|

市場調查報告書

商品編碼

1801908

糖尿病護理設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Diabetes Care Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

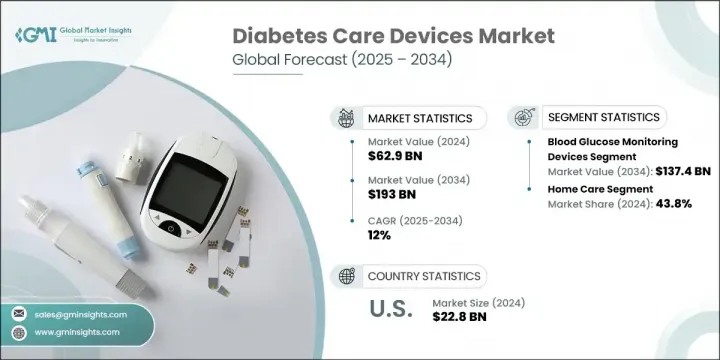

2024年,全球糖尿病護理設備市場規模達629億美元,預計2034年將以12%的複合年成長率成長,達到1,930億美元。這一成長主要源於全球糖尿病負擔的增加、持續的技術突破以及公共和私營部門資金的增加。糖尿病照護設備是重要的醫療工具,透過有效的血糖監測和胰島素給藥,幫助患者管理糖尿病。隨著全球糖尿病患者數量的持續成長,對可靠且方便用戶使用的護理設備的需求也持續成長。

致力於降低這些工具的侵入性、提高準確性和成本效益的創新正在推動需求成長。各公司正大力投資研發,以推出能確保更舒適和疾病管理的先進設備。市場也正在向更智慧、整合的解決方案轉變,這些解決方案能夠提供無縫的血糖追蹤和胰島素輸送,以滿足日益成長的消費者期望。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 629億美元 |

| 預測值 | 1930億美元 |

| 複合年成長率 | 12% |

2024年,血糖監測設備市場規模達422億美元,預計2034年將達到1,374億美元,複合年成長率為12.7%。這些設備在醫院、診斷實驗室和家庭護理機構的廣泛應用支撐了這一成長。動態血糖監測儀(CGM)和自我監測儀等設備提供持續更新,幫助使用者根據即時血糖資料調節生活方式、食物攝取和胰島素給藥方案。定期監測對於避免血糖水平突然飆升或下降至關重要,因為血糖水平突然下降可能導致嚴重的健康問題。這些工具提供全天候回饋,確保使用者在糖尿病管理方面保持主動性,並最大限度地減少長期併發症。

2024年,家庭護理市場佔了43.8%的佔有率。居家管理糖尿病已成為許多人的一大便利,無需頻繁就診。如今,家用設備的功能已與專業設備相媲美。即時血糖趨勢分析、警報和資料追蹤等進階功能可幫助患者快速、明智地決定食物攝取量、胰島素劑量和日常習慣。居家糖尿病管理的這種日益成長的趨勢,持續吸引那些尋求獨立生活和提升生活品質的人。

2024年,美國糖尿病護理設備市場規模達228億美元。強勁成長得益於糖尿病患者數量的成長以及創新糖尿病技術的快速普及。老齡化人口更容易患慢性病,進一步加劇了對高效糖尿病管理解決方案的需求。該地區市場的發展勢頭得益於高階醫療基礎設施的普及、優惠的報銷方案以及消費者對預防保健和早期診斷的認知。

影響全球糖尿病照護設備市場的關鍵公司包括 Tandem Diabetes Care、Becton、Dickinson and Company、Ypsomed Holding、Insulet、Sanofi、Dr. Reddy's Laboratories、Medtronic、Dexcom、Ascensia Diabetes Care、Sinocare、Platinum Equity Advisors、Abbott Company Laborator Advisors、Evo、Eunyet, 或Ekario、Equity Advisors. Nordisk、F. Hoffmann-La Roche、Bionime 和 Nova Biomedical。糖尿病護理設備市場的領導者正致力於加強產品創新和產品組合多樣化,以滿足用戶不斷變化的需求。該公司正在推出具有即時資料分析和藍牙連接功能的智慧穿戴設備,以改善血糖追蹤。與數位健康平台的策略合作有助於將資料整合到更廣泛的健康生態系統中。併購也被用來擴大地理覆蓋範圍和獲取新的客戶群。持續的研發投資確保設備侵入性更小、更準確、更易於使用。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 全球糖尿病盛行率不斷上升

