|

市場調查報告書

商品編碼

1833435

汽車訂閱服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Vehicle Subscription Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

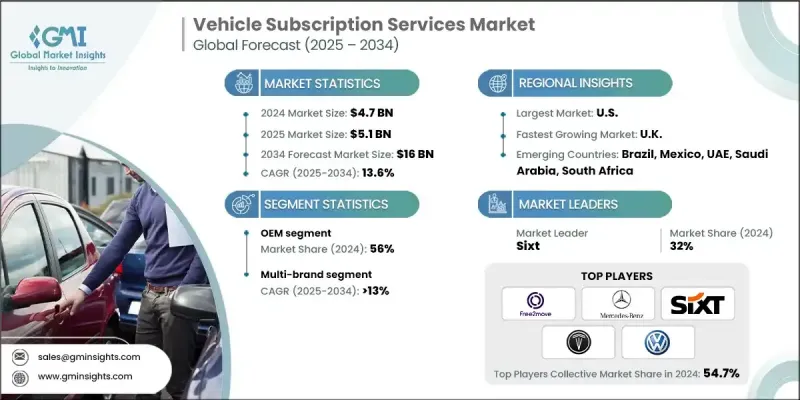

2024 年全球汽車訂閱服務市場價值為 47 億美元,預計到 2034 年將以 13.6% 的複合年成長率成長至 160 億美元。

消費者正從傳統的汽車所有權轉向更靈活、更方便的出行方式。這種轉變源自於他們希望避免購買或租賃汽車所帶來的長期財務和維護成本。汽車訂閱服務讓使用者能夠根據需要使用不同類型的車輛,無論是日常通勤、週末出行還是特殊場合,而無需承擔擁有車輛的麻煩。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 47億美元 |

| 預測值 | 160億美元 |

| 複合年成長率 | 13.6% |

OEM獲得發展動力

2024年, OEM在汽車訂閱服務市場中佔據了顯著佔有率。汽車製造商正利用其品牌忠誠度和豐富的車型組合,提供訂閱服務,讓用戶可以無縫存取其車型。這種方式使OEM能夠透過提供靈活的購車方案,並將維護、保險和道路救援服務捆綁到單一套餐中,從而深化客戶關係。透過整合數位平台和個人化服務,OEM正在將自己定位為不斷發展的出行格局中的關鍵參與者,吸引精通科技且注重便利性的消費者。

多品牌需求不斷成長

多品牌細分市場在2024年佔據了相當大的佔有率,這得益於用戶可以透過第三方平台存取來自不同製造商的各種車型。多品牌服務提供從經濟型到豪華型等各種車型的選擇,以滿足不同的客戶偏好。在該領域營運的公司強調方便用戶使用的應用程式、透明的定價和便捷的訂閱流程,以脫穎而出。與經銷商和車隊營運商的策略合作夥伴關係使這些平台能夠維護廣泛且動態的庫存,從而提高客戶保留率和市場覆蓋率。

美國將成為推動力地區

美國汽車訂閱服務市場正經歷強勁成長,預計未來五年規模將超過50億美元,這得益於城鎮化、消費者偏好的轉變以及技術進步。美國消費者越來越青睞靈活、經濟高效的出行解決方案,以減輕購車負擔。該市場的供應商專注於透過無縫的數位介面、量身定做的訂閱計劃以及保險和維護等增值服務來提升客戶體驗。為了鞏固市場地位,各公司正在投資在地化車隊擴張,與汽車製造商和經銷商建立聯盟,並運用資料分析來最佳化車輛可用性和用戶參與度。

汽車訂閱服務市場的主要參與者有大眾、TeslaRents、現代化、FINN、Myles、塔塔汽車、Sixt、梅賽德斯-奔馳、Free2move 和 Carvolution。

