|

市場調查報告書

商品編碼

1833629

汽車駕駛艙域控制器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Cockpit Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

根據 Global Market Insights Inc. 發布的最新報告,2024 年全球汽車座艙控制器市場規模估計為 21.1 億美元,預計將從 2025 年的 23.9 億美元成長到 2034 年的 156 億美元,複合年成長率為 23.1%。

汽車製造商正在從多個獨立的ECU轉向集中式駕駛艙域控制器,從而簡化軟體架構並降低複雜性。這種整合不僅減少了佈線和重量,還簡化了資訊娛樂、儀表板和空調系統的更新和診斷。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 21.1億美元 |

| 預測值 | 156億美元 |

| 複合年成長率 | 23.1% |

硬體採用率不斷上升

2024年,汽車座艙域控制器市場的硬體部分佔據了相當大的佔有率,這得益於專注於提供強大且節能的處理器的創新,這些處理器能夠同時管理複雜的資訊娛樂、互聯和安全功能。該部分透過將先進的SoC、GPU和高速通訊介面整合到緊湊、散熱最佳化的模組中,以適應汽車級環境,從而推動成長。隨著對即時處理和多任務處理能力的需求不斷成長,硬體供應商優先考慮模組化設計和可擴展架構,以滿足多樣化的車輛需求,確保下一代智慧座艙的可靠性和性能。

乘用車將獲得發展動力

2024年,乘用車市場收入可觀,這得益於消費者對增強用戶體驗、互聯互通和安全性的期望不斷提升。原始設備製造商正大力投資整合式智慧座艙,透過語音識別、多螢幕顯示設定和人工智慧助理提供無縫交互,所有這些都由強大的網域控制器進行協調。這反映出一個明顯的趨勢:更聰明、更互聯的內裝將重新定義駕駛體驗。

亞太地區將成為利潤豐厚的地區

亞太地區是汽車座艙控制器市場的主要成長引擎,其驅動力來自快速的城市化進程、汽車產量的不斷成長以及消費者對先進車載技術日益成長的需求。在政府推動電動車和數位轉型的舉措的支持下,中國、日本、韓國和印度等國家正在大力投資智慧汽車技術。市場成長的動力源於本地製造能力以及全球供應商與區域汽車製造商之間的緊密合作,這些合作旨在滿足日益成長的互聯智慧座艙解決方案需求。

汽車座艙控制器市場的主要參與者有偉世通、NVIDIA、羅伯特·博世、高通技術、Aptiv、HARMAN、Denso、英特爾、佛吉亞和大陸集團。

為了鞏固市場地位,汽車座艙域控制器領域的企業正專注於多項策略措施。這些措施包括投資研發,開發整合人工智慧、擴增實境和5G連接等新興技術的可擴展高效能平台。許多企業正在與原始設備製造商(OEM)和軟體開發商建立合作夥伴關係或合資企業,共同打造針對特定車型和地區的客製化解決方案。此外,擴大區域製造業務,尤其是在亞太地區,可以加快交貨速度並提升成本優勢。企業也強調網路安全功能和無線更新功能,以滿足不斷變化的安全標準和消費者期望,從而在這個競爭激烈、快速發展的市場中站穩腳跟。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 對連網和軟體定義汽車的需求不斷成長