- 糖尿病照護設備的技術進步日新月異

- 公共和私人組織增加對糖尿病護理的投資

- 產業陷阱與挑戰

- 糖尿病照護設備成本高昂

- 嚴格的監管框架

- 市場機會

- 新興市場的擴張

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 技術進步

- 當前的技術趨勢

- 新興技術

- 供應鏈和分銷分析

- 報銷場景

- 編碼和報銷

- 胰島素輸送系統的報銷政策和公共醫療部門保險覆蓋範圍

- 美國

- 歐洲

- 2024年定價分析

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 血糖監測設備

- 自我監測血糖儀

- 連續血糖監測儀

- 測試條

- 刺血針

- 胰島素輸送裝置

- 胰島素幫浦

- 管式幫浦

- 無內胎幫浦

- 鋼筆

- 可重複使用的

- 一次性的

- 筆針

- 標準

- 安全

- 注射器

- 其他胰島素輸送裝置

- 胰島素幫浦

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 診斷中心

- 居家護理

- 其他最終用途

第7章:市場估計與預測:按國家/地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 比利時

- 丹麥

- 芬蘭

- 挪威

- 立陶宛

- 拉脫維亞

- 愛沙尼亞

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 埃及

- 以色列

- 科威特

- 卡達

第8章:公司簡介

- Abbott Laboratories

- ARKRAY

- Ascensia Diabetes Care

- B. Braun Melsungen

- Becton, Dickinson and Company

- Bionime

- DarioHealth

- Dexcom

- Dr. Reddy's Laboratories

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Insulet

- Medtronic

- Nova Biomedical

- Novo Nordisk

- Pendiq

- Platinum Equity Advisors

- Sanofi

- Sinocare

- Tandem Diabetes Care

- Ypsomed Holding

The Global Diabetes Care Devices Market was valued at USD 62.9 billion in 2024 and is estimated to grow at a CAGR of 12% to reach USD 193 billion by 2034. This growth is driven by the rising global diabetes burden, continuous technological breakthroughs, and increased funding from both public and private sectors. Diabetes care devices are essential medical tools that support individuals in managing diabetes by enabling effective blood glucose monitoring and insulin administration. As the number of individuals living with diabetes continues to rise worldwide, the demand for reliable and user-friendly care devices continues to grow.

Innovations focused on making these tools less invasive, more accurate, and cost-effective are propelling demand. Companies are investing heavily in R&D to bring forward advanced devices that ensure better comfort and disease management. The market is also experiencing a shift toward smarter, integrated solutions that provide seamless glucose tracking and insulin delivery to meet growing consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $62.9 Billion |

| Forecast Value | $193 Billion |

| CAGR | 12% |

In 2024, the blood glucose monitoring devices segment generated USD 42.2 billion and projected to hit USD 137.4 billion by 2034, growing at a CAGR of 12.7%. Their extensive use in hospitals, diagnostic labs, and homecare setups underpins this growth. Devices like CGMs and self-monitoring meters offer continuous updates, helping users regulate their lifestyle, food intake, and insulin schedules based on real-time glucose data. Regular monitoring is vital to avoid spikes or drops in glucose levels, which can lead to serious health issues. These tools provide round-the-clock feedback, ensuring users remain proactive in their diabetes management and minimizing long-term complications.

The home care segment held 43.8% share in 2024. The ability to manage diabetes at home has become a crucial convenience for many, eliminating the need for frequent clinical visits. Devices designed for home use now offer similar capabilities as those used in professional settings. Advanced features like real-time glucose trend analysis, alarms, and data tracking help patients make quick and informed decisions about food intake, insulin doses, and daily routines. This growing trend of home-based diabetes management continues to attract individuals looking for independence and improved quality of life.

United States Diabetes Care Devices Market generated USD 22.8 billion in 2024. This strong performance is due to the growing diabetic population and the rapid adoption of innovative diabetes technologies. An aging population more prone to chronic conditions further intensifies demand for efficient diabetes management solutions. The market's momentum in the region is supported by access to high-end healthcare infrastructure, favorable reimbursement scenarios, and consumer awareness around preventative care and early diagnosis.

Key companies influencing the Global Diabetes Care Devices Market include Tandem Diabetes Care, Becton, Dickinson and Company, Ypsomed Holding, Insulet, Sanofi, Dr. Reddy's Laboratories, Medtronic, Dexcom, Ascensia Diabetes Care, Sinocare, Platinum Equity Advisors, Abbott Laboratories, ARKRAY, DarioHealth, Eli Lilly and Company, Pendiq, Novo Nordisk, F. Hoffmann-La Roche, Bionime, and Nova Biomedical. Leading players in the diabetes care devices market are focusing on enhancing product innovation and portfolio diversification to meet the evolving needs of users. Companies are introducing smart, wearable devices with real-time data analytics and Bluetooth connectivity to improve glucose tracking. Strategic collaborations with digital health platforms help integrate data into broader health ecosystems. Mergers and acquisitions are also being used to expand geographic presence and access new customer bases. Continuous investments in R&D ensure devices become less invasive, more accurate, and easier to use.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of diabetes across the world

- 3.2.1.2 Rising technological advancements in diabetes care devices

- 3.2.1.3 Increasing investments by public and private organizations for diabetes care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diabetes care devices

- 3.2.2.2 Rigorous regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain and distribution analysis

- 3.7 Reimbursement scenario

- 3.7.1 Coding and reimbursement

- 3.7.2 Reimbursement policies and public healthcare sector insurance coverage for insulin delivery systems

- 3.7.2.1 U.S.

