|

市場調查報告書

商品編碼

1801797

乳製品及大豆食品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dairy and Soy Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

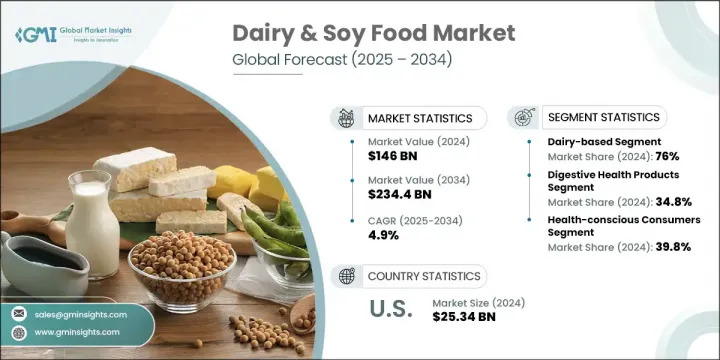

2024 年全球乳製品和大豆食品市場價值為 1,460 億美元,預計到 2034 年將以 4.9% 的複合年成長率成長至 2,344 億美元。市場涵蓋的產品種類繁多,包括牛奶、優格和起司等乳製品,以及植物性飲料和大豆替代品。這一成長背後的一個關鍵驅動力是消費者對健康和保健的日益關注。人們對添加劑最少、功能性較強的營養產品的需求日益成長。隨著乳糖不耐症變得越來越普遍,許多消費者開始轉向具有與傳統乳製品相同口味、質地和營養價值的植物性食品。

植物性飲食和純素飲食的興起引發了該領域的重大創新,各大公司紛紛拓展產品組合,推出新型優格、植物性飲料和強化食品,瞄準純素食者、彈性素食者和注重環保的消費者。已開發國家人口老化也刺激了對強化乳製品和大豆食品的需求,尤其是那些富含蛋白質、維生素和益生菌的食品,這些食品有助於骨骼健康、消化功能和整體活力。同時,電子商務的快速發展也提高了產品的可及性,使品牌能夠觸及更多消費者,並提供更豐富的產品種類。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1460億美元 |

| 預測值 | 2344億美元 |

| 複合年成長率 | 4.9% |

2024 年,乳製品類健康食品佔最大佔有率,達到 76%,預計到 2034 年將維持 5.3% 的成長率。這些產品吸引了注重腸道健康、免疫力和骨骼強度的健康消費者,其開發創新旨在降低脂肪和糖的含量,同時增加飲食限制人群的可及性。

2024年,消化健康產品領域佔了34.8%的市場佔有率,預計到2034年成長率將達到5.5%。這一迅猛成長主要源於消費者對腸道健康和增強免疫系統的日益關注,越來越多的人尋求兼具營養和功能的產品。隨著消化健康問題在全球日益普遍,從腹脹、消化不良到腸躁症(IBS)等更為複雜的疾病,消費者開始轉向能夠促進消化和整體腸道菌叢平衡的食品和補充劑。

2024年,美國乳製品和大豆食品市場產值達253.4億美元。預計到2034年,美國市場的複合年成長率將達到6.4%,這得益於消費者對注重安全、營養成分透明和便利產品形式的品牌的信任。有機、無麩質和植物性產品的日益普及,進一步推動了美國市場的發展。

全球乳製品和大豆食品市場的領先公司包括達能公司、聯合利華、拉克塔利斯集團、恆天然合作集團、Hain Celestial 集團、菲仕蘭坎皮納、通用磨坊、迪安食品公司、Arla Foods amba、Silk(達能)、雀巢公司、卡夫亨氏公司、養樂多本社、WhiteWave Foods(達能)和家樂氏公司。為了鞏固其在競爭激烈的乳製品和大豆食品領域的地位,各公司實施了各種策略。這些措施包括不斷改進產品配方以滿足消費者不斷變化的偏好,例如提供低糖、高蛋白和無乳糖的選擇。許多公司已經擴大了他們的產品線,包括植物性替代品,以滿足對純素食和彈性素食日益成長的需求。合作、收購和生產流程創新也是多元化產品組合和提高產品可及性的關鍵策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 增強健康意識

