|

市場調查報告書

商品編碼

1797722

低溫超導材料市場機會、成長動力、產業趨勢分析及2025-2034年預測Cryogenic Superconductor Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

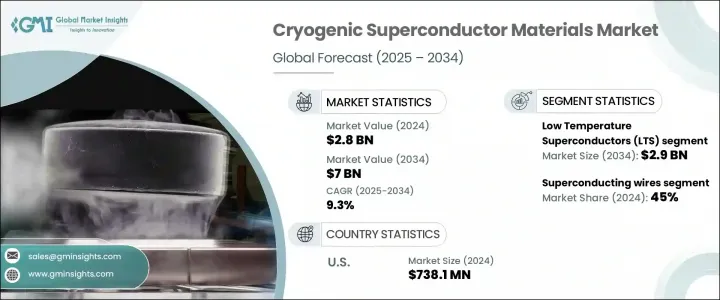

2024年,全球低溫超導材料市場規模達28億美元,預計2034年將以9.3%的複合年成長率成長,達到70億美元。隨著關鍵產業擴大採用先進技術,全球對低溫超導材料的需求日益成長。這些材料能夠在極低溫下實現零電阻導電,正成為從清潔能源到高精度醫學成像等各個領域的關鍵組件。其獨特的電氣特性協助打造節能基礎設施,並日益被視為支持下一代電力系統和科學創新的關鍵。全球範圍內的節能目標持續推動超導材料的應用,使其成為永續發展努力的一部分。

超導體能夠無損耗地傳輸電力,使其成為升級現代電網的重要解決方案,尤其是在再生能源佔比不斷擴大的背景下。整合超導電纜的基礎設施建設有助於穩定和增強電力傳輸,提供優於傳統方法的性能。同時,醫療保健和科研行業仍然是這些材料的強勁終端用戶。核磁共振掃描儀等醫療技術依靠超冷超導磁鐵產生強大而穩定的磁場,以實現精確的內部成像。隨著技術進步和醫療保健需求的不斷成長,超導磁鐵的用途也在不斷擴大。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 28億美元 |

| 預測值 | 70億美元 |

| 複合年成長率 | 9.3% |

低溫超導體 (LTS) 領域在 2024 年創造了 11 億美元的市場規模,預計到 2034 年將達到 29 億美元。這些超導體主要由鈮鈦 (NbTi) 和鈮錫 (Nb3Sn) 等化合物組成,在低於 20 開爾文(約 -253°C)的溫度下表現最佳。其主導地位源於其技術成熟度、穩定性以及數十年的發展,這些發展帶來了精良且經濟高效的製造流程。 LTS 材料憑藉其久經考驗的性能,尤其是在能夠可靠地維持穩定低溫環境的應用中,仍然是許多商用系統的實用首選。

超導導線市場在2024年佔了45%的市佔率。這些導線因其能夠無阻力傳輸電流而備受推崇,這意味著零能量損耗和無與倫比的運作效率。它們能夠處理更高的電流密度,從而能夠建立具有更高磁場強度的緊湊系統,這對於醫學、能源和研究領域的先進技術至關重要。超導導線緊湊的體積和性能優勢持續吸引那些尋求提高電源效率和系統可靠性的行業的需求。

2024年,美國低溫超導材料市場規模達7.381億美元,預計2034年將以9.1%的複合年成長率成長。受醫療保健、電力基礎設施和高科技產業對超導技術的廣泛應用所推動,美國仍處於該領域的領先地位。 MRI系統是美國此類材料的主要應用領域,隨著診斷影像技術的不斷發展,對下一代超導材料的需求也不斷成長。這些系統利用高度穩定的磁場,這得益於冷卻至低溫的超導線圈。隨著醫療保健服務的擴展以及舊系統的升級和更換,對這些專用材料的需求持續強勁。

全球低溫超導材料市場的領導公司包括 Cryomagnetics、Hyper Tech Research、SAMRI Advanced Material、American Superconductor Corporation、Western Superconducting Technologies、Bruker Energy & Supercon Technologies、THEVA Dunnschichttechnik、Sam Dong、SuperPower 和住友電氣工業。低溫超導材料領域的公司正在大力投資先進研發,以提高材料性能、降低生產成本並提高可擴展性。許多公司正專注於與大學和研究機構合作,以加速下一代超導合金的開發。另一個關鍵策略是擴大製造能力並整合垂直營運,以更好地控制供應鏈。公司還優先考慮客製化,為 MRI 系統、電力傳輸和量子計算提供特定應用的超導體。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場規模及預測:依材料類型,2021-2034

