|

市場調查報告書

商品編碼

1797812

汽車光學感測器 IC 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Optical Sensor IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

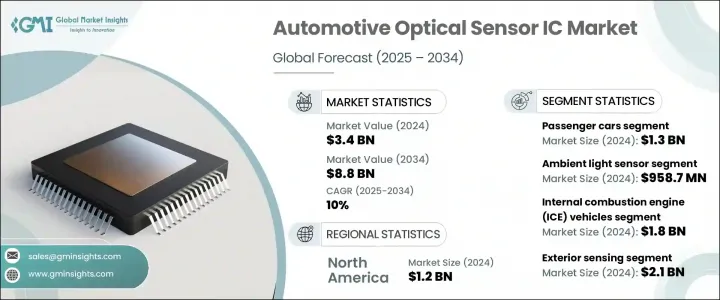

2024年,全球汽車光學感測器IC市場規模達34億美元,預計2034年將以10%的複合年成長率成長,達到88億美元。這一成長主要得益於技術的快速進步、駕駛輔助系統需求的不斷成長以及自動駕駛汽車的不斷發展。汽車光學感測器在汽車中的應用日益廣泛,以提高安全性、舒適性和性能,這推動了市場需求的成長。汽車製造商面臨越來越大的壓力,需要滿足不斷變化的監管安全要求,這促使他們在現代車輛中整合複雜的感測組件。

汽車產業正日益青睞光學感測器 IC,因為它們在增強先進駕駛輔助系統(ADAS) 方面發揮著重要作用。自適應巡航控制、車道維持和盲點監控等功能都嚴重依賴這些感測器。汽車系統日益複雜,消費者對更智慧、更安全、更直覺的駕駛體驗的期望也日益提升,這顯著提升了對精準高性能感測器技術的需求。光學感測器尤其因其速度快、精度高以及在各種光照和環境條件下都能有效工作的能力而備受推崇。隨著越來越多的原始設備製造商 (OEM) 致力於滿足嚴格的安全基準並提供優質的駕駛體驗,光學感測器 IC 的應用正在迅速擴展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 34億美元 |

| 預測值 | 88億美元 |

| 複合年成長率 | 10% |

就車型而言,乘用車市場引領全球市場,2024 年市場價值達 13 億美元。該領域對高階功能(包括增強安全性、舒適性和內裝美觀性)的需求日益成長,促使汽車製造商整合更多基於光學感測器的系統。感測器 IC 正被嵌入到汽車中,以支援從自動大燈到座艙燈光調節等各種應用,這與日益成長的智慧出行解決方案需求相契合。隨著電動和自動駕駛乘用車的持續成長,對光學感測器 IC 的依賴預計將大幅成長。

按感測器類型分類,環境光感測器佔據了最大的市場佔有率,到2024年將達到9.587億美元。這些感測器對於即時調節車輛內外照明至關重要,從而提高可視性、減少干擾並提升整體駕駛舒適度。人們對能夠適應不斷變化的環境的方便用戶使用型照明系統的需求日益成長,這推動了環境光感測器在各種車型中的持續應用。

根據應用,汽車光學感測器 IC 市場分為內部感測和外部感測。其中,外部感測領域佔據主導地位,2024 年市場價值達 21 億美元。外部感測技術用於監測周圍環境、偵測附近物體並動態響應路況。這些功能對於支援行人偵測、緊急煞車和盲點識別等系統至關重要。包括LiDAR、紅外線和攝影機模組在內的光學感測器是這些功能的核心。外部應用對堅固耐用、防水且精確的感測器的需求持續成長,尤其是在汽車製造商優先考慮高性能駕駛輔助功能以符合全球安全標準和新車評估程序 (NCAP) 的情況下。

從區域來看,北美市場佔據主導地位,2024 年市場規模達 12 億美元。該地區擁有完善的車輛安全監管框架,以及先進的自動駕駛和電動車發展生態系統。在美國,2024 年市場規模達 9.104 億美元,複合年成長率為 10.5%。預計支持國內半導體生產的政策措施將在未來幾年顯著影響汽車感測器元件的供應和成本效益,進一步促進市場擴張。

汽車光學感測器 IC 市場的主要公司包括松下公司、安森美半導體公司、邁來芯公司、奧托立夫公司、亞德諾半導體公司、意法半導體公司、豪威科技公司、博通公司、英偉達公司、英飛凌科技股份公司、羅伯特·博世有限公司、美國微晶片科技公司、股份集團、安波福公司、艾邁斯公司公司、德州儀器公司、恩智浦半導體公司、濱松光子株式會社和電裝株式會社。這些公司專注於感測技術創新、晶片性能提升以及與汽車原始設備製造商的合作,以在不斷變化的市場環境中保持競爭力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 先進駕駛輔助系統(ADAS) 的採用率不斷提高

