|

市場調查報告書

商品編碼

1801825

宗教與精神產品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Religious and Spiritual Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

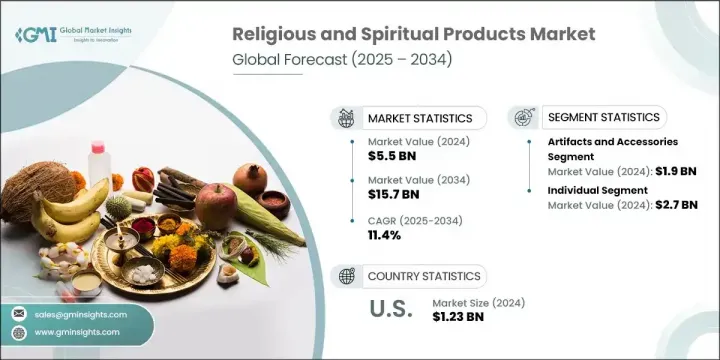

2024年,全球宗教和精神產品市場價值55億美元,預計到2034年將以11.4%的複合年成長率成長,達到157億美元。市場擴張的動力源於不斷發展的精神實踐和道德消費主義的興起,消費者正在尋求與其價值觀產生共鳴的產品。人們對不僅具有精神意義,而且永續的商品的需求日益成長,例如無殘忍儀式蠟燭或環保香。這種轉變使品牌能夠同時吸引傳統用戶和環保意識的消費者,從而釋放出更高的價格潛力。精神產品與健康和保健實踐的結合也增強了產品的相關性。

隨著祈禱和冥想等精神工具因其對心理健康的益處而日益受到青睞,它們被定位為健康必需品,而不是純粹的宗教物品。這種轉變反映了信仰與商業的交融,將象徵性物品轉化為生活風格產品。市場正在超越宗教界限,服務更廣泛關注個人成長、正念和自我關懷的人群。數位化的可及性和精神產品的個人化進一步擴大了其覆蓋範圍,吸引了新一代追求購物意義和便利性的消費者。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 55億美元 |

| 預測值 | 157億美元 |

| 複合年成長率 | 11.4% |

2024年,文物及配件市場產值達19億美元,預計到2034年將以10.1%的複合年成長率成長。諸如聖物、念珠和神像等產品具有強大的文化價值,是不同傳統宗教信仰中不可或缺的一部分。它們在個人崇拜和禮儀禮品中的頻繁使用,使得城鄉地區的需求保持穩定。這些物品還可以客製化、適應不同地區並進行創意設計,使製造商能夠靈活地滿足不同的精神偏好和美學品味。

2024年,個人消費市場規模達27億美元,佔49.1%。個人消費者持續購買精神類產品,用於個人儀式、冥想練習和正念修行。精神自我關懷的興起拓展了產品的相關性,尤其是在尋求情緒健康和日常平衡的年輕消費者群體中。線上購物平台和行動應用程式的便利性提升了產品的可近性,用戶無需依賴傳統零售或機構中介,即可直接探索和購買。香、配件,甚至數位精神內容等產品都根據個人用途進行客製化,提供舒適感、個人化體驗和情感共鳴。

2024年,美國宗教及精神產品市場價值達12.3億美元,預計2025年至2034年期間的複合年成長率將達到10.4%。美國憑藉其濃厚的宗教氛圍和高度的個人精神活動參與度,仍然是最具影響力的市場之一。這種環境支撐了對禮儀用品、精神文學和生活方式配件的需求。宗教自由和機構支持也使得美國市場在文化和政治層面上仍有利於基於信仰的商業活動。精神生活與身心健康的融合進一步刺激了消費。數位商務平台增強了可近性,為不同年齡層和信仰體系的消費者提供了更廣泛的覆蓋範圍和更個人化的購物體驗。

影響全球宗教和精神產品市場的關鍵參與者包括 Divine Hindu、Pujahome、Brown Living、Powerfulhand.com、Rudra India、Indo Divine Spiritual Solutions Pvt. Ltd.、Stuller, Inc.、Mysore Deep Perfumery House、Rgyan Shop、Namoh Indiya、Bolsius International BV、Delsbo Cant、Shuan True宗教和精神產品市場的領導品牌正在透過多樣化的產品線擴大其影響力,這些產品線既滿足傳統信仰習俗,也滿足現代健康習慣。許多公司專注於環保製造,提供可生物分解、無殘忍且符合道德規範的產品,以吸引價值驅動的消費者。客製化選項和特定區域的設計正在實現更深層的消費者聯繫。公司也正在利用數位管道,創造沉浸式電子商務體驗和行動應用程式,以簡化客戶旅程。與精神影響者和健康平台的策略合作正在幫助品牌擴大知名度。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業影響力量

- 成長動力

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區和產品類型

- 監理框架

- 標準和認證

- 環境法規

- 進出口法規

- 波特的分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021-2034 年

- 主要趨勢

- 文物及配件

- 禮儀用品

- 數位產品

- 教科書

- 其他

第6章:市場估計與預測:依最終用途,2021-2034 年

- 主要趨勢

- 個人

- 宗教機構

- 其他

第7章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 線上

- 公司網站

- 電子商務網站

- 離線

- 宗教書店

- 禮品店

- 專賣店

- 其他

第8章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第9章:公司簡介

- Bolsius International BV

- Brown Living

- Delsbo Candle AB

- Divine Hindu

- Indo Divine Spiritual Solutions Pvt. Ltd.