- 主要趨勢

- 低溫超導體(LTS)

- 鈮鈦(NbTi)合金

- 鈮錫(Nb3Sn)化合物

- 二硼化鎂(MgB2)

- 高溫超導體(HTS)

- YBCO(YBa2Cu3O7)材料

- BSCCO(Bi2Sr2Ca2Cu3O10)材料

- 鐵基超導體

- 其他 HTS 材料(TBCCO、汞基)

- 新興超導材料

- 拓樸超導體

- 有機超導體

- 室溫超導體

- 混合和複合材料

第6章:市場規模及預測:依產品形式,2021-2034

- 主要趨勢

- 超導導線

- 圓線產品

- 多絲線結構

- 交流損耗特性及應用

- 扁平線材及帶材產品

- 塗層導體技術

- 高電流密度應用

- 絞合導體和成纜導體

- 大電流應用

- 融合磁鐵和電源線的使用

- 圓線產品

- 塊體超導材料

- 單晶塊體材料

- 俘獲場磁鐵應用

- 磁浮系統

- 多晶塊體材料

- 經濟高效的批量應用

- 磁屏蔽和軸承

- 紋理和取向材料

- 增強的性能特徵

- 專業高場應用

- 單晶塊體材料

- 薄膜超導體

- 外延薄膜

- 電子和感測器應用

- 量子裝置整合

- 多層和異質結構薄膜

- 高階量子運算應用

- 約瑟夫森結技術

- 外延薄膜

- 超導粉末和前驅體

- 原料粉末

- 前驅化學物質和化合物

- 特種加工材料

第7章:市場規模及預測:依最終用途,2021-2034

- 主要趨勢

- 醫療保健應用

- 磁振造影(MRI)系統

- 核磁共振(NMR)光譜

- 超高場 NMR 系統(>1 Ghz)

- 研究和藥物應用

- 粒子治療與醫療加速器

- 質子和離子治療系統

- 緊湊型加速器開發

- 能源和電力應用

- 輸配電

- 超導電力電纜

- 故障電流限制器

- 電力變壓器和變電站

- 儲能系統

- 超導磁能儲存(SMES)

- 電網穩定和電能質量

- 再生能源整合

- 發電機和電動機

- 風力發電機

- 船舶推進電機

- 工業馬達應用

- 輸配電

- 聚變能與研究

- 磁約束聚變反應器

- Iter計畫和國際合作

- 私人核融合公司舉措

- 環形和極向場線圈

- 高能物理研究

- 粒子加速器與對撞機

- 大型強子對撞機(LHC)應用

- 未來的加速器項目

- 磁約束聚變反應器

- 量子計算與電子學

- 量子計算系統

- 超導量子位元技術

- 量子處理器開發

- 低溫量子運算基礎設施

- 超導電子學

- 單光子偵測器(SSPDS)

- 魷魚感測器和磁力儀

- 約瑟夫森結裝置

- 量子感測器和計量學

- 超靈敏磁場檢測

- 重力波探測

- 量子計算系統

- 交通運輸應用

- 磁浮系統

- 高鐵運輸

- 城市交通應用

- 電動航空

- 飛機推進電機

- 輕量級電力系統

- 磁浮系統

- 工業和科學應用

- 材料加工與製造

- 磁分離系統

- 科學研究儀器

第8章:市場規模及預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- American Superconductor Corporation

- SuperPower

- Sumitomo Electric Industries

- Bruker Energy & Supercon Technologies

- Hyper Tech Research

- THEVA Dunnschichttechnik

- Western Superconducting Technologies

- SAMRI Advanced Material

- Sam Dong

- Cryomagnetics

The Global Cryogenic Superconductor Materials Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 7 billion by 2034. As critical industries increasingly adopt advanced technologies, demand for cryogenic superconductors is gaining traction across the globe. These materials, capable of conducting electricity with zero resistance at extremely low temperatures, are becoming essential components in sectors ranging from clean energy to high-precision medical imaging. Their unique electrical properties enable energy-efficient infrastructure and are increasingly being viewed as key to supporting next-generation power systems and scientific innovation. Energy efficiency goals worldwide continue to push the adoption of superconducting materials as part of larger sustainability efforts.