- 自動駕駛汽車發展的成長

- 加強道路安全監管要求

- 消費者對增強車載體驗的需求

- 對感測器技術進步的需求不斷成長

- 陷阱與挑戰

- 開發和實施成本高

- 與現有系統的整合複雜性

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按感測器類型,2021 - 2034 年

- 主要趨勢

- 環境光感測器

- 紅外線(IR)感測器

- LiDAR感測器

- 接近感測器

- 雨水和陽光感測器

- 其他

第6章:市場估計與預測:按車輛類型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第7章:市場估計與預測:按推進類型,2021 - 2034 年

- 主要趨勢

- 電動車(EV)

- 內燃機(ICE)車輛

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 內部感測

- 外部感測

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- AMS-OSRAM AG

- Analog Devices, Inc.

- Aptiv PLC

- Autoliv Inc.

- Broadcom Inc.

- Continental AG

- Denso Corporation

- Hamamatsu Photonics KK

- Infineon Technologies AG

- LeddarTech Inc.

- Melexis NV

- Microchip Technology Inc.

- NVIDIA Corporation

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Omnivision Technologies, Inc.

- Panasonic Corporation

- Robert Bosch GmbH

- STMicroelectronics NV

- Texas Instruments Incorporated

The Global Automotive Optical Sensor IC Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 8.8 billion by 2034. The growth is driven by rapid technological advancement, increased demand for driver assistance systems, and the evolution of autonomous vehicles. The demand is primarily being fueled by the expanding adoption of optical sensors in automobiles for safety, comfort, and performance enhancements. Automakers are under increasing pressure to meet evolving regulatory safety mandates, which is contributing to the integration of sophisticated sensing components in modern vehicles.

The automotive sector is increasingly turning to optical sensor ICs due to their role in enhancing advanced driver assistance systems (ADAS). Features such as adaptive cruise control, lane keeping, and blind spot monitoring rely heavily on these sensors. The growing complexity of automotive systems and rising consumer expectations for smarter, safer, and more intuitive driving experiences have significantly increased the need for precise and high-performance sensor technologies. Optical sensors, in particular, are highly valued for their speed, accuracy, and ability to function effectively under diverse lighting and environmental conditions. As more OEMs aim to meet stringent safety benchmarks and offer premium vehicle experiences, the use of optical sensor ICs is rapidly expanding.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 10% |

In terms of vehicle type, the passenger cars segment led the global market and was valued at USD 1.3 billion in 2024. The increasing demand for high-end features in this segment, including enhanced safety, comfort, and interior aesthetics, is encouraging automakers to integrate more optical sensor-based systems. Sensor ICs are being embedded to support applications ranging from automated headlights to cabin light adjustments, aligning with the growing push towards smart mobility solutions. As electric and autonomous passenger cars continue to gain traction, the reliance on optical sensor ICs is anticipated to grow substantially.

When categorized by sensor type, ambient light sensors commanded the largest market share, reaching USD 958.7 million in 2024. These sensors are vital for adjusting both internal and external vehicle lighting in real-time, thereby improving visibility, reducing distractions, and enhancing overall driving comfort. The rising demand for user-friendly lighting systems that adapt to changing environments is fostering the continued adoption of ambient light sensors across various vehicle models.

By application, the automotive optical sensor IC market is divided into interior and exterior sensing. Among these, the exterior sensing segment dominated with a market value of USD 2.1 billion in 2024. Exterior sensing technologies are used to monitor surroundings, detect nearby objects, and respond dynamically to road conditions. These functions are crucial for supporting systems such as pedestrian detection, emergency braking, and blind spot recognition. Optical sensors, including LiDAR, infrared, and camera modules, are at the core of these capabilities. The need for robust, water-resistant, and accurate sensors for external applications continues to rise, especially as vehicle manufacturers prioritize high-performance driver assistance features to comply with global safety standards and New Car Assessment Programs (NCAP).

Regionally, North America stood out as the dominant market, accounting for USD 1.2 billion in 2024. The region benefits from a strong regulatory framework supporting vehicle safety and an advanced ecosystem for the development of autonomous and electric vehicles. In the United States, the market reached a valuation of USD 910.4 million in 2024, growing at a CAGR of 10.5%. Policy initiatives to support domestic semiconductor production are expected to significantly impact the availability and cost-efficiency of automotive sensor components in the coming years, further bolstering market expansion.