汽車訂閱服務市場中的公司正在採取多項關鍵策略來鞏固其市場地位。首先,他們大力投資數位平台,以實現順暢的訂閱管理和個人化的使用者體驗。其次,與原始設備製造商和經銷商的合作有助於確保多樣化的車輛庫存並提升品牌信譽。第三,公司專注於靈活的訂閱計劃,以滿足不同客戶群的需求,包括短期和長期選擇。第四,整合涵蓋保險、維護和道路救援的綜合服務套餐,提升價值並帶來便利。最後,有針對性的行銷和忠誠度計劃有助於在競爭激烈的環境中提高客戶留存率並擴大用戶群。

目錄

第1章:方法論

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- GMI 專有 AI 系統

- 人工智慧驅動的研究增強

- 來源一致性協議

- 人工智慧準確度指標

- 預測模型

- 初步研究和驗證

- 市場估計的主要趨勢

- 量化市場影響分析

- 生長參數對預測的數學影響

- 情境分析框架

- 一些主要來源(但不限於)

- 資料探勘來源

- 次要

- 付費來源

- 公共資源

- 來源(按地區)

- 次要

- 研究軌跡和信心評分

- 研究路線組成部分

- 評分組件

- 研究透明度附錄

- 來源歸因框架

- 品質保證指標

- 我們對信任的承諾

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 從所有權轉向基於存取權的移動性

- 訂閱平台推動電動車普及率上升

- 數位化和基於應用程式的行動生態系統日益完善

- 為個人和商業用戶提供靈活的合約

- 永續性和循環經濟趨勢

- 產業陷阱與挑戰

- 訂閱成本高昂,而非租賃/融資

- 部分地區車型供應有限

- 複雜的保險和責任問題

- 與叫車、租賃和汽車租賃的競爭

- 新興經濟體認知度較低

- 市場機會

- 多品牌和電動車隊的整合

- 與原始設備製造商、經銷商和車隊營運商建立合作夥伴關係

- 中小企業和物流企業擴大採用

- 亞太及拉丁美洲新興市場

- 人工智慧車隊管理和預測性維護

- 成長動力

- 成長潛力分析

- 監管格局

- NHTSA 法規和安全標準

- 資料隱私和連網汽車法規

- 跨境數位貿易合規

- 州和地方監管差異

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 連網汽車訂閱服務

- 物聯網整合和即時監控

- 數據分析和預測性維護

- 提升客戶體驗

- 隱私和資料安全框架

- 自動駕駛汽車訂閱準備情況

- AV 技術整合時間表

- 監理框架發展

- 安全標準和測試要求

- 市場準備與消費者接受度

- 傳統車輛訂閱模式

- 服務交付最佳化

- 營運效率提升

- 客戶服務與支援系統

- 支援遠端資訊處理的訂閱服務

- 車輛追蹤和使用情況監控

- 效能分析與最佳化

- 保險整合與風險管理

- 維護計劃和預測服務

- 連網汽車訂閱服務

- 專利分析

- 生產統計

- 進出口

- 主要進口國家

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

- 用例和應用分析

- 消費者用例

- 城市交通解決方案

- 臨時交通需求

- 車輛試乘及購買決策支持

- 季節性和偶爾使用場景

- 多車家庭最佳化

- 商業用例

- 企業車隊現代化

- 員工流動計劃

- 基於專案的運輸需求

- 地理擴展支持

- 成本管理與預算最佳化

- 政府和公共部門用例

- 艦隊現代化舉措

- 緊急應變和災害管理

- 機構間車輛共享

- 試點專案和技術測試

- 產業特定應用

- 醫療保健和醫療服務

- 房地產和物業管理

- 諮詢和專業服務

- 施工及現場服務

- 最佳案例和成功案例

- 最佳市場條件分析

- 高效能用例範例

- 投資報酬率最大化策略

- 客戶滿意度卓越模型

- 消費者用例

- 定價分析和成本結構

- 定價模型和策略

- 每月訂閱定價等級

- 基於使用情況的定價模型

- 全包定價與模組化定價

- 動態定價和基於需求的調整

- 企業和車隊定價結構

- 成本分解分析

- 車輛購置和折舊成本

- 保險和責任保險費用

- 維護和服務交付成本

- 技術平台和數位基礎設施

- 客戶獲取和行銷費用

- 營運和管理費用

- 區域定價差異

- 北美定價基準

- 歐洲市場定價分析

- 亞太定價策略

- 新興市場定價調整

- 競爭性定價分析

- 高階市場與經濟型市場定價

- 價值主張與價格論證

- 價格彈性和需求敏感度

- 定價策略最佳化

- 定價模型和策略

- 客戶行為與市場採用

- 消費者人口統計與心理統計

- 年齡層分析和代際偏好

- 收入水平和經濟地位的影響

- 地理與城市模式與鄉村模式

- 生活方式與旅遊偏好相關性

- 客戶旅程和決策過程

- 意識和考慮階段

- 評估標準和選擇因素

- 入職和初步體驗

- 使用模式和服務利用率

- 保留和忠誠度發展

- 行為細分分析

- 早期採用者和技術愛好者

- 務實的使用者和價值追求者

- 注重便利的消費者

- 永續發展驅動的客戶

- 客戶滿意度和體驗指標

- 淨推薦值(NPS)分析

- 客戶生命週期價值(CLV)評估

- 流失率和留存率分析

- 服務品質和績效指標

- 採用障礙和阻力因素

- 收養的心理障礙

- 經濟和金融問題

- 服務品質和可靠性問題

- 科技與數位素養挑戰

- 消費者人口統計與心理統計

- 投資分析與市場機會

- 市場成長預測與情境分析

- 投資要求和資本配置

- 投資報酬率分析與獲利能力指標