- 向集中式電子電氣車輛架構過渡

- 消費者對高級資訊娛樂和數位駕駛艙體驗的需求不斷成長

- 電動車和自動駕駛汽車的成長

- OEM一級廠商與半導體和軟體廠商的合作

- 產業陷阱與挑戰

- 高整合和軟體驗證成本

- 網路安全與資料隱私風險

- 市場機會

- 擴展雲端與 OTA 更新生態系統

- 新興市場(亞太地區、拉丁美洲地區、中東和非洲地區)滲透率不斷提高

- 先進的 HMI 和多模式互動系統

- 與行動服務和車隊應用程式整合

- 成長動力

- 成長潛力分析

- 監管和標準格局

- 全球監理框架分析

- 功能安全標準及實施

- 區域監管差異和合規性

- 合規成本分析及實施策略

- 波特的分析

- PESTEL分析

- 技術與創新格局

- 當前的技術趨勢

- 硬體技術成熟度

- 軟體平台準備就緒

- 整合複雜性評估

- 未來技術路線圖

- 硬體發展時程和里程碑

- 軟體平台發展路線圖

- 新興技術整合計劃

- 標準演進和行業影響

- AUTOSAR自適應平台演進

- ISO 26262更新與安全影響

- 網路安全標準路線圖

- 3.6.1 區域

- 當前的技術趨勢

- 成本結構分析與商業案例框架

- 總擁有成本(TCO)分析

- ROI 模型與報酬分析

- 定價策略分析和基準測試

- 各細分市場的投資需求

- 專利分析

- 永續性和ESG影響評估

- 環境影響分析和指標

- 社會影響考量與指標

- 治理與合規框架

- ESG 投資影響與財務影響

- 用例和應用

- 最佳情況

- 供應鏈情報與風險評估

- 全球供應鏈映射與分析

- 半導體供應鏈深度探究

- 地緣政治風險評估

- 供應鏈彈性與最佳化策略

- 智慧財產權和專利狀況

- 專利申請趨勢與創新分析

- 主要專利持有者及智慧財產權策略分析

- IP貨幣化機會和策略

- 自由營運和知識產權風險管理

- 市場進入策略框架

- 市場進入策略分析

- 客戶區隔與目標策略

- 通路策略與合作夥伴生態系統

- 行銷和銷售效率

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依組件分類,2021 - 2034 年

- 主要趨勢

- 硬體

- 系統

- 模組

- 記憶

- 連接性

- 模組

- 顯示介面

- 網路攝影機和感測器

- 其他(電源管理IC、HUD)

- 系統

- 軟體

- 服務

第6章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車

- 中型商用車

- 重型商用車

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 集中式架構

- 分散式架構

- 區域架構

- 混合架構

第 8 章:市場估計與預測:按銷售管道,2021 年至 2034 年

- 主要趨勢

- 原始設備製造商(OEM)管道

- 售後頻道

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 資訊娛樂系統

- 數位儀表板

- 人機介面(hmi)

- 平視顯示器 (hud) 整合

- 駕駛員監控系統

- 氣候控制與舒適系統

- 高級應用程式和新興用例

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- Aptiv

- Continental

- Denso

- HARMAN International Industries

- Intel

- NVIDIA

- Qualcomm Technologies

- Robert Bosch

- STMicroelectronics

- Texas Instruments

- Visteon

- Valeo

- 區域參與者

- Alpine Electronics

- Faurecia

- Hyundai Mobis

- Infineon Technologies

- LG Electronics

- Magna International

- NXP Semiconductors

- Panasonic

- Sony

- 新興參與者/顛覆者

- Analog Devices

- Black Sesame Technologies

- BYD Company

- ECARX Holdings

- Horizon Robotics

- Huawei Technologies

- MediaTek

- Renesas Electronics

- Tesla

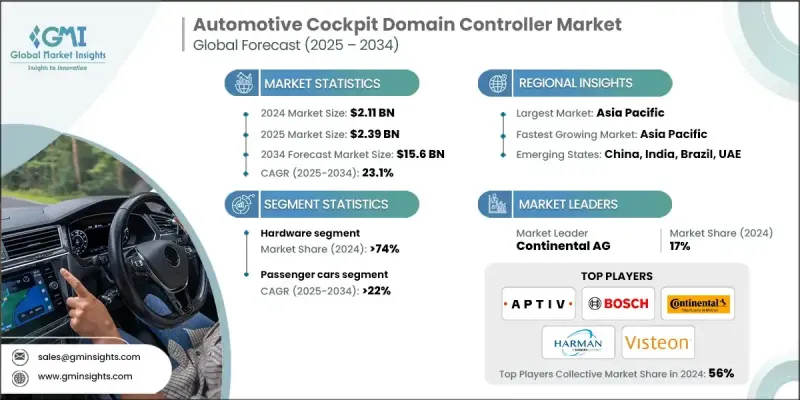

The global automotive cockpit domain controller market was estimated at USD 2.11 billion in 2024 and is expected to grow from USD 2.39 billion in 2025 to USD 15.6 billion by 2034, at a CAGR of 23.1%, according to the latest report published by Global Market Insights Inc.

