|

市場調查報告書

商品編碼

1822621

區域供熱市場機會、成長動力、產業趨勢分析及2025-2034年預測District Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

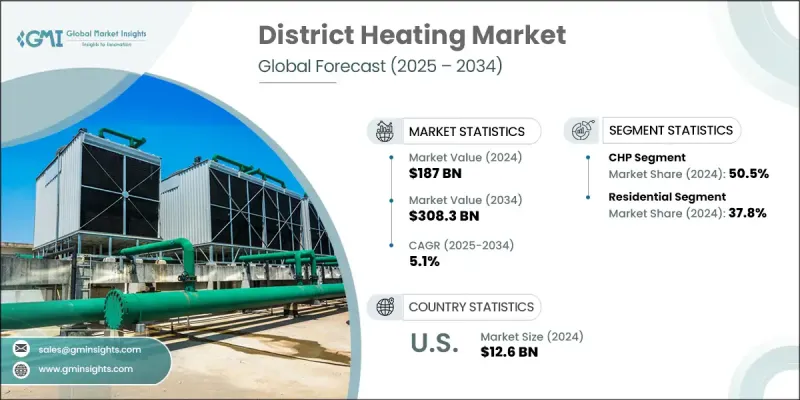

2024年,全球區域供熱市場規模達1,870億美元,預計到2034年將以5.1%的複合年成長率成長,達到3,083億美元。這一成長將透過提供穩定的能源供應來增強能源安全。與依賴易揮發化石燃料的獨立供熱系統不同,區域供熱管網不易受價格波動和供應中斷的影響。這些系統採用集中式供熱和分配方式,確保住宅、商業和工業用戶獲得穩定的能源供應。這種韌性有助於促進經濟穩定,並透過減少對化石燃料的依賴和降低碳排放來支持永續發展目標。為此,2024年6月,惠普企業和丹佛斯攜手合作,致力於降低資料中心的能耗。雙方的模組化設計整合了熱量捕獲系統,以加速邊緣人工智慧和運算任務的運行,同時將多餘的熱量回收利用。此舉與全球為降低能源相關風險和建立更具韌性的未來能源基礎設施所做的努力一致。

整個區域供熱市場根據應用、來源和地區進行分類。地熱能市場預計將在2032年之前錄得可觀的複合年成長率,這得益於其作為永續可靠熱源的日益普及。地熱能提供穩定且可再生的熱能供應,減少了對化石燃料的依賴,並最大限度地減少了溫室氣體排放。此外,技術進步使地熱開採更有效率且經濟實惠,從而鼓勵將其整合到區域供熱系統中。各國政府和環保政策也支持地熱能應用於區域供熱,將進一步促進該領域的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1870億美元 |

| 預測值 | 3083億美元 |

| 複合年成長率 | 5.1% |

到2032年,住宅供暖市場將佔據顯著的區域供熱市場佔有率,這得益於城鎮化進程的加快以及人口稠密地區對高效、永續供暖解決方案的需求。屋主們正在尋求環保的選擇,以降低能源成本和碳足跡。區域供熱系統提供可靠且方便的加熱方式,無需單獨安裝鍋爐和維護。此外,政府推出的獎勵措施和法規促進了節能建築的發展,也促使新建住宅項目採用區域供熱。由於致力於減少碳排放和實現氣候目標,歐洲區域供熱市場在預測期內將呈現顯著的複合年成長率。歐洲各國正在大力投資再生能源和先進的暖氣基礎設施。城鎮化和老化供暖系統的現代化改造,催生了對更有效率、集中式解決方案的需求。此外,歐盟的政策和資金支持永續區域供熱網路的發展,鼓勵公共和私營部門採用這些系統,以提高能源效率並減少對環境的影響。這些因素將促進區域供熱產業的成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 主要供應商和技術提供商