- Mysore Deep Perfumery House

- Namoh Indiya

- Powerfulhand.com

- Prajjwal International

- Pujahome

- Rgyan Shop

- Rudra India

- Shubhkart

- Sounds True Inc.

- Stuller, Inc.

The Global Religious and Spiritual Products Market was valued at USD 5.5 billion in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 15.7 billion by 2034. Market expansion is being fueled by a blend of evolving spiritual practices and the rise of ethical consumerism, where buyers are seeking products that resonate with their values. There's increasing demand for goods that are not only spiritually meaningful but also sustainable, such as cruelty-free ritual candles or environmentally conscious incense. This shift enables brands to appeal to both traditional users and conscious consumers, unlocking premium price potential. The alignment of spiritual products with health and wellness practices is also enhancing product relevance.

As spiritual tools like prayer and meditation gain traction for their mental health benefits, they're being positioned as wellness essentials rather than strictly religious items. This transition reflects how belief and commerce intersect, turning symbolic artifacts into lifestyle products. The market is moving beyond religious boundaries to serve a broader demographic interested in personal growth, mindfulness, and self-care. Digital accessibility and the personalization of spiritual products further increase their reach, attracting a new generation of consumers seeking both meaning and convenience in their purchases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.5 billion |

| Forecast Value | $15.7 billion |

| CAGR | 11.4% |

In 2024, the artifacts and accessories segment generated USD 1.9 billion and is expected to grow at a CAGR of 10.1% through 2034. Products such as sacred symbols, prayer beads, and idols carry strong cultural value and are integral to spiritual routines across diverse traditions. Their frequent use in both personal worship and ceremonial gifting keeps demand steady across urban and rural regions alike. These items also allow for customization, regional adaptation, and creative design, giving manufacturers the flexibility to cater to various spiritual preferences and aesthetic tastes.

The individual segment generated USD 2.7 billion and accounted for 49.1% share in 2024. Individuals consistently purchase spiritual products for their personal rituals, meditation practices, and mindfulness routines. The growth of spiritual self-care has broadened product relevance, especially among younger consumers seeking emotional well-being and daily balance. The convenience of online shopping platforms and mobile applications has enhanced accessibility, allowing users to explore and buy directly without relying on traditional retail or institutional intermediaries. Items like incense, accessories, and even digital spiritual content are being tailored for personal use, offering comfort, personalization, and emotional resonance.

United States Religious and Spiritual Products Market was valued at USD 1.23 billion in 2024 and is projected to grow at a CAGR of 10.4% between 2025 and 2034. The U.S. remains one of the most influential markets due to its strong religious landscape and high level of individual engagement in spiritual activities. This environment supports demand for ceremonial goods, spiritual literature, and lifestyle-based accessories. Religious freedom and institutional support also contribute to a market that remains culturally and politically favorable for faith-based commerce. The integration of spirituality with wellness and mental health routines further fuels consumption. Digital commerce platforms have enhanced accessibility, enabling broader outreach and more personalized shopping experiences for consumers across age groups and belief systems.

Key players influencing the Global Religious and Spiritual Products Market include Divine Hindu, Pujahome, Brown Living, Powerfulhand.com, Rudra India, Indo Divine Spiritual Solutions Pvt. Ltd., Stuller, Inc., Mysore Deep Perfumery House, Rgyan Shop, Namoh Indiya, Bolsius International BV, Delsbo Candle AB, Shubhkart, Sounds True Inc., and Prajjwal International. Leading brands in the religious and spiritual products market are expanding their footprint through diversified product lines that cater to both traditional faith practices and modern wellness routines. Many companies are focusing on eco-conscious manufacturing, offering biodegradable, cruelty-free, and ethically sourced goods to attract value-driven consumers. Customization options and region-specific designs are enabling deeper consumer connection. Firms are also leveraging digital channels, creating immersive e-commerce experiences and mobile apps that streamline the customer journey. Strategic collaborations with spiritual influencers and wellness platforms are helping brands expand their visibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 End use

- 2.2.3 Distribution channel

- 2.2.4 Regional

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region and product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 -2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Artifacts and accessories

- 5.3 Ceremonial items

- 5.4 Digital products

- 5.5 Textbooks

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End Use, 2021 -2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Individual

- 6.3 Religious institutions

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 -2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Online

- 7.2.1 Company website

- 7.2.2 E-commerce website

- 7.3 Offline

- 7.3.1 Religious bookstores

- 7.3.2 Gift shops

- 7.3.3 Specialty stores

- 7.3.4 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 -2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Bolsius International BV

- 9.2 Brown Living

- 9.3 Delsbo Candle AB

- 9.4 Divine Hindu

- 9.5 Indo Divine Spiritual Solutions Pvt. Ltd.

- 9.6 Mysore Deep Perfumery House

- 9.7 Namoh Indiya

- 9.8 Powerfulhand.com

- 9.9 Prajjwal International

- 9.10 Pujahome

- 9.11 Rgyan Shop

- 9.12 Rudra India

- 9.13 Shubhkart

- 9.14 Sounds True Inc.

- 9.15 Stuller, Inc.