|

市場調查報告書

商品編碼

1833620

電動工具市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Power Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

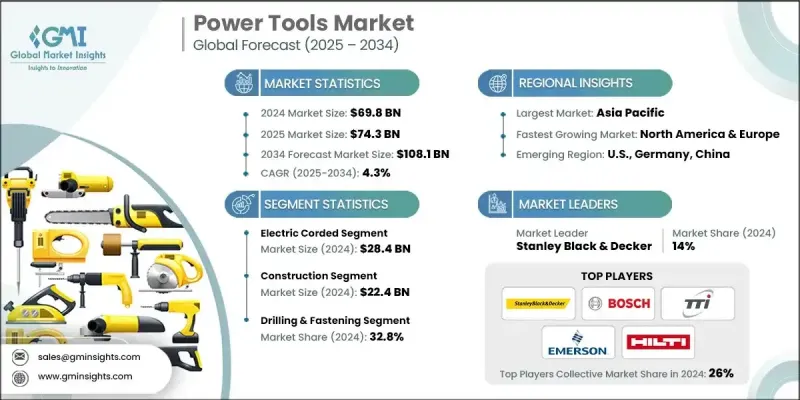

2024 年全球電動工具市場價值為 698 億美元,預計將以 4.3% 的複合年成長率成長,到 2034 年達到 1,081 億美元。

在城鎮化、人口成長以及政府加大基礎建設投資的推動下,全球建築業正穩步擴張。從大型公共交通系統和道路,到高層建築和工業園區,建築活動正在蓬勃發展,尤其是在亞太地區、拉丁美洲和中東地區的新興經濟體。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 698億美元 |

| 預測值 | 1081億美元 |

| 複合年成長率 | 4.3% |

電動有線工具的普及率不斷上升

2024年,有線電動工具憑藉其可靠性、穩定的功率輸出以及對重型任務的適應性,佔據了顯著的市場佔有率。儘管無線工具發展迅速,但有線工具仍然是在固定場所工作的專業人士的首選,因為在這些場所,不間斷的表現至關重要。該領域的製造商正在提升產品的人體工學、安全性能和能源效率,以保持競爭力,同時滿足不斷變化的最終用戶期望。

建築業需求不斷成長

受持續城鎮化、大規模基礎設施建設和住宅需求的推動,建築業在2024年將佔據顯著佔有率。鋸、鑽、磨機和釘槍等電動工具對於商業和住宅項目的框架搭建、安裝和裝修工作至關重要。主要參與者瞄準這一領域,推出了堅固耐用、性能卓越、防塵性能更強、電池續航時間和工具連接性更強的工具,從而提高施工現場的生產力和工人安全。

鑽孔和緊固以獲得牽引力

2024年,鑽孔和緊固工具市場佔據了相當大的佔有率。其應用範圍從基本的房屋維修到複雜的裝配線和基礎設施安裝。精密工程、更輕巧的外形尺寸以及無刷馬達整合推動了市場的成長。領先的公司專注於開發能夠處理各種表面和材料的多功能工具,並添加扭矩控制和數位監控等智慧功能,以提高用戶的準確性和控制力。

亞太地區將崛起成為推動力地區

2024年,亞太地區電動工具市場收入可觀,這得益於快速的工業化進程、蓬勃發展的建築業以及中國、印度和東南亞等國家不斷成長的消費支出。本地和全球製造商正在該地區擴大生產設施,建立更強大的分銷網路,並推出符合當地需求的經濟實惠的產品線。積極的定價策略、在地化的品牌建立和售後支援也有助於品牌建立長期的市場影響力。

電動工具市場的主要參與者有 Chervon Trading、Ingersoll-Rand、Festool、Makita、Emerson Electric、Hilti、Apex Tool Group、Bosch、Hikoki(原 Hitachi Koki)、Snap-on、Enerpac Tool Group、Andreas Stihl、Atlas Copco、Techtronic Industries (Toki) 和 Stantronley 和 Stantronley (Toki) 和 Stantronic (Toki)。