- 風險評估和緩解策略

- 融資格局與資金來源

- 策略合作機會

- 地域擴張投資重點

- 技術開發與創新投資

- 市場進入策略和時機考慮

- 退出策略和價值實現

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按服務供應商,2021 - 2034 年

- 主要趨勢

- OEM /自營企業

- 第三方/獨立提供者

第6章:市場估計與預測:按訂閱量,2021 - 2034

- 主要趨勢

- 多品牌訂閱

- 單一品牌訂閱

第7章:市場估計與預測:依認購期,2021 - 2034

- 主要趨勢

- 1-6個月

- 6-12個月

- 超過12個月

第8章:市場估計與預測:依車型,2021 - 2034

- 主要趨勢

- 豪華轎車

- 行政車

- 經濟型轎車

- 其他

第9章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 個人的

- 商業的

第10章:市場估計與預測:按燃料,2021 - 2034

- 主要趨勢

- 冰

- 純電動車

- 插電式混合動力

- 油電混合車

第 11 章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 12 章:公司簡介

- 全球參與者

- Audi

- BMW Group

- Cadillac

- Ford Motor Company

- General Motors

- Hyundai Motor

- Jaguar Land Rover

- Lexus

- Mercedes-Benz Group

- Regional Champions

- Autolib

- Cambio CarSharing

- Car2 Go

- DriveNow

- Enterprise CarShare

- Europcar Mobility Group

- Getaround

- GreenMobility

- Hertz Corporation

- Miles Mobility

- Mobility Cooperative

- 新興企業和技術推動者

- Carbar

- Cazoo

- Cluno

- Communauto

- Drover

- Evo Car Share

- Fair

- Flexdrive

- GoGet

- INVERS

The Global Vehicle Subscription Services Market was valued at USD 4.7 billion in 2024 and is estimated to grow at a CAGR of 13.6% to reach USD 16 billion by 2034.

Consumers are shifting away from traditional car ownership toward more flexible and convenient mobility options. This change is fueled by a desire to avoid the long-term financial and maintenance commitments associated with buying or leasing a vehicle. Vehicle subscription services offer users the ability to access different types of vehicles as needed, whether for daily commuting, weekend trips, or special occasions, without the hassles of ownership.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $16 Billion |

| CAGR | 13.6% |

OEM to Gain Traction

The OEM segment in the vehicle subscription services market held a notable share in 2024. Automakers are leveraging their brand loyalty and extensive vehicle portfolios to offer subscription services that provide seamless access to their models. This approach allows OEMs to deepen customer relationships by providing flexible ownership alternatives and bundling maintenance, insurance, and roadside assistance into single packages. By integrating digital platforms and personalized offerings, OEMs are positioning themselves as key players in the evolving mobility landscape, attracting tech-savvy and convenience-oriented consumers.