Superconductors can transmit electricity without energy loss, making them a vital solution for upgrading modern grids-especially as the share of renewable energy expands. Infrastructure development that integrates superconducting cables can help stabilize and enhance power transmission, offering superior performance over conventional methods. Meanwhile, the healthcare and scientific research industries remain strong end-users of these materials. Medical technologies such as MRI scanners depend on supercooled superconducting magnets to generate powerful, steady magnetic fields for precise internal imaging. Their usage is expanding in line with technological advancement and rising healthcare needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $7 Billion |

| CAGR | 9.3% |

The low temperature superconductors (LTS) segment generated USD 1.1 billion in 2024 and is expected to reach USD 2.9 billion by 2034. These superconductors, primarily composed of compounds such as niobium-titanium (NbTi) and niobium-tin (Nb3Sn), function optimally at temperatures under 20 Kelvin (around -253°C). Their dominance is due to technological maturity, stability, and decades of development that have led to refined, cost-effective manufacturing processes. LTS materials remain a practical and preferred choice for many commercial systems because of their proven performance, especially in applications where stable, low-temperature environments can be reliably maintained.

The superconducting wires segment held a 45% share in 2024. These wires are valued for their ability to transmit electric current without resistance, translating to zero energy loss and unmatched operational efficiency. Their capability to handle higher current densities also allows for compact systems with greater magnetic field strengths-essential for advanced technologies in medicine, energy, and research. Their compact footprint and performance advantages continue to attract demand from industries seeking to improve power efficiency and system reliability.

United States Cryogenic Superconductor Materials Market was valued at USD 738.1 million in 2024 and is expected to grow at a CAGR of 9.1% through 2034. The United States remains at the forefront of this sector, driven by adoption of superconducting technologies in healthcare, power infrastructure, and high-tech industries. MRI systems are the primary application for these materials in the US, and as diagnostic imaging technology continues to evolve, so does the need for next-generation superconducting materials. These systems utilize highly stable magnetic fields, made possible by superconducting coils cooled to cryogenic temperatures. As healthcare services expand, along with upgrades and replacements of older systems, the demand for these specialized materials remains consistently strong.

Leading companies operating in the Global Cryogenic Superconductor Materials Market include Cryomagnetics, Hyper Tech Research, SAMRI Advanced Material, American Superconductor Corporation, Western Superconducting Technologies, Bruker Energy & Supercon Technologies, THEVA Dunnschichttechnik, Sam Dong, SuperPower, and Sumitomo Electric Industries Companies in the cryogenic superconductor materials space are investing heavily in advanced R&D to enhance material performance, reduce production costs, and increase scalability. Many are focusing on partnerships with universities and research institutions to accelerate the development of next-generation superconducting alloys. Another key strategy is expanding their manufacturing capabilities and integrating vertical operations for better supply chain control. Firms are also prioritizing customization, offering application-specific superconductors for MRI systems, power transmission, and quantum computing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Low temperature superconductors (LTS)

- 5.2.1 Niobium-Titanium (NbTi) alloys

- 5.2.2 Niobium-Tin (Nb3Sn) compounds

- 5.2.3 Magnesium diboride (MgB2)

- 5.3 High temperature superconductors (HTS)

- 5.3.1 YBCO (YBa2Cu3O7) materials

- 5.3.2 BSCCO (Bi2Sr2Ca2Cu3O10) materials

- 5.3.3 Iron-based superconductors

- 5.3.4 Other HTS materials (TBCCO, Hg-based)

