|

市場調查報告書

商品編碼

1822593

衛星 NTN 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Satellite NTN Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

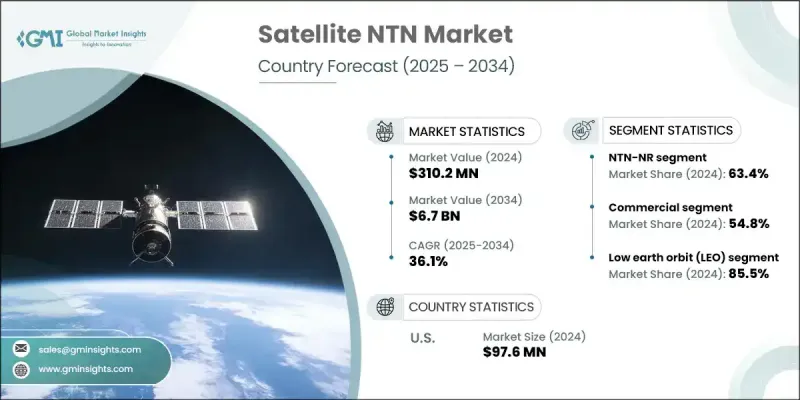

2024 年全球衛星 NTN 市值為 3.102 億美元,預計到 2034 年將以 36.1% 的複合年成長率成長至 67 億美元。

這一顯著成長主要得益於全球對高速寬頻連線日益成長的需求,尤其是在服務不足的地區。持續部署的包含NTN基礎設施的5G網路在市場擴張中發揮關鍵作用。 NTN與3GPP Release 17及更高版本的整合,在地面和衛星網路之間建立了更無縫的連接,改善了農村和偏遠地區的覆蓋範圍。對低地球軌道(LEO)衛星系統的投資正在激增,各大公司大幅擴充其衛星群,以填補全球連結缺口。隨著電信業者尋求更具彈性和可擴展性的基礎設施,基於衛星的NTN解決方案正在部署以加強地面系統,特別是在網路基礎設施稀疏的地區。在各國透過衛星服務和支持地面設施縮小數位落差的努力的支持下,巴西、南非和印度等新興經濟體正在迅速採用這些技術。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.102億美元 |

| 預測值 | 67億美元 |

| 複合年成長率 | 36.1% |

NTN-NR 技術由於相容 5G 標準,在 2024 年佔據了 63.4% 的市場佔有率,為行動和物聯網應用提供了高資料吞吐量和超低延遲。政府對 5G NTN 部署的支援不斷增加,電信業者也加強了投資力度,進一步加速了這一領域的發展動能。 NTN-NR 系統的整合正在帶來更流暢的用戶體驗,並推動動物聯網、物流和行動領域的創新。

受寬頻存取、數位內容交付和企業物聯網解決方案需求不斷成長的推動,商業應用領域在2024年佔據了54.8%的佔有率。隨著數位轉型成為企業的策略重點,各企業紛紛投資衛星NTN,以提高網路的連續性、速度和可擴展性。從媒體到物流,再到雲端服務,商業用戶紛紛轉向這些解決方案,以獲得跨地域的可靠覆蓋。

2024年,北美衛星NTN市場佔據35.1%的市場佔有率,這得益於5G NTN的早期採用、成熟的衛星基礎設施以及對低地球軌道(LEO)系統的大量投資。核心技術公司的聚集、強大的用戶群,以及強力的監管和資金支持,將繼續推動北美地區保持領先地位。有意在該地區擴張規模的企業應專注於與當地電信業者和公共部門機構合作,將衛星覆蓋範圍擴展到服務不足的農村地區,特別是利用低延遲解決方案和寬頻補貼。

影響全球衛星 NTN 市場的關鍵公司包括洛克希德馬丁、OneWeb、L3Harris Technologies、Teledyne Technologies、Viasat Inc.、愛立信、SES SA、太空探索技術公司 (SpaceX)、SWISSto12 和 Telesat。為了保持在衛星 NTN 產業的競爭優勢,各公司正在與電信營運商和政府建立戰略合作關係,以擴大 5G NTN 覆蓋範圍。領先的參與者正在擴展其 LEO 衛星星座,以向偏遠和城市市場提供低延遲、高吞吐量的服務。他們還投資於下一代地面基礎設施、邊緣整合和自適應波形技術,以滿足不斷變化的資料需求。對研發、可擴展平台解決方案和基於雲端的連接服務的重視正在幫助品牌滿足企業需求和新興的物聯網用例。戰略性的政府合作夥伴關係支持在服務欠缺地區部署基礎設施。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 全球對寬頻連線的需求不斷成長

- 擴展採用NTN技術的5G網路

- 低地球軌道(LEO)衛星星座的投資不斷增加

- 物聯網和機器對機器 (M2M) 應用的採用率不斷上升

- 政府措施支持國防和公共安全衛星通訊

- 產業陷阱與挑戰

- 高資本支出和營運成本

- 監管挑戰和複雜的頻譜分配

- 市場機會

- 融合地面和非地面通訊的混合網路發展

- 不斷成長的數位基礎設施需求

- 機載處理和天線系統的技術進步

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規要求

- 專利和智慧財產權分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021 - 2034

- 主要趨勢

- NTN天然橡膠

- NTN-物聯網

第6章:市場估計與預測:按組件,2021 - 2034

- 主要趨勢

- 硬體

- 射頻前端

- 天線

- 板載處理器單元

- 其他

- 軟體

第7章:市場估計與預測:按軌道類型,2021 - 2034 年

- 主要趨勢

- 低地球軌道(LEO)

