|

市場調查報告書

商品編碼

1797796

護膚成分市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Skincare Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

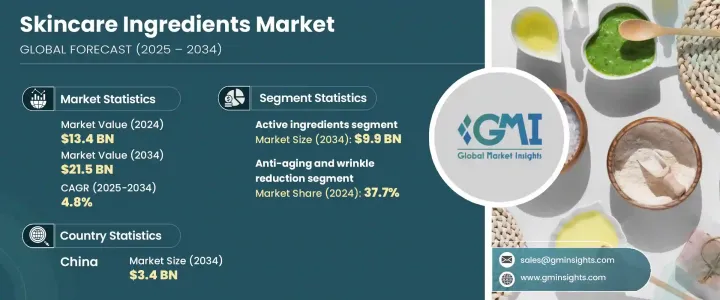

2024年,全球護膚成分市場規模達134億美元,預計2034年將以4.8%的複合年成長率成長,達到215億美元。這一成長主要源於人們對皮膚健康的日益關注、消費者意識的提升,以及已開發市場和新興市場對更天然、清潔標籤護膚配方的日益偏好。對滿足個人化護膚需求的高階多功能產品的需求,也推動了這一成長。此外,強調成分透明度的清潔美容運動,也持續影響產品開發。

如今,超過60%的新產品都帶有「無添加」或極簡成分等宣稱,這使得成分透明度成為市場成長的重要驅動力。數位化消費者的崛起也意味著消費者對化妝品成分的關注度不斷提升,越來越重視安全且經臨床驗證的配方。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 134億美元 |

| 預測值 | 215億美元 |

| 複合年成長率 | 4.8% |

此外,韓妝和日妝潮流的影響力日益增強,引發了護膚成分的創新浪潮,兩者均強調使用獨特、尖端的活性成分。這些趨勢促進了強效成分的開發和應用,這些成分通常源自天然,並得到先進科學研究的支持,吸引了全球消費者的注意。這種將創新活性成分融入產品的趨勢不僅影響配方趨勢,也促使品牌更加重視所用成分的功效和永續性。因此,各大品牌正在加大研發投入,以提供符合不同消費族群特定護膚需求的創新解決方案。

2024年,活性成分細分市場產值達到62億美元,預計2034年將以4.8%的複合年成長率成長。活性成分是護膚配方的基石,在皮膚健康、外觀和抗衰老方面帶來顯著的益處。抗氧化劑和維生素(如維生素C、E和阿魏酸)等關鍵成分備受追捧,尤其因為它們具有潛在的保護和煥活功效。穩定化和封裝技術的進步推動了對這些成分的需求。這促使人們投入大量研發精力,以增強其功效並抵禦污染等環境壓力,這也激發了人們對抗老化配方的新興趣。

2024年,抗老和祛皺產品佔了37.7%的市場。受對抗衰老跡象產品需求不斷成長的推動,該領域已成為行業中最大的類別。精華液約佔抗老產品銷售的42%,因其高濃度的活性成分而特別受歡迎。隨著消費者對污染和紫外線對皮膚健康影響的認知不斷加深,對保護性和修復性配方的需求也日益成長。含有抗氧化劑和胜肽的產品尤其受歡迎,這些成分能夠有效抵抗環境損害,並促進肌膚年輕亮澤。

2024年,中國護膚成分市場規模達21億美元,預計複合年成長率為5%。 「中國美妝」趨勢的成長,以及對本土傳統中藥成分的重視,正在推動這一成長。人參和珍珠粉等天然成分的使用日益普及,尤其是在尋求地道、符合當地文化的護膚產品的消費者中。此外,在CSAR規則等不斷發展的監管框架的推動下,對永續性和成分透明度的日益重視,刺激了對綠色化學和生物技術的投資。小紅書和直播等電商平台目前約佔美妝銷售額的10%,它們也加速採用創新成分,進而進一步促進市場的成長和認知度。

護膚成分市場的領先公司包括德之馨股份有限公司 (Symrise AG)、亞什蘭公司 (Ashland Inc.)、贏創工業股份有限公司 (Evonik Industries AG)、巴斯夫股份有限公司 (BASF SE) 和禾大國際 (Croda International)。這些公司持續推動創新,始終走在市場趨勢的前沿,專注於成分開發、永續性和以客戶為中心的解決方案,以保持競爭優勢。為了鞏固其在護膚成分市場的地位,各公司正專注於創新、永續性和以消費者為中心的產品開發。關鍵策略包括開發天然、清潔標籤成分,以滿足市場對環保安全產品日益成長的需求。許多公司正在大力投資研發新型活性成分,以解決老化、色素沉澱和環境壓力等特定皮膚問題。與化妝品品牌建立策略合作夥伴關係以及在亞洲等新興市場不斷擴張也是擴大其市場影響力的關鍵。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 活性成分

