|

市場調查報告書

商品編碼

1822562

古董及收藏品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Antiques and Collectibles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

根據 Global Market Insights, Inc. 發布的最新報告,古董和收藏品市場在 2024 年的價值為 2,381 億美元,預計將從 2025 年的 2,492 億美元成長到 2034 年的 4029 億美元,複合年成長率為 5.5%。

懷舊和復古產品的復甦、數位拍賣網站的擴張,以及人們對非傳統投資(例如藝術品、稀有玩具、紀念品和古代文物)日益成長的興趣,共同推動了市場的成長。成熟收藏家和新一代收藏家都在線上線下推動市場需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2381億美元 |

| 預測值 | 4029億美元 |

| 複合年成長率 | 5.5% |

關鍵促進因素:

1.另類投資日益普及:在市場不穩定時期,收藏品、藝術品和古董產品越來越被視為一種價值儲存手段。

2.拍賣數位化:行動應用程式和網路平台擴大了全球收藏品的取得管道。

3.名人和流行文化的吸引力日益增強:與標誌性人物、電影和品牌相關的收藏品仍然吸引著大批買家。

4.千禧世代和 Z 世代參與度上升:年輕一代正在收藏諸如 Pokemon 卡、黑膠唱片和 90 年代紀念品等收藏品。

關鍵參與者:

- 2024年古董和收藏品領域的主要參與者包括佳士得、蘇富比、Heritage Auctions、eBay、邦瀚斯和Hakes Auctions。這六家公司合計佔據約11%的市場。

主要挑戰:

- 真實性和出處問題:假冒風險仍然是主要的威懾因素(尤其是對於高階和數位收藏品)。

- 價格不確定性:價值可能會根據趨勢或經濟變化而波動,這可能會阻礙消費者(尤其是那些規避風險的消費者)的購買。

1. 按產品類別 - 美術和繪畫佔據最大市場佔有率

2024年,純藝術和繪畫佔據了市場的最大佔有率,知名藝術家創作的傳統和當代藝術(包括原創作品)的拍賣價格均有所上漲。知名藝術家的原創作品吸引了「高淨值」收藏家和機構買家的青睞。

2. 依最終用途分類-個人買家引領市場

個人買家是 2024 年最大的終端用戶群體,他們根據個人興趣、懷舊情緒或在房地產銷售、古董展覽或網路上購買。

3. 按配銷通路-線下通路仍重要

線下管道,無論是透過傳統拍賣行、古董展銷會、畫廊或房地產拍賣,在2024年仍將佔據最大的市場佔有率,成為最大的市場。即使電子商務的使用日益普及,對物品進行實物檢查、驗證物品是否與描述相符以及進行現場競價的能力仍然吸引了眾多認真的收藏家和投資者。

4. 按地區分類-北美引領全球需求

2022 年,北美在古董和收藏品領域處於領先地位。古董被明確視為文化的一部分,並且擁有豐富的拍賣基礎設施和全國成熟的二級市場。

2024年,北美引領古董和收藏品市場,其拍賣行業發展成熟,擁有眾多高淨值個人收藏家,而體育紀念品、漫畫書和流行文化紀念品的收藏熱潮也推動了這一市場的發展。美國尤其在實體房地產銷售和線上拍賣方面表現強勁,人們對經過認證和評級的收藏品的興趣也日益濃厚。

收藏品和古董產業的主要參與者有蘇富比、佳士得國際、邦瀚斯、Heritage Auctions、RR Auction、Skinner、Invaluable、Julien's Auctions、Lelands、PWCC Marketplace、BiddingForGood、ComicLink、Hake's Americana & Collectibles、The Upperions、Funks、Goldens、Hake's American Upperons、The Upperions、Funks、Hersr、Golders、Mr.