- 物流、配送和服務

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 區域供熱成本結構分析

- 價格趨勢分析

- 按地區

- 按來源

- 未來市場展望及新興機遇

- 未來區域供熱和製冷解決方案的開發

- 靛青

- 軟性網路

- E2區

- 交易

- 案例研究分析—斯德哥爾摩綜合DHC系統

- 項目概述

- 關鍵事實和數據

- 客戶區隔

- 支持 DHC 的政策和激勵措施

- 區域供熱系統的技術與運作參數

- 客戶和最終用途分析

- 住宅、工業和商業部門的採用

- 都市與農村滲透率

- 需求趨勢與消費模式

第4章:競爭格局

- 介紹

- 2024年各地區公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 戰略儀表板

- 策略舉措

- 重大併購活動

- 關鍵夥伴關係和合作

- 產品創新與發布

- 市場擴張策略

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依來源,2021 - 2034

- 主要趨勢

- 熱電聯產

- 地熱

- 太陽的

- 僅供熱鍋爐

- 其他

第6章:市場規模與預測:按應用,2021 - 2034

- 主要趨勢

- 住宅

- 商業的

- 學院/大學

- 辦公室

- 政府/軍隊

- 其他

- 工業的

- 化學

- 煉油廠

- 紙

- 其他

第7章:市場規模及預測:依地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 波蘭

- 俄羅斯

- 瑞典

- 芬蘭

- 義大利

- 丹麥

- 英國

- 斯洛伐克

- 奧地利

- 捷克共和國

- 法國

- 亞太地區

- 中國

- 日本

- 韓國

第8章:公司簡介

- A2A SpA

- Alfa Laval

- Antin Infrastructure Partners

- BEW Berlin Energy and Heat

- CenTrio

- Cordia

- Danfoss

- E.ON

- EDF

- EnBW Energie Baden-Wurttemberg

- ENGIE

- Fortum

- Goteborg Energi

- Hafslund

- Iren SpA

- Kelag Energie & Warme

- Keppel

- Korea District Heating

- LOGSTOR Denmark Holding

- Nevel

- Ørsted

- Ramboll

- RWE

- Shinryo Corporation

- Statkraft

- STEAG

- Vattenfall

- Veolia

The Global District Heating Market was valued at USD 187 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 308.3 billion by 2034, ushered by enhancing energy security by providing a stable energy supply. Unlike individual heating systems reliant on volatile fossil fuels, district heating networks are less susceptible to price fluctuations and supply disruptions. By utilizing a centralized approach to heat production and distribution, these systems ensure consistent energy availability for residential, commercial, and industrial users. This resilience promotes economic stability and supports sustainability goals by reducing reliance on fossil fuels and lowering carbon emissions. To that end, in June 2024, Hewlett Packard Enterprise and Danfoss joined forces to reduce data center energy usage. Their modular design integrates heat capture systems to accelerate AI and compute tasks at the edge, while excess heat is reused externally. It aligns with global efforts to mitigate energy-related risks and build more resilient energy infrastructures for the future.

The overall district heating market is categorized based on application, source, and region. The geothermal segment will record a promising CAGR through 2032, due to its increasing recognition as a sustainable and reliable heat source. Geothermal energy provides a consistent and renewable supply of heat, reducing dependency on fossil fuels and minimizing GHG emissions. Additionally, technological advancements have made geothermal extraction more efficient and cost-effective, encouraging its integration into district heating systems. Governments and environmental policies also support geothermal adoption for district heating applications, adding to segment growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $187 Billion |

| Forecast Value | $308.3 Billion |

| CAGR | 5.1% |

The residential segment will acquire a remarkable district heating market share by 2032, owing to growing urbanization and the need for efficient, sustainable heating solutions in densely populated areas. Homeowners are seeking eco-friendly options to reduce energy costs and carbon footprints. District heating systems provide a reliable and convenient heating source, eliminating the need for individual boilers and maintenance. Additionally, government incentives and regulations promoting energy-efficient buildings are ushering in the adoption of district heating in new residential developments. Europe district heating market will infer a notable CAGR during the forecast period, because of the commitment to reducing carbon emissions and achieving climate goals. European countries are investing heavily in renewable energy sources and advanced heating infrastructure. Urbanization and the modernization of aging heating systems catapult the need for more efficient, centralized solutions. Additionally, European Union policies and funding support the development of sustainable district heating networks, encouraging public and private sectors to adopt these systems for improved energy efficiency and environmental impact reduction. These factors will bolster the regional industry growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid sources