Rising Demand for Multi-Brand

The multi-brand segment generated a substantial share in 2024, driven by subscribers' access to a wide range of vehicles from various manufacturers, often through third-party platforms. Multi-brand services provide options across vehicle classes, from economy to luxury, catering to diverse customer preferences. Companies operating in this space emphasize user-friendly apps, transparent pricing, and hassle-free subscription processes to differentiate themselves. Strategic partnerships with dealerships and fleet operators enable these platforms to maintain a broad and dynamic inventory, enhancing customer retention and market reach.

U.S. to Emerge as a Propelling Region

The U.S. vehicle subscription services market is experiencing robust growth, projected to surpass USD 5 billion in the next five years, driven by urbanization, evolving consumer preferences, and technological advancements. American consumers are increasingly favoring flexible, cost-effective transportation solutions that eliminate the burdens of ownership. Providers in this market focus on enhancing customer experience through seamless digital interfaces, tailored subscription plans, and value-added services such as insurance and maintenance. To strengthen their market foothold, companies are investing in localized fleet expansions, forging alliances with automakers and dealerships, and employing data analytics to optimize vehicle availability and subscriber engagement.

Major players in the vehicle subscription services market are Volkswagen, TeslaRents, Hyundai, FINN, Myles, Tata Motors, Sixt, Mercedes-Benz, Free2move, and Carvolution.

Companies in the vehicle subscription services market are adopting several key strategies to solidify their market position. First, they are investing heavily in digital platforms that enable smooth subscription management and personalized user experiences. Second, partnerships with OEMs and dealerships help secure diverse vehicle inventories and enhance brand credibility. Third, companies focus on flexible subscription plans that cater to different customer segments, including short-term and long-term options. Fourth, integrating comprehensive service packages covering insurance, maintenance, and roadside assistance adds value and convenience. Lastly, targeted marketing and loyalty programs help increase customer retention and expand their subscriber base in a competitive landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.1.6 GMI proprietary AI system

- 1.1.6.1 AI-Powered research enhancement

- 1.1.6.2 Source consistency protocol

- 1.1.6.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research trail & confidence scoring

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service provider

- 2.2.3 Subscription

- 2.2.4 Subscription period

- 2.2.5 Vehicle

- 2.2.6 Fuel

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift from ownership to access-based mobility

- 3.2.1.2 Rising EV adoption supported by subscription platforms

- 3.2.1.3 Increasing digitalization & app-based mobility ecosystems

- 3.2.1.4 Flexible contracts for personal & commercial users

- 3.2.1.5 Sustainability and circular economy trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High subscription costs vs. leasing/financing

- 3.2.2.2 Limited availability of vehicle models in some regions

- 3.2.2.3 Complex insurance & liability issues

- 3.2.2.4 Competition with ride-hailing, leasing, and car rental

- 3.2.2.5 Low awareness in emerging economies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of multi-brand and EV fleets

- 3.2.3.2 Partnerships with OEMs, dealers, and fleet operators

- 3.2.3.3 Growing adoption by SMEs and logistics players

- 3.2.3.4 Emerging markets in APAC & LATAM

- 3.2.3.5 AI-enabled fleet management & predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 NHTSA regulations & safety standards

- 3.4.2 Data privacy & connected vehicle regulations

- 3.4.3 Cross-border digital trade compliance

- 3.4.4 State & local regulatory variations

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Connected vehicle subscription services