Key companies operating in the automotive optical sensor IC market include Panasonic Corporation, ON Semiconductor Corporation, Melexis NV, Autoliv Inc., Analog Devices, Inc., STMicroelectronics N.V., Omnivision Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Infineon Technologies AG, Robert Bosch GmbH, Microchip Technology Inc., Continental AG, Aptiv PLC, ams-OSRAM AG, LeddarTech Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., Hamamatsu Photonics K.K., and Denso Corporation. These players are focusing on innovations in sensing technology, improved chip performance, and partnerships with automotive OEMs to stay competitive in the evolving landscape.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Propulsion type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of advanced driver assistance systems (ADAS)

- 3.2.1.2 Growth of autonomous vehicle development

- 3.2.1.3 Increasing road safety regulatory mandates

- 3.2.1.4 Consumer demand for enhanced in-vehicle experiences

- 3.2.1.5 Growing demand for advancements in sensor technology

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High development and implementation costs

- 3.2.2.2 Integration complexity with existing systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Sensor Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Ambient light sensors

- 5.3 Infrared (IR) sensors

- 5.4 Lidar sensors

- 5.5 Proximity sensors

- 5.6 Rain and sunlight sensors

- 5.7 Others

Chapter 6 Market estimates and forecast, by Vehicle Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Light commercial vehicle (LCV)

- 6.4 Medium commercial vehicle (MCV)

- 6.5 Heavy commercial vehicle (HCV)

Chapter 7 Market estimates and forecast, by Propulsion Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Electric vehicles (EVs)

- 7.3 Internal combustion engine (ICE) vehicles

Chapter 8 Market estimates and forecast, by Application, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Interior sensing

- 8.3 Exterior sensing

Chapter 9 Market estimates and forecast, by region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Uk

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company profiles

- 10.1 AMS-OSRAM AG

- 10.2 Analog Devices, Inc.

- 10.3 Aptiv PLC

- 10.4 Autoliv Inc.

- 10.5 Broadcom Inc.

- 10.6 Continental AG

- 10.7 Denso Corporation

- 10.8 Hamamatsu Photonics K.K.

- 10.9 Infineon Technologies AG

- 10.10 LeddarTech Inc.

- 10.11 Melexis NV

- 10.12 Microchip Technology Inc.

- 10.13 NVIDIA Corporation

- 10.14 NXP Semiconductors N.V.

- 10.15 ON Semiconductor Corporation

- 10.16 Omnivision Technologies, Inc.

- 10.17 Panasonic Corporation

- 10.18 Robert Bosch GmbH

- 10.19 STMicroelectronics N.V.

- 10.20 Texas Instruments Incorporated

全球汽車串列資料轉換晶片市場佔有率及排名、總收入及需求預測(2026-2032)

全球汽車串列資料轉換晶片市場佔有率及排名、總收入及需求預測(2026-2032) 2026年全球汽車積體電路(IC)市場報告

2026年全球汽車積體電路(IC)市場報告 新能源汽車感測器晶片市場按感測器類型、車輛類型、駕駛自動化程度、應用和分銷管道分類,全球預測(2026-2032年)汽車振盪器市場按類型、頻率範圍、安裝方式、輸出類型、應用和最終用戶分類,全球預測,2026-2032年汽車晶片電感器市場按產品類型、電感範圍、安裝技術和應用分類-2026-2032年全球預測汽車通用快閃記憶體市場按技術世代、儲存容量、應用、車輛類型、驅動方式和分銷管道分類-2026-2032年全球預測車用級FRD晶片市場:依晶片材料、車輛類型、電壓等級、通路及應用分類-2026-2032年全球預測

新能源汽車感測器晶片市場按感測器類型、車輛類型、駕駛自動化程度、應用和分銷管道分類,全球預測(2026-2032年)汽車振盪器市場按類型、頻率範圍、安裝方式、輸出類型、應用和最終用戶分類,全球預測,2026-2032年汽車晶片電感器市場按產品類型、電感範圍、安裝技術和應用分類-2026-2032年全球預測汽車通用快閃記憶體市場按技術世代、儲存容量、應用、車輛類型、驅動方式和分銷管道分類-2026-2032年全球預測車用級FRD晶片市場:依晶片材料、車輛類型、電壓等級、通路及應用分類-2026-2032年全球預測 汽車晶片市場規模、佔有率和成長分析(按類型、車輛類型、應用和地區分類)-2026-2033年產業預測2025年全球汽車光學鍵結生產線市場報告

汽車晶片市場規模、佔有率和成長分析(按類型、車輛類型、應用和地區分類)-2026-2033年產業預測2025年全球汽車光學鍵結生產線市場報告 自旋電子元件在汽車應用領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

自旋電子元件在汽車應用領域的市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)