- 1.5.1.2 Public sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Source trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key suppliers and technology providers

- 3.1.2 Logistics, distribution, and services

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of district heating

- 3.8 Price trend analysis

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market outlook & emerging opportunities

- 3.10 Development of future district heating & cooling solutions

- 3.10.1 INDIGO

- 3.10.2 FLEXYNETS

- 3.10.3 E2District

- 3.10.4 InDeal

- 3.11 Case study analysis - Integrated DHC system in Stockholm

- 3.11.1 Project overview

- 3.11.2 Key facts & figures

- 3.11.3 Customer segmentation

- 3.11.4 Policies & incentives supporting the DHC

- 3.12 Technical and operational parameters of district heating systems

- 3.13 Customer & End Use analysis

- 3.13.1 Adoption by residential, industrial, and commercial sectors

- 3.13.2 Urban vs rural penetration

- 3.13.3 Demand trends and consumption patterns

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Major M&A activities

- 4.4.2 Key partnerships and collaborations

- 4.4.3 Product innovations and launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Source, 2021 - 2034 (USD Billion & PJ)

- 5.1 Key trends

- 5.2 CHP

- 5.3 Geothermal

- 5.4 Solar

- 5.5 Heat only boiler

- 5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion & PJ)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 College/university

- 6.3.2 Office

- 6.3.3 Government/military

- 6.3.4 Others

- 6.4 Industrial

- 6.4.1 Chemical

- 6.4.2 Refinery

- 6.4.3 Paper

- 6.4.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & PJ)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Poland

- 7.3.3 Russia

- 7.3.4 Sweden

- 7.3.5 Finland

- 7.3.6 Italy

- 7.3.7 Denmark

- 7.3.8 UK

- 7.3.9 Slovakia

- 7.3.10 Austria

- 7.3.11 Czech Republic

- 7.3.12 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

Chapter 8 Company Profiles

- 8.1 A2A S.p.A.

- 8.2 Alfa Laval

- 8.3 Antin Infrastructure Partners

- 8.4 BEW Berlin Energy and Heat

- 8.5 CenTrio

- 8.6 Cordia

- 8.7 Danfoss

- 8.8 E.ON

- 8.9 EDF

- 8.10 EnBW Energie Baden-Wurttemberg

- 8.11 ENGIE

- 8.12 Fortum

- 8.13 Goteborg Energi

- 8.14 Hafslund

- 8.15 Iren S.p.A.

- 8.16 Kelag Energie & Warme

- 8.17 Keppel

- 8.18 Korea District Heating

- 8.19 LOGSTOR Denmark Holding

- 8.20 Nevel

- 8.21 Ørsted

- 8.22 Ramboll

- 8.23 RWE

- 8.24 Shinryo Corporation

- 8.25 Statkraft

- 8.26 STEAG

- 8.27 Vattenfall

- 8.28 Veolia

區域供熱市場:網路類型、電站容量、能源來源、供熱溫度、應用、最終用途-2026-2032年全球市場預測

區域供熱市場:網路類型、電站容量、能源來源、供熱溫度、應用、最終用途-2026-2032年全球市場預測 英國區域供熱:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

英國區域供熱:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球區域供熱市場規模、佔有率、趨勢和成長分析報告(2026-2034年)住宅區域供熱市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測商業區域供熱市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

全球區域供熱市場規模、佔有率、趨勢和成長分析報告(2026-2034年)住宅區域供熱市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測商業區域供熱市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 2026年全球區域供熱市場報告

2026年全球區域供熱市場報告 區域供熱市場規模、佔有率和趨勢分析報告:按熱源、類型、應用、工廠類型、地區和細分市場預測(2026-2033 年)

區域供熱市場規模、佔有率和趨勢分析報告:按熱源、類型、應用、工廠類型、地區和細分市場預測(2026-2033 年) 全球熱力網路市場

全球熱力網路市場 區域供熱的全球市場:廠房類型·熱源·用途·各地區 (~2032年)

區域供熱的全球市場:廠房類型·熱源·用途·各地區 (~2032年) 按工廠類型、熱源、應用和地區分類的區域供熱市場

按工廠類型、熱源、應用和地區分類的區域供熱市場