|

市場調查報告書

商品編碼

1833442

HVAC 感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測HVAC Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

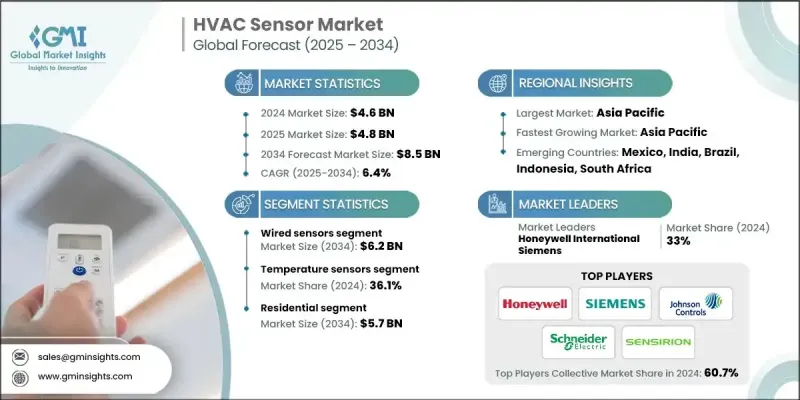

2024 年全球 HVAC 感測器市場價值為 46 億美元,預計到 2034 年將以 6.4% 的複合年成長率成長至 85 億美元。

隨著人們對室內空氣品質的日益重視,以及住宅環境中暖通空調系統 (HVAC) 的日益普及,先進感測器技術的需求持續成長。越來越多的業主和設施營運商開始使用多功能感測器來即時監測溫度、濕度、二氧化碳濃度、顆粒物和揮發性有機化合物。消費者對健康、舒適度和空氣品質的意識不斷增強,以及注重環境安全的監管框架也推動了這一轉變。隨著暖通空調系統日益先進和互聯互通,商業、工業和住宅領域對用於確保空氣品質和能源效率的精密感測器的需求正在不斷成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 46億美元 |

| 預測值 | 85億美元 |

| 複合年成長率 | 6.4% |

預計到2034年,有線感測器市場規模將達到62億美元,憑藉其可靠性、穩定的性能和資料完整性,在大型工業和商業領域保持主導地位。儘管無線替代方案日益受到青睞,但在無縫通訊和最低延遲至關重要的關鍵任務環境中,有線配置仍然備受青睞。製造商目前正致力於提升安裝便利性,並將有線感測器更有效地整合到集中控制基礎設施中,同時又不損害其核心性能優勢。

2024年,溫度感測器市場佔有36.1%的佔有率。它們與智慧暖通空調系統的整合日益複雜,通常整合在多功能設備中,這些設備還能偵測濕度、二氧化碳和空氣污染物。這些先進的溫度感測器在智慧氣候調節中發揮著至關重要的作用,可以即時調節氣流和溫度,從而提高舒適度並降低能耗。隨著互聯建築的發展,符合物聯網協定的緊湊型高精度感測器正受到製造商和最終用戶的青睞。

2024年,北美暖通空調感測器市場佔據27%的市場佔有率,預計到2034年將以6.6%的複合年成長率成長。該地區強勁的成長勢頭得益於對節能暖通空調設備日益成長的需求以及智慧建築生態系統的蓬勃發展。北美多參數感測器的使用正在穩步改變住宅和商業物業的空氣管理策略,使自動化、數據驅動的暖通空調系統能夠提高合規性和居住者的健康水平。

暖通空調感測器市場的主要參與者包括西門子、江森自控、霍尼韋爾國際、盛思銳和施耐德電機。暖通空調感測器產業的領先公司正在透過開發緊湊型多功能感測器解決方案來提升其市場地位,以滿足日益成長的即時監控和智慧暖通空調整合需求。這些公司正在大力投入研發,以打造節能、相容物聯網的感測器,將溫度、濕度和空氣品質檢測功能整合在一個模組中。與智慧建築系統供應商的合作以及對互通性和資料分析的更多關注,有助於提升整個系統的效能並簡化部署。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 醫療保健和製藥行業對客製化 HVAC 解決方案的需求不斷成長