Automakers are shifting from multiple standalone ECUs to centralized cockpit domain controllers, streamlining software architecture and reducing complexity. This consolidation not only cuts down on wiring and weight but also simplifies updates and diagnostics across infotainment, instrument clusters, and climate systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.11 Billion |

| Forecast Value | $15.6 Billion |

| CAGR | 23.1% |

Rising Adoption in Hardware

The hardware segment from the automotive cockpit domain controller market held a significant share in 2024, driven by innovation focusing on delivering powerful and energy-efficient processors capable of managing complex infotainment, connectivity, and safety features simultaneously. This segment drives growth by integrating advanced SoCs, GPUs, and high-speed communication interfaces into compact, thermally optimized modules designed to withstand automotive-grade conditions. With increasing demand for real-time processing and multitasking capabilities, hardware suppliers are prioritizing modular designs and scalable architectures to meet diverse vehicle requirements, ensuring reliability and performance in next-generation smart cockpits.

Passenger Cars to Gain Traction

The passenger cars segment generated notable revenues in 2024, fueled by rising consumer expectations for enhanced user experiences, connectivity, and safety. OEMs are investing heavily in integrating smart cockpits that offer seamless interaction through voice recognition, multi-display setups, and AI-powered assistants, all orchestrated by robust domain controllers. This reflects a clear trend toward smarter, more connected interiors that redefine the driving experience.

Asia Pacific to Emerge as a Lucrative Region

Asia Pacific stands as a key growth engine in the automotive cockpit domain controller market, driven by rapid urbanization, increasing vehicle production, and expanding consumer demand for advanced in-car technologies. Countries like China, Japan, South Korea, and India are investing heavily in smart vehicle technologies, supported by government initiatives promoting electric mobility and digital transformation. The market growth is propelled by local manufacturing capabilities and strong collaborations between global suppliers and regional automakers seeking to capture the rising demand for connected, intelligent cockpit solutions.

Major players in the automotive cockpit domain controller market are Visteon, NVIDIA, Robert Bosch, Qualcomm Technologies, Aptiv, HARMAN, Denso, Intel, Faurecia, and Continental.

To strengthen their market position, companies in the automotive cockpit domain controller space are focusing on several strategic initiatives. These include investing in R&D to develop scalable, high-performance platforms integrate emerging technologies such as AI, AR, and 5G connectivity. Many firms are forging partnerships and joint ventures with OEMs and software developers to co-create customized solutions tailored to specific vehicle models and regions. Additionally, expanding regional manufacturing footprints, particularly in the Asia Pacific, enables faster delivery and cost advantages. Companies also emphasize cybersecurity features and over-the-air update capabilities to meet evolving safety standards and consumer expectations, securing their foothold in this competitive and rapidly evolving market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for connected and software-defined vehicles

- 3.2.1.2 Transition toward centralized e/e vehicle architecture

- 3.2.1.3 Increasing consumer demand for advanced infotainment & digital cockpit experiences

- 3.2.1.4 Growth of EVs and autonomous vehicles

- 3.2.1.5 OEM-tier 1 collaborations with semiconductor & software players

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High integration & software validation costs

- 3.2.2.2 Cybersecurity and data privacy risks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of cloud-enabled and OTA update ecosystems

- 3.2.3.2 Growing penetration in emerging markets (APAC, LATAM, MEA)

- 3.2.3.3 Advanced HMI & multimodal interaction systems

- 3.2.3.4 Integration with mobility services and fleet applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory and standards landscape

- 3.4.1 Global regulatory framework analysis

- 3.4.2 Functional safety standards and implementation

- 3.4.3 Regional regulatory variations and compliance

- 3.4.4 Compliance cost analysis and implementation strategy

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology & innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Hardware technology maturity