- 乳糖不耐症盛行率上升

- 植物性飲食的採用和素食主義的成長

- 蛋白質強化與營養強化需求

- 產業陷阱與挑戰

- 傳統乳業競爭

- 特色保健產品價格溢價

- 市場機會

- 新興市場健康意識增強

- 功能性食品與營養保健品的整合

- 個人化營養和客製化

- 電子商務和直接面對消費者的成長

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品類別

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品類別,2021-2034 年

- 主要趨勢

- 乳製品健康食品

- 益生菌乳製品

- 富含蛋白質的乳製品

- 功能性乳製品

- 大豆食品

- 傳統大豆食品

- 豆奶及飲料

- 大豆蛋白製品

- 組合和混合產品

- 乳製品和大豆混合產品

- 多蛋白配方

- 功能性食品組合

- 特殊營養產品

第6章:市場估計與預測:依健康效益,2021-2034 年

- 主要趨勢

- 消化健康產品

- 益生菌和益生元食品

- 增強消化酶

- 腸道健康支持產品

- 骨骼和關節健康

- 富鈣產品

- 維生素D強化食品

- 骨骼健康支持配方

- 心臟保健產品

- 膽固醇管理食品

- Omega-3 增強產品

- 有益心臟健康的配方

- 蛋白質和肌肉健康

- 高蛋白產品

- 肌肉恢復配方

- 運動營養整合

- 體重管理

- 低熱量、低脂肪

- 增強飽足感的產品

- 代謝支持配方

第7章:市場估計與預測:依消費者細分,2021-2034

- 主要趨勢

- 注重健康的消費者

- 飲食限制部分

- 基於年齡的細分

- 兒童及青少年營養

- 成人健康與保健

- 老年營養與護理

- 基於生活方式的細分

- 忙碌的專業人士

- 有機和天然偏好

- 高階和手工消費者

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Arla Foods amba

- Danone SA

- Dean Foods Company

- Fonterra Co-operative Group

- FrieslandCampina

- General Mills, Inc.

- Hain Celestial Group, Inc.

- Kellogg Company

- Lactalis Group

- Nestle SA

- Silk (Danone)

- The Kraft Heinz Company

- Unilever PLC

- WhiteWave Foods (Danone)

- Yakult Honsha Co., Ltd.

The Global Dairy & Soy Food Market was valued at USD 146 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 234.4 billion by 2034. This market spans a broad range of products, including dairy items like milk, yogurt, and cheese, as well as plant-based beverages and soy alternatives. A key driver behind this growth is the increasing focus on health and wellness among consumers. There is a growing demand for nutritious products with minimal additives and more functional benefits. As lactose intolerance becomes more common, many consumers are turning to plant-based options that offer the same taste, texture, and nutritional value as traditional dairy products.

The rise of plant-based and vegan diets has sparked significant innovation in this space, with companies diversifying their portfolios to include new types of yogurt, plant-based beverages, and fortified goods aimed at vegans, flexitarians, and environmentally conscious shoppers. The aging population in developed countries is also fueling demand for fortified dairy and soy foods, particularly those enriched with proteins, vitamins, and probiotics to support bone health, digestion, and overall vitality. Meanwhile, the rapid growth of e-commerce is improving product accessibility, allowing brands to reach more consumers and offer a wider variety of products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $146 Billion |

| Forecast Value | $234.4 Billion |

| CAGR | 4.9% |

In 2024, dairy-based health foods segment held the largest share at 76% and is expected to maintain a growth rate of 5.3% through 2034. These products, which appeal to health-conscious consumers focused on gut health, immunity, and bone strength, are being developed with innovations aimed at reducing fat and sugar content while increasing accessibility for individuals with dietary restrictions.

The digestive health products segment captured a significant 34.8% share of the market in 2024, with an anticipated growth rate of 5.5% through to 2034. This impressive expansion is largely driven by an increasing consumer focus on gut health and immune system enhancement, as more individuals seek products that offer both nutritional and functional benefits. As digestive health issues become more prevalent globally, from bloating and indigestion to more complex conditions like IBS, consumers are turning to foods and supplements that promote better digestion and overall gut flora balance.