目前,主要參與者正在大力投資NFT的普及、數位化和全球擴張,以利用不斷變化的消費者偏好。蘇富比和佳士得增加了線上拍賣的數量。此外,eBay和PWCC Marketplace正在為分級收藏品建立基於人工智慧的鑑定工具。孩之寶和Funko正在推動授權合作,以滿足流行文化帶來的市場需求。同樣,其他拍賣行,例如RR Auction和邦瀚斯,也在開發精簡的實體-數位混合競價解決方案,為全球收藏家提供參與式、便捷的體驗。這些策略與收藏品經濟數位化和民主化的趨勢一致。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 對藝術和歷史的興趣日益濃厚

- 文化和歷史魅力

- 潛在古董和收藏品的投資

- 可支配所得增加

- 產業陷阱與挑戰

- 身份驗證和出處問題

- 監管和法律挑戰

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品類別

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品類別,2021 - 2034 年

- 主要趨勢

- 美術和繪畫

- 古董家具和裝飾藝術

- 金屬製品及雕塑

- 珠寶和手錶

- 收藏玩具和遊戲

- 書籍、手稿和紙張的短暫性

- 硬幣、貨幣和錢幣學

- 體育紀念品和交易卡

- 樂器及音訊裝置

- 其他(汽車和交通收藏品)

第6章:市場估計與預測:依價格區間,2021 - 2034 年

- 主要趨勢

- 低的

- 中等的

- 高的

第7章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- 個人

- 商業的

- 博物館

- 機構

- 其他

第 8 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 線上

- 專用古董平台

- 電子商務平台

- 離線

- 傳統拍賣行

- 實體經銷商

- 古董展覽會

- 房地產銷售和清算

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- BiddingForGood

- Bonhams

- Christie's International

- ComicLink

- eBay

- Funko

- Golden Auctions

- Hake's Americana & Collectibles

- Hasbro

- Heritage Auctions

- Invaluable

- Julien's Auctions

- Lelands

- PWCC Marketplace

- RR Auction

- Skinner

- Sotheby's

- Stanley Gibbons Group

- The Upper Deck Company

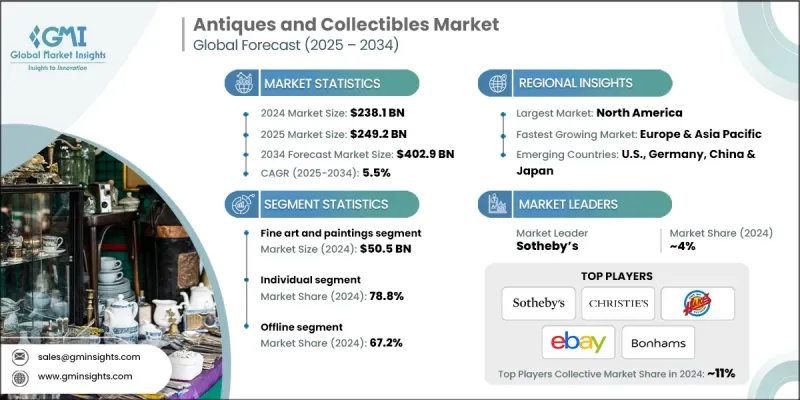

The antiques and collectibles market was valued at USD 238.1 billion in 2024 and is projected to grow from USD 249.2 billion in 2025 to USD 402.9 billion by 2034, at a CAGR of 5.5%, according to the latest report published by Global Market Insights, Inc.

The market growth is supported by a resurgence in nostalgic and vintage products, the expansion of digital auction sites, and increasing interest in non-traditional investments, such as fine art, rare toys, memorabilia, and ancient artifacts. Both mature collectors and the newer generations are fueling demand both online and offline.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $238.1 Billion |

| Forecast Value | $402.9 Billion |

| CAGR | 5.5% |

Key Drivers:

1. Increasing popularity of alternative investments: Collectibles, art, and vintage products are increasingly perceived as a store of value during market instability.

2. Auction digitalization: Mobile apps and internet platforms have expanded access to collectibles worldwide.

3. Growing Appeal of celebrity and pop culture: Collectibles with links to iconic figures, movies, and brands are still attracting big bids.

4. Rise in millennial and Gen Z engagement: Younger generations are adopting collectibles like Pokemon cards, vinyl records, and 90s memorabilia.

Key Players:

- The major players in the antiques and collectibles sector in 2024 are Christie's, Sotheby's, Heritage Auctions, eBay, Bonhams, and Hakes Auctions. In total, these six players have an estimated market share of ~11%.

Key Challenges:

- Authenticity and provenance concerns: Counterfeit risks remain a chief deterrent (especially for high-end and digital collectibles).

- Price uncertainty: Value can fluctuate based on trends or economic changes, which can discourage purchases for consumers (especially those who are risk-averse).