- 抗衰老劑

- 類視黃醇及其衍生物

- 胜肽和蛋白質

- α-羥基酸(AHAS)

- BETA-羥基酸(BHAS)

- 保濕劑

- 玻尿酸

- 神經醯胺

- 甘油和保濕劑

- 紫外線防護劑

- 化學紫外線過濾器

- 物理紫外線過濾器

- 亮膚劑

- 維生素C及其衍生物

- 菸鹼醯胺

- 麴酸

- 痤瘡治療劑

- 抗衰老劑

- 功能性成分

- 乳化劑

- 界面活性劑

- 增稠劑和流變改質劑

- 潤膚劑

- 調理劑

- 防腐劑

- 傳統防腐劑

- 對羥基苯甲酸酯

- 苯氧乙醇

- 天然防腐劑

- 多功能防腐劑

- 傳統防腐劑

- 特殊食材

- 植物萃取物

- 海洋衍生成分

- 生物技術衍生成分

- 益生菌和益生元

第6章:市場估計與預測:按來源,2021 - 2034 年

- 主要趨勢

- 天然和有機成分

- 植物萃取物

- 海洋衍生成分

- 礦物質成分

- 經過認證的有機成分

- 合成成分

- 實驗室合成的化合物

- 與天然成分相同的成分

- 石化衍生成分

- 生物技術衍生成分

- 發酵衍生成分

- 細胞培養衍生成分

- 酵素生產的成分

- 升級再造和再利用的原料

- 農業廢棄物衍生

- 食品工業副產品

- 海洋廢棄物利用

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 抗老化和減少皺紋

- 乳霜和精華液

- 眼部護理產品

- 頸部和胸部產品

- 保濕補水

- 日常保濕霜

- 強效補水護理

- 隔夜修復產品

- 防曬

- 日常防曬產品

- 高防護防曬霜

- 曬後護理

- 痤瘡和瑕疵治療

- 局部治療

- 日常痤瘡護理

- 痤瘡後修復

- 亮膚和色素沉著

- 暗斑修正液

- 整體亮白產品

- 黃褐斑治療

- 敏感肌膚保養

- 溫和清潔

- 屏障修復

- 減少發紅

- 專業應用

- 藥妝品

- 男士護膚

- 嬰兒和兒童產品

第8章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 直銷

- 製造商直接向品牌

- 技術銷售團隊

- 大客戶管理

- 分銷商和批發商

- 區域經銷商

- 特用化學品分銷商

- 多線經銷商

- 線上B2B平台

- 專業原料市場

- 化學品交易平台

- 直接製造商門戶

- 貿易展覽會

- 化妝品行業活動

- 區域貿易展覽會

- 虛擬展覽平台

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- BASF SE

- Croda International Plc

- Dow Inc.

- DSM-Firmenich

- Estee Lauder Companies Inc.

- Evonik Industries AG

- Givaudan SA

- Henkel AG & Co. KGaA

- Lonza Group AG

- L'Oreal SA

- Procter & Gamble Company

- Shiseido Company Limited

- Solvay SA

- Symrise AG

- Unilever PLC

The Global Skincare Ingredients Market was valued at USD 13.4 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 21.5 billion by 2034. This expansion is driven by an increasing focus on skin health, rising consumer awareness, and the growing preference for more natural, clean-label skincare formulations in both developed and emerging markets. The demand for premium, multi-functional products that cater to personalized skincare needs is fueling this growth. Additionally, the clean beauty movement, with an emphasis on ingredient transparency, continues to shape product development.

Over 60% of new product launches now feature claims such as "free-from" or minimalist ingredients, making ingredient transparency a significant driver of market growth. The rise in digital-savvy consumers also means more attention is given to cosmetic ingredients, with a growing emphasis on safe, clinically backed formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.4 Billion |

| Forecast Value | $21.5 Billion |

| CAGR | 4.8% |

Furthermore, the growing influence of K-beauty and J-beauty trends has sparked a wave of innovation in skincare ingredients, with both movements emphasizing the use of unique, cutting-edge actives. These trends have encouraged the development and adoption of potent ingredients, often derived from nature and supported by advanced scientific research, which have captured the attention of consumers globally. This shift towards incorporating innovative actives into products is not only influencing formulation trends but also pushing brands to focus on the efficacy and sustainability of the ingredients used. As a result, brands are investing more in research and development to bring forward novel solutions that align with the specific skincare needs of diverse consumer groups.