- 智慧家庭和建築自動化的普及率不斷提高

- 室內空氣品質(IAQ)監測日益受到關注

- 住宅領域暖通空調系統安裝量不斷上升

- 資料中心建置激增推動冷卻需求

- 產業陷阱與挑戰

- 初期投資和安裝成本高

- 與現有 HVAC 系統整合的複雜性

- 市場機會

- 智慧互聯建築需求不斷成長

- 能源效率法規和標準

- 舊式 HVAC 系統的改造與升級

- 與建築管理系統 (BMS) 整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- 溫度感測器

- 濕度感測器

- 壓力感測器

- 煙霧和氣體感測器

- 運動感應器

- 其他

第6章:市場估計與預測:按連結類型,2021 - 2034 年

- 主要趨勢

- 有線感應器

- 無線感測器

第7章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 住宅

- 商業的

- 工業的

第8章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 全球關鍵參與者

- Honeywell International

- Siemens

- Johnson Controls

- TE Connectivity

- Schneider Electric

- 區域關鍵參與者

- 北美洲

- Emerson Electric

- Trane

- Amphenol

- 歐洲

- Belimo Holding

- STMicroelectronics

- Infineon Technologies

- 亞太地區

- Omron

- Chino

- Acal Bfi

- 北美洲

- 利基市場參與者/顛覆者

- Sensirion

- Sensata Technologies

- Microchip Technology

- Greystone Energy Systems

- Texas Instruments

The Global HVAC Sensor Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 8.5 billion by 2034.

Increasing emphasis on indoor air quality, coupled with growing HVAC system installations in residential environments, continues to fuel demand for advanced sensor technologies. A growing number of property owners and facility operators are turning to multi-functional sensor units to monitor temperature, humidity, carbon dioxide levels, particulate matter, and volatile organic compounds in real time. This shift is being driven by heightened consumer awareness around health, comfort, and air quality, as well as regulatory frameworks focused on environmental safety. As HVAC systems become more advanced and interconnected, the demand for precision sensors that ensure air quality and energy efficiency is rising across commercial, industrial, and residential sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 6.4% |

The wired sensors segment is predicted to generate USD 6.2 billion by 2034, maintaining its dominance in large-scale industrial and commercial spaces due to its reliability, consistent performance, and data integrity. While wireless alternatives are gaining traction, wired configurations continue to be favored in mission-critical environments where seamless communication and minimal latency are key. Manufacturers are now focusing on enhancing installation convenience and integrating wired sensors more effectively into centralized control infrastructures without compromising their core performance advantages.

The temperature sensors segment held a 36.1% share in 2024. Their integration into smart HVAC systems is becoming more sophisticated, often packaged within multi-functional devices that also detect humidity, CO2, and air pollutants. These advanced temperature sensors play a crucial role in intelligent climate regulation, adapting airflow and temperature in real-time to improve comfort and reduce energy usage. As connected buildings evolve, compact, high-accuracy sensors that align with IoT protocols are gaining favor among manufacturers and end-users alike.

North America HVAC Sensor Market held 27% share in 2024 and is projected to grow at a CAGR of 6.6% through 2034. The region's strong momentum is driven by rising demand for energy-efficient HVAC installations and the proliferation of smart building ecosystems. The use of multi-parameter sensors in North America is steadily transforming air management strategies across residential and commercial properties, enabling automated, data-driven HVAC systems that improve compliance and occupant well-being.