United States Dairy and Soy Food Market generated USD 25.34 billion in 2024. The country's market is expected to grow at a CAGR of 6.4% by 2034, driven by consumer trust in brands that prioritize safety, transparency in nutritional labeling, and convenient product formats. The increasing popularity of organic, gluten-free, and plant-based products has further propelled the U.S. market forward.

Leading companies in the Global Dairy and Soy Food Market include Danone S.A., Unilever PLC, Lactalis Group, Fonterra Co-operative Group, Hain Celestial Group, Inc., FrieslandCampina, General Mills, Inc., Dean Foods Company, Arla Foods amba, Silk (Danone), Nestle S.A., The Kraft Heinz Company, Yakult Honsha Co., Ltd., WhiteWave Foods (Danone), and Kellogg Company. To solidify their position in the competitive dairy and soy food sector, companies have implemented various strategies. These include continuous product reformulations to meet evolving consumer preferences, such as offering lower sugar, high-protein, and lactose-free options. Many companies have expanded their product lines to include plant-based alternatives, tapping into the growing demand for vegan and flexitarian choices. Partnerships, acquisitions, and innovation in production processes have also been key strategies to diversify portfolios and improve product accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product category

- 2.2.3 Health benefit

- 2.2.4 Consumer segment

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing health and wellness consciousness

- 3.2.1.2 Rising prevalence of lactose intolerance

- 3.2.1.3 Plant-based diet adoption and veganism growth

- 3.2.1.4 Protein enrichment and nutritional enhancement demands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Traditional dairy industry competition

- 3.2.2.2 Price premium for specialty health products

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market health awareness growth

- 3.2.3.2 Functional food and nutraceutical integration

- 3.2.3.3 Personalized nutrition and customization

- 3.2.3.4 E-commerce and direct-to-consumer growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Category, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based health foods

- 5.2.1 Probiotic dairy products

- 5.2.2 Protein-enriched dairy

- 5.2.3 Functional dairy products

- 5.3 Soy-based food products

- 5.3.1 Traditional soy foods

- 5.3.2 Soy milk and beverages

- 5.3.3 Soy protein products

- 5.4 Combination and hybrid products

- 5.4.1 Dairy-soy blend products

- 5.4.2 Multi-protein formulations

- 5.4.3 Functional food combinations

- 5.4.4 Specialty nutritional products

Chapter 6 Market Estimates and Forecast, By Health Benefit, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Digestive health products

- 6.2.1 Probiotic and prebiotic foods

- 6.2.2 Digestive enzyme enhanced

- 6.2.3 Gut health support products

- 6.3 Bone and joint health

- 6.3.1 Calcium-enriched products

- 6.3.2 Vitamin D fortified foods

- 6.3.3 Bone health support formulations

- 6.4 Heart health products

- 6.4.1 Cholesterol management foods

- 6.4.2 Omega-3 enhanced products

- 6.4.3 Heart-healthy formulations

- 6.5 Protein and muscle health

- 6.5.1 High-protein products

- 6.5.2 Muscle recovery formulations

- 6.5.3 Sports nutrition integration

- 6.6 Weight management

- 6.6.1 Low-calorie and reduced-fat

- 6.6.2 Satiety-enhancing products

- 6.6.3 Metabolic support formulations

Chapter 7 Market Estimates and Forecast, By Consumer Segment, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Health-conscious consumers

- 7.3 Dietary restriction segments

- 7.4 Age-based segments

- 7.4.1 Children and adolescent nutrition

- 7.4.2 Adult health and wellness

- 7.4.3 Senior nutrition and care

- 7.5 Lifestyle-based segments

- 7.5.1 Busy professional

- 7.5.2 Organic and natural preference

- 7.5.3 Premium and artisanal consumers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arla Foods amba

- 9.2 Danone S.A.

- 9.3 Dean Foods Company

- 9.4 Fonterra Co-operative Group

- 9.5 FrieslandCampina

- 9.6 General Mills, Inc.

- 9.7 Hain Celestial Group, Inc.

- 9.8 Kellogg Company

- 9.9 Lactalis Group

- 9.10 Nestle S.A.

- 9.11 Silk (Danone)

- 9.12 The Kraft Heinz Company

- 9.13 Unilever PLC

- 9.14 WhiteWave Foods (Danone)

- 9.15 Yakult Honsha Co., Ltd.