The active ingredients segment generated USD 6.2 billion in 2024 and is projected to grow at a CAGR of 4.8% through 2034. Active ingredients are the cornerstone of skincare formulations, providing measurable benefits in terms of skin health, appearance, and anti-aging effects. Key ingredients like antioxidants and vitamins (such as Vitamin C, E, and ferulic acid) have become highly sought-after, especially due to their potential protective and rejuvenating properties. The demand for these ingredients is supported by advances in stabilization and encapsulation technologies. This has led to significant research and development efforts to enhance their efficacy and protect against environmental stressors such as pollution, which has also sparked new interest in anti-aging formulations.

In 2024, the anti-aging and wrinkle reduction segment held a 37.7% share. This segment has become the largest category in the industry, driven by the rising demand for products that combat the visible signs of aging. Serums, which make up around 42% of the volume in the anti-aging segment, are particularly popular due to their high concentrations of active ingredients. As consumer awareness of the effects of pollution and UV rays on skin health continues to grow, the demand for protective and reparative formulations is increasing. Products containing antioxidants and peptides are particularly in demand, with these ingredients offering protective benefits against environmental damage and promoting youthful, radiant skin.

China Skincare Ingredients Market was valued at USD 2.1 billion in 2024 and is projected to grow at a CAGR of 5%. The growth of the "C-Beauty" trend, with a focus on indigenous, Traditional Chinese Medicine (TCM)-inspired ingredients, is driving this expansion. The use of naturally sourced ingredients like ginseng and pearl powder is gaining popularity, particularly among consumers seeking authentic, culturally relevant skincare options. Additionally, the increasing emphasis on sustainability and ingredient transparency, driven by evolving regulatory frameworks such as the CSAR rules, has spurred investment in green chemistry and biotech. E-commerce platforms, such as Xiaohongshu and livestreaming, which now account for approximately 10% of beauty sales, are also accelerating the adoption of innovative ingredients, thereby further boosting the market's growth and awareness.

The leading companies in the skincare ingredients market include Symrise AG, Ashland Inc., Evonik Industries AG, BASF SE, and Croda International. These players continue to drive innovation and remain at the forefront of market trends, focusing on ingredient development, sustainability, and customer-centric solutions to maintain their competitive positions. To strengthen their presence in the skincare ingredients market, companies are focusing on innovation, sustainability, and consumer-centric product development. Key strategies include the development of natural, clean-label ingredients that align with the growing demand for environmentally responsible and safe products. Many firms are investing heavily in research and development to create new actives that address specific skin concerns like aging, pigmentation, and environmental stress. Strategic partnerships with cosmetic brands and a growing presence in emerging markets such as Asia are also key to expanding their market footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Active ingredients

- 5.2.1 Anti-aging agents

- 5.2.1.1 Retinoids and derivatives

- 5.2.1.2 Peptides and proteins

- 5.2.1.3 Alpha hydroxy acids (AHAS)

- 5.2.1.4 Beta hydroxy acids (BHAS)

- 5.2.2 Moisturizing agents

- 5.2.2.1 Hyaluronic acid

- 5.2.2.2 Ceramides

- 5.2.2.3 Glycerin and humectants

- 5.2.3 UV protection agents

- 5.2.3.1 Chemical UV filters

- 5.2.3.2 Physical UV filters

- 5.2.4 Skin brightening agents

- 5.2.4.1 Vitamin C and derivatives

- 5.2.4.2 Niacinamide

- 5.2.4.3 Kojic acid

- 5.2.5 Acne treatment agents

- 5.2.1 Anti-aging agents

- 5.3 Functional ingredients

- 5.3.1 Emulsifiers

- 5.3.2 Surfactants

- 5.3.3 Thickeners and rheology modifiers

- 5.3.4 Emollients

- 5.3.5 Conditioning agents

- 5.4 Preservatives

- 5.4.1 Traditional preservatives

- 5.4.1.1 Parabens

- 5.4.1.2 Phenoxyethanol

- 5.4.2 Natural preservatives

- 5.4.3 Multifunctional preservatives

- 5.4.1 Traditional preservatives

- 5.5 Specialty ingredients

- 5.5.1 Botanical extracts

- 5.5.2 Marine-derived ingredients

- 5.5.3 Biotechnology-derived ingredients

- 5.5.4 Probiotics and prebiotics

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Natural and organic ingredients