- 中地球軌道(MEO)

- 地球靜止軌道(GEO)

第8章:市場估計與預測:按頻率,2021 - 2034 年

- 主要趨勢

- L波段

- S波段

- C波段

- Ku波段

- Ka波段

- HF/VHF/UHF頻段

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 寬頻網路存取

- 直接到裝置 (D2D) 連接

- 回程和網路擴展

- 物聯網/M2M 連接

- 其他

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 商業的

- 電信及網際網路服務

- 媒體與廣播

- 企業和消費者物聯網

- 能源和公用事業

- 運輸與物流

- 其他

- 防禦

- C4 ISR

- 軍事通訊

- 戰場機動性和戰術網路

- 監視和偵察衛星

- 其他

- 政府

- 公共安全與緊急應變

- 太空研究與探索

- 環境監測

- 基礎設施管理

- 其他

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 全球關鍵參與者

- Space Exploration Technologies Corp. (SpaceX)

- OneWeb

- SES SA

- Viasat Inc.

- Telesat

- 區域關鍵參與者

- 北美洲

- Intelsat General Communications

- Lockheed Martin

- L3Harris Technologies

- Qorvo, Inc.

- Qualcomm Technologies Inc.

- 歐洲

- Airbus

- Thales Alenia Space

- SWISSto12

- OQ Technology

- 亞太地區

- Huawei Technologies Co., Ltd.

- MediaTek Inc.

- NEC Corporation

- Nokia Corporation

- 北美洲

- 利基市場參與者/顛覆者

- AST SpaceMobile

- Teledyne Technologies

- Ericsson

- Filtronic Plc

- ZTE Corporation

The Global Satellite NTN Market was valued at USD 310.2 million in 2024 and is estimated to grow at a CAGR of 36.1% to reach USD 6.7 billion by 2034.

This remarkable growth is largely driven by the rising global demand for high-speed broadband connectivity, especially in underserved regions. The continued rollout of 5G networks incorporating NTN infrastructure is playing a key role in market expansion. Integration of NTN into 3GPP's Release 17 and beyond has created a more seamless link between terrestrial and satellite networks, improving coverage in rural and hard-to-reach areas. Investment in low Earth orbit (LEO) satellite systems is surging, with companies significantly expanding their satellite fleets to fill connectivity gaps worldwide. As telecom providers look for more resilient and scalable infrastructure, satellite-based NTN solutions are being deployed to strengthen terrestrial systems-particularly in regions where network infrastructure is sparse. Emerging economies like Brazil, South Africa, and India are rapidly adopting these technologies, backed by national efforts to close the digital divide through satellite services and supporting ground installations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $310.2 Million |

| Forecast Value | $6.7 Billion |

| CAGR | 36.1% |

The NTN-NR technology held a 63.4% share in 2024 due to its compatibility with 5G standards, offering high data throughput and ultra-low latency for mobile and IoT applications. Increasing government support and telecom operator investment in 5G NTN rollouts are further accelerating the momentum of this segment. The integration of NTN-NR systems is enabling smoother user experiences and driving innovation across IoT, logistics, and mobile sectors.

The commercial application segment held 54.8% share in 2024, propelled by growing demand for broadband access, digital content delivery, and enterprise IoT solutions. As digital transformation becomes a strategic priority for businesses, organizations are investing in satellite NTN to improve network continuity, speed, and scalability. From media to logistics and cloud-based services, commercial users are turning to these solutions for dependable coverage across diverse geographies.

North America Satellite NTN Market held a 35.1% share in 2024, supported by early 5G NTN adoption, an established satellite infrastructure, and substantial investments in LEO systems. The presence of key technology companies and a robust user base, along with strong regulatory and funding support, continues to drive regional leadership. Businesses aiming to scale in this region should focus on partnerships with local telecom carriers and public-sector agencies to extend satellite coverage to underserved rural zones, particularly by leveraging low-latency solutions and broadband grants.

Key companies shaping the Global Satellite NTN Market include Lockheed Martin, OneWeb, L3Harris Technologies, Teledyne Technologies, Viasat Inc., Ericsson, SES S.A., Space Exploration Technologies Corp. (SpaceX), SWISSto12, and Telesat. To maintain a competitive edge in the satellite NTN industry, companies are pursuing strategic collaborations with telecom carriers and governments to scale 5G NTN coverage. Leading players are expanding their LEO satellite constellations to deliver low-latency, high-throughput services across remote and urban markets. They are also investing in next-gen ground infrastructure, edge integration, and adaptive waveform technology to meet evolving data needs. Emphasis on R&D, scalable platform solutions, and cloud-based connectivity services is helping brands cater to enterprise demand and emerging IoT use cases. The strategic government partnerships support infrastructure deployment in underserved areas.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Component trends

