.1.4 Predictive maintenance & AI applications development

- 3.3.2 Emerging technologies

- 3.3.2.1 Cybersecurity solutions & connected equipment protection

- 3.3.2.2 Blockchain integration & supply chain transparency

- 3.3.2.3 Augmented reality & virtual training system development

- 3.3.2.4 5G connectivity & real-time data processing applications

- 3.3.1 Current technologies

- 3.4 Regulatory landscape

- 3.4.1 Global emissions standards & environmental regulations

- 3.4.2 Mining safety regulations & MSHA compliance

- 3.4.3 Autonomous vehicle regulations & standards

- 3.4.4 International trade & tariff implications

- 3.4.5 Cybersecurity regulations & data protection

- 3.5 Aftermarket services & support ecosystem

- 3.5.1 Parts & components aftermarket analysis

- 3.5.2 Maintenance & repair services market

- 3.5.3 Training & certification programs market

- 3.5.4 Digital services & software solutions

- 3.6 Financing & leasing market analysis

- 3.6.1 Equipment financing market dynamics

- 3.6.2 Equipment leasing market analysis

- 3.6.3 Rental market & short-term solutions

- 3.6.4 Alternative financing solutions

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Environmental impact assessment & lifecycle analysis

- 3.10.2 Social impact & community relations

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable technological development

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Articulated

- 5.2.1 Below 50 Metric Tons

- 5.2.2 50 Metric Tons and above

- 5.3 Rigid

- 5.3.1 Below 50 metric tons

- 5.3.2 50 to 100 metric tons

- 5.3.3 101 - 150 metric tons

- 5.3.4 151 - 200 metric tons

- 5.3.5 201 - 250 metric tons

- 5.3.6 251 - 300 metric tons

- 5.3.7 Above 300 metric tons

Chapter 6 Market Estimates & Forecast, By Drive Configuration, 2021 - 2034 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Front-wheel drive (FWD)

- 6.3 Rear-wheel drive (RWD)

- 6.4 All-wheel drive (AWD)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($ Bn & Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Construction

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channels, 2021 - 2034 ($ Bn & Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Distributors/Dealers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn & Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Caterpillar

- 11.1.2 Komatsu

- 11.1.3 Liebherr

- 11.1.4 Hitachi

- 11.1.5 Volvo

- 11.1.6 Scania

- 11.1.7 Cummins

- 11.1.8 Parker Hannifin

- 11.2 Regional Champions

- 11.2.1 John Deere

- 11.2.2 SANY

- 11.2.3 BelAZ

- 11.2.4 XCMG

- 11.2.5 Doosan Infracore

- 11.2.6 Hyundai Construction Equipment

- 11.2.7 Bell Equipment

- 11.2.8 MAN Truck & Bus

- 11.2.9 Terex

- 11.2.10 Tadano

- 11.3 Emerging Players & Technology Disruptors

- 11.3.1 Autonomous Solutions (ASI)

- 11.3.2 Modular Mining Systems

- 11.3.3 Epiroc

- 11.3.4 Sandvik Mining & Rock Solutions

- 11.3.5 Kuhn Schweiz

- 11.3.6 Allison Transmission

- 11.3.7 Rio Tinto Technology & Innovation

2026年全球自動卸貨卡車市場報告

2026年全球自動卸貨卡車市場報告 鉸接式自動卸貨卡車市場:依驅動系統、負載容量、應用及銷售管道分類-2026-2032年全球市場預測自動卸貨卡車市場:按負載容量、推進系統和應用分類的全球預測,2026-2032年自動卸貨卡車市場:按車輛類型、負載容量、燃料類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測

鉸接式自動卸貨卡車市場:依驅動系統、負載容量、應用及銷售管道分類-2026-2032年全球市場預測自動卸貨卡車市場:按負載容量、推進系統和應用分類的全球預測,2026-2032年自動卸貨卡車市場:按車輛類型、負載容量、燃料類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測 自卸車車廂市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球鉸接式自動卸貨卡車輪胎市場報告全地形自動卸貨卡車市場按有效載荷能力、燃料類型、驅動類型、車輛類型、應用、最終用戶和銷售管道分類,全球預測,2026-2032年柴油動力鉸接式自動卸貨卡車市場(按載重能力、引擎功率、變速箱、底盤配置、輪胎類型、應用和銷售管道)——全球預測,2026-2032年自動卸貨卡車底盤市場按載重能力、傳動系統、動力傳動系統、車橋配置和應用分類-全球預測,2026-2032年

自卸車車廂市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球鉸接式自動卸貨卡車輪胎市場報告全地形自動卸貨卡車市場按有效載荷能力、燃料類型、驅動類型、車輛類型、應用、最終用戶和銷售管道分類,全球預測,2026-2032年柴油動力鉸接式自動卸貨卡車市場(按載重能力、引擎功率、變速箱、底盤配置、輪胎類型、應用和銷售管道)——全球預測,2026-2032年自動卸貨卡車底盤市場按載重能力、傳動系統、動力傳動系統、車橋配置和應用分類-全球預測,2026-2032年 礦用自動卸貨卡車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

礦用自動卸貨卡車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)