Key players operating in the HVAC Sensor Market include Siemens, Johnson Controls, Honeywell International, Sensirion, and Schneider Electric. Leading companies in the HVAC sensor industry are advancing their market position by developing compact, multi-functional sensor solutions that align with the growing need for real-time monitoring and smart HVAC integration. These firms are investing heavily in R&D to create energy-efficient, IoT-compatible sensors that combine temperature, humidity, and air quality detection in a single module. Partnerships with smart building system providers and increased focus on interoperability and data analytics help enhance system-wide performance and simplify deployment.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Connectivity type trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising need for customized HVAC solutions in healthcare and pharmaceuticals

- 3.2.1.2 Growing adoption of smart homes and building automation

- 3.2.1.3 Rising focus on indoor air quality (IAQ) monitoring

- 3.2.1.4 Rising HVAC system installations in residential sector

- 3.2.1.5 Surge in data center construction driving cooling demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and installation costs

- 3.2.2.2 Complexity in integration with existing HVAC systems

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for smart and connected buildings

- 3.2.3.2 Energy efficiency regulations and standards

- 3.2.3.3 Retrofit and upgradation of legacy HVAC systems

- 3.2.3.4 Integration with building management systems (BMS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Temperature sensors

- 5.3 Humidity sensors

- 5.4 Pressure sensors

- 5.5 Smoke & gas sensors

- 5.6 Motion sensors

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Connectivity Type, 2021 - 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Wired sensors

- 6.3 Wireless sensors

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Honeywell International

- 9.1.2 Siemens

- 9.1.3 Johnson Controls

- 9.1.4 TE Connectivity

- 9.1.5 Schneider Electric

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Emerson Electric

- 9.2.1.2 Trane

- 9.2.1.3 Amphenol

- 9.2.2 Europe

- 9.2.2.1 Belimo Holding

- 9.2.2.2 STMicroelectronics

- 9.2.2.3 Infineon Technologies

- 9.2.3 APAC

- 9.2.3.1 Omron

- 9.2.3.2 Chino

- 9.2.3.3 Acal Bfi

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Sensirion

- 9.3.2 Sensata Technologies

- 9.3.3 Microchip Technology

- 9.3.4 Greystone Energy Systems

- 9.3.5 Texas Instruments

暖通空調控制市場報告:按組件、部署模式、系統、最終用戶和地區分類(2026-2034 年)

暖通空調控制市場報告:按組件、部署模式、系統、最終用戶和地區分類(2026-2034 年) 暖通空調系統感測器市場報告:趨勢、預測和競爭分析(至2035年)

暖通空調系統感測器市場報告:趨勢、預測和競爭分析(至2035年) 手持式暖通空調監測設備市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終使用者、功能、安裝類型及設備分類暖通空調控制市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類

手持式暖通空調監測設備市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終使用者、功能、安裝類型及設備分類暖通空調控制市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類 智慧暖通空調控制市場:機會、成長要素、產業趨勢分析及2026年至2035年預測

智慧暖通空調控制市場:機會、成長要素、產業趨勢分析及2026年至2035年預測 2026年全球暖氣、通風和空調控制系統市場報告2026年全球暖氣、通風和空調(HVAC)控制系統市場報告

2026年全球暖氣、通風和空調控制系統市場報告2026年全球暖氣、通風和空調(HVAC)控制系統市場報告 HVAC控制系統市場規模、佔有率和成長分析(按系統、組件、部署類型、應用和地區分類)-產業預測(2026-2033年)

HVAC控制系統市場規模、佔有率和成長分析(按系統、組件、部署類型、應用和地區分類)-產業預測(2026-2033年) 全球智慧暖通空調系統市場:市場規模、佔有率、趨勢分析(按技術、應用、分銷管道和地區分類)、細分市場預測(2025-2033年)

全球智慧暖通空調系統市場:市場規模、佔有率、趨勢分析(按技術、應用、分銷管道和地區分類)、細分市場預測(2025-2033年) HVAC 控制市場(按產品類型、連接性、安裝、最終用戶和分銷管道)- 全球預測 2025-2032

HVAC 控制市場(按產品類型、連接性、安裝、最終用戶和分銷管道)- 全球預測 2025-2032