- 3.7.2.2 Europe

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood glucose monitoring devices

- 5.2.1 Self-monitoring blood glucose meters

- 5.2.2 Continuous glucose monitors

- 5.2.3 Testing strips

- 5.2.4 Lancets

- 5.3 Insulin delivery devices

- 5.3.1 Insulin pumps

- 5.3.1.1 Tubed pumps

- 5.3.1.2 Tubeless pumps

- 5.3.2 Pens

- 5.3.2.1 Reusable

- 5.3.2.2 Disposable

- 5.3.3 Pen needles

- 5.3.3.1 Standard

- 5.3.3.2 Safety

- 5.3.4 Syringes

- 5.3.5 Other insulin delivery devices

- 5.3.1 Insulin pumps

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospital

- 6.3 Ambulatory surgical centres

- 6.4 Diagnostic centres

- 6.5 Homecare

- 6.6 Other end use

Chapter 7 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.3.7 Sweden

- 7.3.8 Belgium

- 7.3.9 Denmark

- 7.3.10 Finland

- 7.3.11 Norway

- 7.3.12 Lithuania

- 7.3.13 Latvia

- 7.3.14 Estonia

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Colombia

- 7.5.5 Chile

- 7.5.6 Peru

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

- 7.6.4 Turkey

- 7.6.5 Egypt

- 7.6.6 Israel

- 7.6.7 Kuwait

- 7.6.8 Qatar

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 ARKRAY

- 8.3 Ascensia Diabetes Care

- 8.4 B. Braun Melsungen

- 8.5 Becton, Dickinson and Company

- 8.6 Bionime

- 8.7 DarioHealth

- 8.8 Dexcom

- 8.9 Dr. Reddy’s Laboratories

- 8.10 Eli Lilly and Company

- 8.11 F. Hoffmann-La Roche

- 8.12 Insulet

- 8.13 Medtronic

- 8.14 Nova Biomedical

- 8.15 Novo Nordisk

- 8.16 Pendiq

- 8.17 Platinum Equity Advisors

- 8.18 Sanofi

- 8.19 Sinocare

- 8.20 Tandem Diabetes Care

- 8.21 Ypsomed Holding

糖尿病醫療設備市場規模、佔有率和趨勢分析報告:按類型、分銷管道、最終用途、地區和細分市場預測(2026-2033 年)

糖尿病醫療設備市場規模、佔有率和趨勢分析報告:按類型、分銷管道、最終用途、地區和細分市場預測(2026-2033 年) 糖尿病照護設備:市場趨勢、競爭格局與市場預測(至2034年)

糖尿病照護設備:市場趨勢、競爭格局與市場預測(至2034年) 糖尿病護理設備市場:2026年至2032年全球市場預測(按設備類型、技術、給藥方法、胰島素類型、分銷管道和最終用戶分類)

糖尿病護理設備市場:2026年至2032年全球市場預測(按設備類型、技術、給藥方法、胰島素類型、分銷管道和最終用戶分類) 糖尿病護理設備市場規模、佔有率、趨勢和預測:按類型、分銷管道、最終用戶和地區分類,2026-2034 年

糖尿病護理設備市場規模、佔有率、趨勢和預測:按類型、分銷管道、最終用戶和地區分類,2026-2034 年 2026年全球糖尿病護理設備市場報告

2026年全球糖尿病護理設備市場報告 全球糖尿病護理設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本糖尿病設備市場報告(按類型(管理設備、監測設備)、配銷通路(醫院藥房、零售藥房、糖尿病診所/中心、線上藥房及其他)和地區分類,2026-2034 年)

全球糖尿病護理設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本糖尿病設備市場報告(按類型(管理設備、監測設備)、配銷通路(醫院藥房、零售藥房、糖尿病診所/中心、線上藥房及其他)和地區分類,2026-2034 年) 糖尿病護理設備和藥品市場規模、佔有率和成長分析(按類型、通路、最終用途和地區分類)—2026-2033年行業預測

糖尿病護理設備和藥品市場規模、佔有率和成長分析(按類型、通路、最終用途和地區分類)—2026-2033年行業預測 全球糖尿病護理設備市場(按產品類型、疾病類型、患者治療設施和地區分類)- 預測至 2030 年

全球糖尿病護理設備市場(按產品類型、疾病類型、患者治療設施和地區分類)- 預測至 2030 年 全球糖尿病護理設備市場

全球糖尿病護理設備市場