- 3.7.1.1 IoT integration & real-time monitoring

- 3.7.1.2 Data analytics & predictive maintenance

- 3.7.1.3 Customer experience enhancement

- 3.7.1.4 Privacy & data security frameworks

- 3.7.2 Autonomous vehicle subscription readiness

- 3.7.2.1 AV technology integration timeline

- 3.7.2.2 Regulatory framework development

- 3.7.2.3 Safety standards & testing requirements

- 3.7.2.4 Market readiness & consumer acceptance

- 3.7.3 Traditional vehicle subscription models

- 3.7.3.1 Service delivery optimization

- 3.7.3.2 Operational efficiency improvements

- 3.7.3.3 Customer service & support systems

- 3.7.4 Telematics-enabled subscription services

- 3.7.4.1 Vehicle tracking & usage monitoring

- 3.7.4.2 Performance analytics & optimization

- 3.7.4.3 Insurance integration & risk management

- 3.7.4.4 Maintenance scheduling & predictive services

- 3.7.1 Connected vehicle subscription services

- 3.8 Patent analysis

- 3.9 Production statistics

- 3.9.1 Import and export

- 3.9.2 Major import countries

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use Cases & Application Analysis

- 3.11.1 Consumer use cases

- 3.11.1.1 Urban mobility solutions

- 3.11.1.2 Temporary transportation needs

- 3.11.1.3 Vehicle trial & purchase decision support

- 3.11.1.4 Seasonal & occasional use scenarios

- 3.11.1.5 Multi-vehicle household optimization

- 3.11.2 Business use cases

- 3.11.2.1 Corporate fleet modernization

- 3.11.2.2 Employee mobility programs

- 3.11.2.3 Project-based transportation needs

- 3.11.2.4 Geographic expansion support

- 3.11.2.5 Cost management & budget optimization

- 3.11.3 Government & public sector use cases

- 3.11.3.1 Fleet modernization initiatives

- 3.11.3.2 Emergency response & disaster management

- 3.11.3.3 Inter-agency vehicle sharing

- 3.11.3.4 Pilot programs & technology testing

- 3.11.4 Industry-specific applications

- 3.11.4.1 Healthcare & medical services

- 3.11.4.2 Real estate & property management

- 3.11.4.3 Consulting & professional services

- 3.11.4.4 Construction & field services

- 3.11.5 Best case scenarios & success stories

- 3.11.5.1 Optimal market conditions analysis

- 3.11.5.2 High-performance use case examples

- 3.11.5.3 ROI maximization strategies

- 3.11.5.4 Customer satisfaction excellence models

- 3.11.1 Consumer use cases

- 3.12 Pricing analysis & cost structure

- 3.12.1 Pricing models & strategies

- 3.12.1.1 Monthly subscription pricing tiers

- 3.12.1.2 Usage-based pricing models

- 3.12.1.3 All-inclusive vs. Modular pricing

- 3.12.1.4 Dynamic pricing & demand-based adjustments

- 3.12.1.5 Corporate & fleet pricing structures

- 3.12.2 Cost breakdown analysis

- 3.12.2.1 Vehicle acquisition & depreciation costs

- 3.12.2.2 Insurance & liability coverage expenses

- 3.12.2.3 Maintenance & service delivery costs

- 3.12.2.4 Technology platform & digital infrastructure

- 3.12.2.5 Customer acquisition & marketing expenses

- 3.12.2.6 Operational & administrative overheads

- 3.12.3 Regional pricing variations

- 3.12.3.1 North American pricing benchmarks

- 3.12.3.2 European market pricing analysis

- 3.12.3.3 Asia Pacific pricing strategies

- 3.12.3.4 Emerging market pricing adaptations

- 3.12.4 Competitive pricing analysis

- 3.12.4.1 Premium vs. Economy segment pricing

- 3.12.4.2 Value proposition & price justification

- 3.12.4.3 Price elasticity & demand sensitivity

- 3.12.4.4 Pricing strategy optimization

- 3.12.1 Pricing models & strategies

- 3.13 Customer behavior & market adoption

- 3.13.1 Consumer demographics & psychographics