1. By Product Category - Fine Art & Paintings captures the Largest market share

Fine art and paintings took up the largest part of the market in 2024, with an increase in auction prices for both traditional and contemporary art (including original pieces) being made by known artists. Original pieces by recognised artists create demand by 'high net worth' collectors and institutional buyers alike.

2. By End Use - Individual Buyers Lead the Market

Individual buyers made up the largest group of end users in 2024 and bought based on personal interest, nostalgia, or investment value at estate sales, antique shows or on the internet.

3. By Distribution Channel - Offline Channels Remain Important

Offline channels, whether delivered through traditional auction houses, antique fairs, galleries, or estate sales, continued as the largest in 2024, by capturing the largest share of the market. The capacity to physically examine the item, or verify if the item is as described, and live bidding still brings serious collectors and investors to the table, even with the increasing use of e-commerce.

4. By Region - North America Leads Global Demand

North America was the leader in antiques and collectibles in 2022. Antiques are clearly recognized as a part of culture, and there is an abundant infrastructure for auctions and a nationwide established secondary market in place.

North America led the antiques and collectibles market in 2024, with an established auction industry and high-net-worth individual collectors, which was also driven by interest in sports memorabilia, comic books, and pop culture memorabilia. The U.S. specifically experiences strong activity in both in-person estate sales and online auctions, with increasing interest in certified and graded collectibles.

Major players in the collectibles and antiques industry are Sotheby's, Christie's International, Bonhams, Heritage Auctions, RR Auction, Skinner, Invaluable, Julien's Auctions, Lelands, PWCC Marketplace, BiddingForGood, ComicLink, Hake's Americana & Collectibles, The Upper Deck Company, Funko, Golden Auctions, Hasbro, Stanley Gibbons Group, and eBay.

Key players are now making significant investments in NFT adoption, digitalization, and global expansion to capitalize on evolving consumer preferences. Sotheby's and Christie's have boosted the number of online auctions. In addition, eBay and PWCC Marketplace are building AI-based authentication tools for graded collectibles. Hasbro and Funko are moving towards licensing collaborations to meet the market demand spun from pop culture. Likewise, other auction houses, such as RR Auction and Bonhams, are also developing streamlined physical-digital hybrid bidding solutions for participatory, accessible experiences for global collectors. These strategies are consistent with the observed increase in digitization and democratisation of the collectibles economy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product category

- 2.2.3 Price range

- 2.2.4 End use

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing interest in art and history

- 3.2.1.2 Cultural and historical appeal

- 3.2.1.3 Investment of potential antiques and collectibles

- 3.2.1.4 Rising disposable income

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Authentication and provenance issues

- 3.2.2.2 Regulatory and legal challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product category

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Category, 2021 - 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Fine art and paintings

- 5.3 Antique furniture and decorative arts

- 5.4 Metalwork and sculpture

- 5.5 Jewelry and watches

- 5.6 Collectible toys and games

- 5.7 Books, manuscripts, and paper ephemeral

- 5.8 Coins, currency, and numismatics

- 5.9 Sports memorabilia and trading cards

- 5.10 Musical instruments and audio equipment

- 5.11 Others (automotive and transportation collectibles)

Chapter 6 Market Estimates & Forecast, By Price range, 2021 - 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Individual

- 7.3 Commercial

- 7.3.1 Museum

- 7.3.2 Institutions

- 7.3.3 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 Dedicated antique platforms

- 8.2.2 E-commerce platforms

- 8.3 Offline

- 8.3.1 Traditional auction houses

- 8.3.2 Brick-and-mortar dealers

- 8.3.3 Antique fairs and shows

- 8.3.4 Estate sales and liquidations

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 BiddingForGood

- 10.2 Bonhams

- 10.3 Christie’s International

- 10.4 ComicLink

- 10.5 eBay

- 10.6 Funko

- 10.7 Golden Auctions

- 10.8 Hake’s Americana & Collectibles

- 10.9 Hasbro

- 10.10 Heritage Auctions

- 10.11 Invaluable

- 10.12 Julien's Auctions

- 10.13 Lelands

- 10.14 PWCC Marketplace

- 10.15 RR Auction

- 10.16 Skinner

- 10.17 Sotheby's

- 10.18 Stanley Gibbons Group

- 10.19 The Upper Deck Company