- 2.2.3 Orbit type trends

- 2.2.4 Frequency trends

- 2.2.5 Application trends

- 2.2.6 end use trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global demand for broadband connectivity

- 3.2.1.2 Expansion of 5G networks incorporating NTN technology

- 3.2.1.3 Growing investments in Low Earth Orbit (LEO) satellite constellations

- 3.2.1.4 Rising adoption of IoT and Machine-to-Machine (M2M) applications

- 3.2.1.5 Government initiatives supporting satellite communications for defense and public safety

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure and operational costs

- 3.2.2.2 Regulatory challenges and complex spectrum allocation

- 3.2.3 Market opportunities

- 3.2.3.1 Development of hybrid networks integrating terrestrial and non-terrestrial communication

- 3.2.3.2 Growing digital infrastructure needs

- 3.2.3.3 Technological advancements in onboard processing and antenna systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 NTN-NR

- 5.3 NTN-IoT

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 RF front end

- 6.2.2 Antenna

- 6.2.3 Onboard processor unit

- 6.2.4 Others

- 6.3 Software

Chapter 7 Market Estimates and Forecast, By Orbit Type, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Low earth orbit (LEO)

- 7.3 Medium earth orbit (MEO)

- 7.4 Geostationary orbit (GEO)

Chapter 8 Market Estimates and Forecast, By Frequency, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 L-band

- 8.3 S-band

- 8.4 C-band

- 8.5 Ku-band

- 8.6 Ka-band

- 8.7 HF/VHF/UHF-bands

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 Broadband internet access

- 9.3 Direct-to-Device (D2D) connectivity

- 9.4 Backhaul and network extension

- 9.5 IoT/M2M connectivity

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 10.1 Commercial

- 10.1.1 Telecommunications & internet service

- 10.1.2 Media & broadcasting

- 10.1.3 Enterprise & consumer IoT

- 10.1.4 Energy & utilities

- 10.1.5 Transportation & logistics

- 10.1.6 Others

- 10.2 Defense

- 10.2.1. C4 ISR

- 10.2.2 Military communications

- 10.2.3 Battlefield mobility & tactical networks

- 10.2.4 Surveillance & reconnaissance satellites

- 10.2.5 Others

- 10.3 Government

- 10.3.1 Public safety & emergency response

- 10.3.2 Space research & exploration

- 10.3.3 Environmental monitoring

- 10.3.4 Infrastructure management

- 10.3.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Space Exploration Technologies Corp. (SpaceX)

- 12.1.2 OneWeb

- 12.1.3 SES S.A.

- 12.1.4 Viasat Inc.

- 12.1.5 Telesat

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Intelsat General Communications

- 12.2.1.2 Lockheed Martin

- 12.2.1.3 L3Harris Technologies

- 12.2.1.4 Qorvo, Inc.

- 12.2.1.5 Qualcomm Technologies Inc.

- 12.2.2 Europe

- 12.2.2.1 Airbus

- 12.2.2.2 Thales Alenia Space

- 12.2.2.3 SWISSto12

- 12.2.2.4 OQ Technology

- 12.2.3 Asia Pacific

- 12.2.3.1 Huawei Technologies Co., Ltd.

- 12.2.3.2 MediaTek Inc.

- 12.2.3.3 NEC Corporation

- 12.2.3.4 Nokia Corporation

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 AST SpaceMobile

- 12.3.2 Teledyne Technologies

- 12.3.3 Ericsson

- 12.3.4 Filtronic Plc

- 12.3.5 ZTE Corporation

全球NTN衛星市場(至2040年):產業趨勢與預測

全球NTN衛星市場(至2040年):產業趨勢與預測 2026年全球衛星服務市場報告2026年全球通訊衛星營運服務市場報告

2026年全球衛星服務市場報告2026年全球通訊衛星營運服務市場報告 衛星營運商財務關鍵績效指標:2025 年面向消費者的衛星直接分散式服務:趨勢與預測(2024-2034)

衛星營運商財務關鍵績效指標:2025 年面向消費者的衛星直接分散式服務:趨勢與預測(2024-2034) NTN智慧型手機市場:按作業系統、分銷管道、網路世代、最終用戶和螢幕大小的全球預測,2026-2032年智慧型手機衛星直連裝置 (D2D) 服務:案例研究與分析

NTN智慧型手機市場:按作業系統、分銷管道、網路世代、最終用戶和螢幕大小的全球預測,2026-2032年智慧型手機衛星直連裝置 (D2D) 服務:案例研究與分析 消費者對衛星直連裝置的付費意願:消費者調查(2025 年)

消費者對衛星直連裝置的付費意願:消費者調查(2025 年) 消費者對衛星D2D服務的興趣:消費者調查

消費者對衛星D2D服務的興趣:消費者調查 全球直接到設備 (D2D) 市場(按服務類型、客戶類型、延遲等級、頻率、軌道和地區分類)- 預測至 2030 年

全球直接到設備 (D2D) 市場(按服務類型、客戶類型、延遲等級、頻率、軌道和地區分類)- 預測至 2030 年