- 3.13.1.1 Age group analysis & generational preferences

- 3.13.1.2 Income level & economic status impact

- 3.13.1.3 Geographic & urban vs. Rural patterns

- 3.13.1.4 Lifestyle & mobility preference correlation

- 3.13.2 Customer journey & decision-making process

- 3.13.2.1 Awareness & consideration stages

- 3.13.2.2 Evaluation criteria & selection factors

- 3.13.2.3 Onboarding & initial experience

- 3.13.2.4 Usage patterns & service utilization

- 3.13.2.5 Retention & loyalty development

- 3.13.3 Behavioral segmentation analysis

- 3.13.3.1 Early adopters & technology enthusiasts

- 3.13.3.2 Pragmatic users & value seekers

- 3.13.3.3 Convenience-focused consumers

- 3.13.3.4 Sustainability-driven customers

- 3.13.4 Customer satisfaction & experience metrics

- 3.13.4.1 Net promoter score (NPS) analysis

- 3.13.4.2 Customer lifetime value (CLV) assessment

- 3.13.4.3 Churn rate & retention analysis

- 3.13.4.4 Service quality & performance indicators

- 3.13.5 Adoption barriers & resistance factors

- 3.13.5.1 Psychological barriers to adoption

- 3.13.5.2 Economic & financial concerns

- 3.13.5.3 Service quality & reliability issues

- 3.13.5.4 Technology & digital literacy challenges

- 3.13.1 Consumer demographics & psychographics

- 3.14 Investment analysis & market opportunities

- 3.14.1 Market growth projections & scenario analysis

- 3.14.2 Investment requirements & capital allocation

- 3.14.3 ROI analysis & profitability metrics

- 3.14.4 Risk assessment & mitigation strategies

- 3.14.5 Funding landscape & capital sources

- 3.14.6 Strategic partnership opportunities

- 3.14.7 Geographic expansion investment priorities

- 3.14.8 Technology development & innovation investments

- 3.14.9 Market entry strategies & timing considerations

- 3.14.10 Exit strategies & value realization

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service Provider, 2021 - 2034 ($Bn, Fleet Size)

- 5.1 Key trends

- 5.2 OEM / Captives

- 5.3 Third-Party / Independent Providers

Chapter 6 Market Estimates & Forecast, By Subscription, 2021 - 2034 ($Bn, Fleet Size)

- 6.1 Key trends

- 6.2 Multi-brand subscriptions

- 6.3 Single-brand subscriptions

Chapter 7 Market Estimates & Forecast, By Subscription Period, 2021 - 2034 ($Bn, Fleet Size)

- 7.1 Key trends

- 7.2 1-6 months

- 7.3 6-12 months

- 7.4 More than 12 months

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Fleet Size)

- 8.1 Key trends

- 8.2 Luxury car

- 8.3 Executive car

- 8.4 Economy car

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Fleet Size)

- 9.1 Key trends

- 9.2 Personal

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Fuel , 2021 - 2034 ($Bn, Fleet Size)

- 10.1 Key trends

- 10.2 ICE

- 10.3 BEV

- 10.4 PHEV

- 10.5 HEV

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Fleet Size)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Audi

- 12.1.2 BMW Group

- 12.1.3 Cadillac

- 12.1.4 Ford Motor Company

- 12.1.5 General Motors

- 12.1.6 Hyundai Motor

- 12.1.7 Jaguar Land Rover

- 12.1.8 Lexus

- 12.1.9 Mercedes-Benz Group

- 12.2 Regional Champions

- 12.2.1 Autolib

- 12.2.2 Cambio CarSharing

- 12.2.3. Car2 Go

- 12.2.4 DriveNow

- 12.2.5 Enterprise CarShare

- 12.2.6 Europcar Mobility Group

- 12.2.7 Getaround

- 12.2.8 GreenMobility

- 12.2.9 Hertz Corporation

- 12.2.10 Miles Mobility

- 12.2.11 Mobility Cooperative

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 Carbar

- 12.3.2 Cazoo

- 12.3.3 Cluno

- 12.3.4 Communauto

- 12.3.5 Drover

- 12.3.6 Evo Car Share

- 12.3.7 Fair

- 12.3.8 Flexdrive

- 12.3.9 GoGet

- 12.3.10 INVERS