- 6.2.1 Plant-based extracts

- 6.2.2 Marine-derived ingredients

- 6.2.3 Mineral-based ingredients

- 6.2.4 Certified organic ingredients

- 6.3 Synthetic ingredients

- 6.3.1 Laboratory-synthesized compounds

- 6.3.2 Nature-identical ingredients

- 6.3.3 Petrochemical-derived ingredients

- 6.4 Biotechnology-derived ingredients

- 6.4.1 Fermentation-derived ingredients

- 6.4.2 Cell culture-derived ingredients

- 6.4.3 Enzymatically-produced ingredients

- 6.5 Upcycled and circular ingredients

- 6.5.1 Agricultural waste-derived

- 6.5.2 Food industry by-products

- 6.5.3 Marine waste utilization

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.1.1 Anti-aging and wrinkle reduction

- 7.1.2 Face creams and serums

- 7.1.3 Eye care products

- 7.1.4 Neck and decolletage products

- 7.2 Moisturizing and hydration

- 7.2.1 Daily moisturizers

- 7.2.2 Intensive hydration treatments

- 7.2.3 Overnight repair products

- 7.3 Sun protection

- 7.3.1 Daily SPF products

- 7.3.2 High protection sunscreens

- 7.3.3 After-sun care

- 7.4 Acne and blemish treatment

- 7.4.1 Spot treatments

- 7.4.2 Daily acne care

- 7.4.3 Post-acne repair

- 7.5 Skin brightening and pigmentation

- 7.5.1 Dark spot correctors

- 7.5.2 Overall brightening products

- 7.5.3 Melasma treatment

- 7.6 Sensitive skin care

- 7.6.1 Gentle cleansing

- 7.6.2 Barrier repair

- 7.6.3 Redness reduction

- 7.7 Specialty applications

- 7.7.1 Dermocosmetics

- 7.7.2 Men's skincare

- 7.7.3 Baby and children's products

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.2.1 Manufacturer to brand direct

- 8.2.2 Technical sales teams

- 8.2.3 Key account management

- 8.3 Distributors and wholesalers

- 8.3.1 Regional distributors

- 8.3.2 Specialty chemical distributors

- 8.3.3 Multi-line distributors

- 8.4 Online B2B platforms

- 8.4.1 Specialized ingredient marketplaces

- 8.4.2 Chemical trading platforms

- 8.4.3 Direct manufacturer portals

- 8.5 Trade shows and exhibitions

- 8.5.1 In-cosmetics events

- 8.5.2 Regional trade shows

- 8.5.3 Virtual exhibition platforms

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Croda International Plc

- 10.3 Dow Inc.

- 10.4 DSM-Firmenich

- 10.5 Estee Lauder Companies Inc.

- 10.6 Evonik Industries AG

- 10.7 Givaudan SA

- 10.8 Henkel AG & Co. KGaA

- 10.9 Lonza Group AG

- 10.10 L'Oreal S.A.

- 10.11 Procter & Gamble Company

- 10.12 Shiseido Company Limited

- 10.13 Solvay SA

- 10.14 Symrise AG

- 10.15 Unilever PLC

潔面霜市場:依產品形態、膚質、年齡層、性別、價格範圍、應用領域、包裝類型、成分類型和分銷管道分類-全球預測,2026-2032年

潔面霜市場:依產品形態、膚質、年齡層、性別、價格範圍、應用領域、包裝類型、成分類型和分銷管道分類-全球預測,2026-2032年 2026-2030年全球青少年個人護理產品市場

2026-2030年全球青少年個人護理產品市場 基於微生物組的護膚療法市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、形式、材料類型和安裝類型分類護膚品市場分析及預測(至2035年):類型、產品類型、技術、應用、劑型、材料類型、最終用戶、功能、解決方案護膚市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、劑型、最終用戶、功能、材料類型及解決方案分類

基於微生物組的護膚療法市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、形式、材料類型和安裝類型分類護膚品市場分析及預測(至2035年):類型、產品類型、技術、應用、劑型、材料類型、最終用戶、功能、解決方案護膚市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、劑型、最終用戶、功能、材料類型及解決方案分類 眼霜市場機會、成長要素、產業趨勢分析及2026年至2035年預測。

眼霜市場機會、成長要素、產業趨勢分析及2026年至2035年預測。 全球營養美容品市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球爽膚水市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球護膚油市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球護膚美容保養精華液市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球營養美容品市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球爽膚水市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球護膚油市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球護膚美容保養精華液市場規模、佔有率、趨勢及成長分析報告(2026-2034)