為了鞏固市場地位,電動工具領域的公司正在利用創新、策略合作夥伴關係和以客戶為中心的產品開發。無線技術是一大重點,各大品牌大力投資電池效率、快速充電系統以及適用於多種工具的通用電池平台。許多品牌還採用了應用程式整合、使用情況追蹤和物聯網等智慧功能,以在競爭激烈的市場中脫穎而出。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 建築和基礎設施活動不斷增加

- 快速工業化

- DIY 和家居裝修的成長

- 技術進步

- 產業陷阱與挑戰

- 仿冒品

- 激烈的競爭和價格壓力

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按工具類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按模式,2021 - 2034

- 主要趨勢

- 電動有線

- 電動無線

- 氣動

第6章:市場估計與預測:按工具類型,2021 - 2034 年

- 主要趨勢

- 鑽孔和緊固

- 鋸切和切割工具

- 拆除

- 材料去除

- 扳手

- 其他

第7章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 建造

- 汽車

- 航太

- 能源

- 電子產品

- DIY

- 其他

第 8 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直接的

- 間接

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Andreas Stihl

- Apex Tool Group

- Atlas Copco

- Chervon Trading

- Emerson Electric

- Enerpac Tool Group

- Hilti

- Hikoki (formerly Hitachi Koki)

- Ingersoll-Rand

- Makita

- Bosch

- Snap-on

- Stanley Black & Decker

- Techtronic Industries (TTI)

- Festool

The Global Power Tools Market was valued at USD 69.8 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 108.1 billion by 2034.

The global construction sector is witnessing steady expansion, fueled by urbanization, population growth, and increasing government investments in infrastructure development. From large-scale public transit systems and roadways to high-rise buildings and industrial zones, construction activity is surging, particularly in emerging economies across Asia Pacific, Latin America, and the Middle East.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $69.8 Billion |

| Forecast Value | $108.1 Billion |

| CAGR | 4.3% |

Rising Adoption of Electric Corded Tools

The electric corded segment held a notable share in 2024 owing to its reliability, consistent power output, and suitability for heavy-duty tasks. While cordless tools are growing rapidly, corded tools remain a preferred choice for professionals working in fixed locations where uninterrupted performance is critical. Manufacturers in this space are enhancing product ergonomics, safety features, and energy efficiency to remain competitive while addressing evolving end-user expectations.

Increasing Demand in Construction

The construction segment generated a significant share in 2024, driven by ongoing urbanization, large-scale infrastructure development, and residential housing demand. Power tools such as saws, drills, grinders, and nailers are essential for framing, installation, and finishing work across both commercial and residential projects. Key players are targeting this sector by introducing rugged, high-performance tools with improved dust protection, battery runtime, and tool connectivity-allowing for better job site productivity and worker safety.

Drilling and Fastening to Gain Traction

The drilling and fastening tools segment held a sizeable share in 2024. Applications range from basic home repairs to complex assembly lines and infrastructure installations. Market growth is driven by precision engineering, lighter form factors, and brushless motor integration. Leading companies are focusing on multi-functional tools that can handle diverse surfaces and materials, as well as adding smart features like torque control and digital monitoring to improve user accuracy and control.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific power tools market generated substantial revenues in 2024, fueled by rapid industrialization, booming construction sectors, and increasing consumer spending in countries like China, India, and Southeast Asia. Local and global manufacturers are expanding production facilities in the region, establishing stronger distributor networks, and launching budget-friendly product lines tailored to local needs. Aggressive pricing strategies, localized branding, and after-sales support are also helping brands build long-term market presence.

Major players in the power tools market are Chervon Trading, Ingersoll-Rand, Festool, Makita, Emerson Electric, Hilti, Apex Tool Group, Bosch, Hikoki (formerly Hitachi Koki), Snap-on, Enerpac Tool Group, Andreas Stihl, Atlas Copco, Techtronic Industries (TTI), and Stanley Black & Decker.