- 3.7.1.2 Software platform readiness

- 3.7.1.3 Integration complexity assessment

- 3.7.2 Future technology roadmap

- 3.7.2.1 Hardware evolution timeline and milestones

- 3.7.2.2 Software platform development roadmap

- 3.7.2.3 Emerging technology integration schedule

- 3.7.3 Standards evolution and industry impact

- 3.7.3.1 Autosar adaptive platform evolution

- 3.7.3.2 Iso 26262 updates and safety implications

- 3.7.3.3 Cybersecurity standards roadmap

- 3.7.1 Current technological trends

- 3.8 Cost structure analysis and business case framework

- 3.8.1 Total cost of ownership (TCO) analysis

- 3.8.2 ROI models and payback analysis

- 3.8.3 Pricing strategy analysis and benchmarking

- 3.8.4 Investment requirements by market segment

- 3.9 Patent analysis

- 3.10 Sustainability and esg impact assessment

- 3.10.1 Environmental impact analysis and metrics

- 3.10.2 Social impact considerations and metrics

- 3.10.3 Governance and compliance framework

- 3.10.4 Esg investment implications and financial impact

- 3.11 Use cases and applications

- 3.12 Best-case scenario

- 3.13 Supply chain intelligence and risk assessment

- 3.13.1 Global supply chain mapping and analysis

- 3.13.2 Semiconductor supply chain deep dive

- 3.13.3 Geopolitical risk assessment

- 3.13.4 Supply chain resilience and optimization strategies

- 3.14 Intellectual property and patent landscape

- 3.14.1 Patent filing trends and innovation analysis

- 3.14.2 Key patent holders and ip strategy analysis

- 3.14.3 Ip monetization opportunities and strategies

- 3.14.4 Freedom to operate and ip risk management

- 3.15 Go-to-market strategy framework

- 3.15.1 Market entry strategy analysis

- 3.15.2 Customer segmentation and targeting strategy

- 3.15.3 Channel strategy and partner ecosystem

- 3.15.4 Marketing and sales effectiveness

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 System on chip

- 5.2.1.1 Modules

- 5.2.1.1.1 Memory

- 5.2.1.1.2 Connectivity

- 5.2.1.1 Modules

- 5.2.2 Display interfaces

- 5.2.3 Camera & sensors

- 5.2.4 Others (power management IC, HUD)

- 5.2.1 System on chip

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Centralized architecture

- 7.3 Distributed architecture

- 7.4 Zonal architecture

- 7.5 Hybrid architecture

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Original equipment manufacturer (oem) channel

- 8.3 Aftermarket channel

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Infotainment systems

- 9.3 Digital instrument cluster

- 9.4 Human machine interface (hmi)

- 9.5 Head-up display (hud) integration

- 9.6 Driver monitoring systems

- 9.7 Climate control and comfort systems

- 9.8 Advanced applications and emerging use cases

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 HARMAN International Industries

- 11.1.5 Intel

- 11.1.6 NVIDIA

- 11.1.7 Qualcomm Technologies

- 11.1.8 Robert Bosch

- 11.1.9 STMicroelectronics

- 11.1.10 Texas Instruments

- 11.1.11 Visteon

- 11.1.12 Valeo

- 11.2 Regional Players

- 11.2.1 Alpine Electronics

- 11.2.2 Faurecia

- 11.2.3 Hyundai Mobis

- 11.2.4 Infineon Technologies

- 11.2.5 LG Electronics

- 11.2.6 Magna International

- 11.2.7 NXP Semiconductors

- 11.2.8 Panasonic

- 11.2.9 Sony

- 11.3 Emerging Players/Disruptors

- 11.3.1 Analog Devices

- 11.3.2 Black Sesame Technologies

- 11.3.3 BYD Company

- 11.3.4 ECARX Holdings

- 11.3.5 Horizon Robotics

- 11.3.6 Huawei Technologies

- 11.3.7 MediaTek

- 11.3.8 Renesas Electronics

- 11.3.9 Tesla