To strengthen their market position, companies in the power tools space are leveraging innovation, strategic partnerships, and customer-centric product development. A major focus is on cordless technology, with brands investing heavily in battery efficiency, quick-charging systems, and universal battery platforms across multiple tools. Many are also adopting smart features such as app integration, usage tracking, and IoT capabilities to differentiate in a crowded marketplace.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Mode

- 2.2.3 Tool type

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising construction and infrastructure activities

- 3.2.1.2 Rapid industrialization

- 3.2.1.3 Growth in DIY and home improvement

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Counterfeit and low-quality products

- 3.2.2.2 Intense competition and price pressure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By tool type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Mode, 2021 - 2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Electric corded

- 5.3 Electric cordless

- 5.4 Pneumatic

Chapter 6 Market Estimates & Forecast, By Tool type, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Drilling & fastening

- 6.3 Sawing & cutting tools

- 6.4 Demolition

- 6.5 Material removal

- 6.6 Wrenches

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automotive

- 7.4 Aerospace

- 7.5 Energy

- 7.6 Electronics

- 7.7 DIY

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Andreas Stihl

- 10.2 Apex Tool Group

- 10.3 Atlas Copco

- 10.4 Chervon Trading

- 10.5 Emerson Electric

- 10.6 Enerpac Tool Group

- 10.7 Hilti

- 10.8 Hikoki (formerly Hitachi Koki)

- 10.9 Ingersoll-Rand

- 10.10 Makita

- 10.11 Bosch

- 10.12 Snap-on

- 10.13 Stanley Black & Decker

- 10.14 Techtronic Industries (TTI)

- 10.15 Festool

2026年全球電動啃咬機市場報告

2026年全球電動啃咬機市場報告 工業有線電動螺絲起子市場預測至2034年-按類型、應用、最終用戶和地區分類的全球分析

工業有線電動螺絲起子市場預測至2034年-按類型、應用、最終用戶和地區分類的全球分析 清潔電動工具市場:2026-2032年全球市場預測(依產品類型、動力來源、最終用戶、應用及銷售管道)精密螺絲起子市場:按產品類型、驅動系統、最終用戶、應用和銷售管道分類 - 全球預測 2026-2032電動沖孔機市場:按類型、移動式、額定功率、爪型、應用和分銷管道分類-全球預測,2026-2032年全自動壓接機市場:依機器類型、電纜材料、產能、應用、終端用戶產業和銷售管道-全球預測,2026-2032年電動工具市場:按工具類型、類別、馬達類型、最終用戶產業和銷售管道- 全球預測 2026-2032

清潔電動工具市場:2026-2032年全球市場預測(依產品類型、動力來源、最終用戶、應用及銷售管道)精密螺絲起子市場:按產品類型、驅動系統、最終用戶、應用和銷售管道分類 - 全球預測 2026-2032電動沖孔機市場:按類型、移動式、額定功率、爪型、應用和分銷管道分類-全球預測,2026-2032年全自動壓接機市場:依機器類型、電纜材料、產能、應用、終端用戶產業和銷售管道-全球預測,2026-2032年電動工具市場:按工具類型、類別、馬達類型、最終用戶產業和銷售管道- 全球預測 2026-2032 電動工具市場分析及預測(至2035年):依類型、產品、技術、應用、最終用戶、組件、部署模式、功能、安裝類型及設備分類

電動工具市場分析及預測(至2035年):依類型、產品、技術、應用、最終用戶、組件、部署模式、功能、安裝類型及設備分類 全球電動工具市場規模、佔有率、趨勢和成長分析報告(2026-2034年)牆體開槽機全球市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球電動工具市場規模、佔有率、趨勢和成長分析報告(2026-2034年)牆體開槽機全球市場規模、佔有率、趨勢和成長分析報告:2026-2034年