- 5.4 Emerging superconductor materials

- 5.4.1 Topological superconductors

- 5.4.2 Organic superconductors

- 5.4.3 Room temperature superconductor

- 5.4.4 Hybrid and composite materials

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Superconducting wires

- 6.2.1 Round wire products

- 6.2.1.1 Multifilamentary wire construction

- 6.2.1.2 AC loss characteristics and applications

- 6.2.2 Flat wire and tape products

- 6.2.2.1 Coated conductor technology

- 6.2.2.2 High current density applications

- 6.2.3 Stranded and cabled conductors

- 6.2.3.1 High current applications

- 6.2.3.2 Fusion magnet and power cable use

- 6.2.1 Round wire products

- 6.3 Bulk superconductor materials

- 6.3.1 Single crystal bulk materials

- 6.3.1.1 Trapped field magnet applications

- 6.3.1.2 Magnetic levitation systems

- 6.3.2 Polycrystalline bulk materials

- 6.3.2.1 Cost-effective bulk applications

- 6.3.2.2 Magnetic shielding and bearings

- 6.3.3 Textured and oriented materials

- 6.3.3.1 Enhanced performance characteristics

- 6.3.3.2 Specialized high-field applications

- 6.3.1 Single crystal bulk materials

- 6.4 Thin film superconductors

- 6.4.1 Epitaxial thin films

- 6.4.1.1 Electronic and sensor applications

- 6.4.1.2 Quantum device integration

- 6.4.2 Multilayer and heterostructure films

- 6.4.2.1 Advanced quantum computing applications

- 6.4.2.2 Josephson junction technology

- 6.4.1 Epitaxial thin films

- 6.5 Superconducting powders and precursors

- 6.5.1 Raw material powders

- 6.5.2 Precursor chemicals and compounds

- 6.5.3 Specialty processing materials

Chapter 7 Market Size and Forecast, By End Use, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Medical and healthcare applications

- 7.2.1 Magnetic resonance imaging (MRI) systems

- 7.2.2 Nuclear magnetic resonance (NMR) spectroscopy

- 7.2.2.1 Ultra-high field NMR systems (>1 Ghz)

- 7.2.2.2 Research and pharmaceutical applications

- 7.2.3 Particle therapy and medical accelerators

- 7.2.3.1 Proton and ion therapy systems

- 7.2.3.2 Compact accelerator development

- 7.3 Energy and power applications

- 7.3.1 Power transmission and distribution

- 7.3.1.1 Superconducting power cables

- 7.3.1.2 Fault current limiters

- 7.3.1.3 Power transformers and substations

- 7.3.2 Energy storage systems

- 7.3.2.1 Superconducting magnetic energy storage (SMES)

- 7.3.2.2 Grid stabilization and power quality

- 7.3.2.3 Renewable energy integration

- 7.3.3 Electric generators and motors

- 7.3.3.1 Wind turbine generators

- 7.3.3.2 Ship propulsion motors

- 7.3.3.3 Industrial motor applications

- 7.3.1 Power transmission and distribution

- 7.4 Fusion energy and research

- 7.4.1 Magnetic confinement fusion reactors

- 7.4.1.1 Iter project and international collaboration

- 7.4.1.2 Private fusion company initiatives

- 7.4.1.3 Toroidal and poloidal field coils

- 7.4.2 High energy physics research

- 7.4.2.1 Particle accelerators and colliders

- 7.4.2.2 Large hadron collider (LHC) applications

- 7.4.2.3 Future accelerator projects

- 7.4.1 Magnetic confinement fusion reactors

- 7.5 Quantum computing and electronics

- 7.5.1 Quantum computing systems

- 7.5.1.1 Superconducting qubit technology

- 7.5.1.2 Quantum processor development

- 7.5.1.3 Cryogenic quantum computing infrastructure

- 7.5.2 Superconducting electronics

- 7.5.2.1 Single photon detectors (SSPDS)

- 7.5.2.2 Squid sensors and magnetometers

- 7.5.2.3 Josephson junction devices

- 7.5.3 Quantum sensors and metrology

- 7.5.3.1 Ultra-sensitive magnetic field detection

- 7.5.3.2 Gravitational wave detection

- 7.5.1 Quantum computing systems

- 7.6 Transportation applications

- 7.6.1 Magnetic levitation (Maglev) systems

- 7.6.1.1 High-speed rail transportation

- 7.6.1.2 Urban transit applications

- 7.6.2 Electric aviation

- 7.6.2.1 Aircraft propulsion motors

- 7.6.2.2 Lightweight power systems

- 7.6.1 Magnetic levitation (Maglev) systems

- 7.7 Industrial and scientific applications

- 7.7.1 Materials processing and manufacturing

- 7.7.2 Magnetic separation systems

- 7.7.3 Scientific research instruments

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Superconductor Corporation

- 9.2 SuperPower

- 9.3 Sumitomo Electric Industries

- 9.4 Bruker Energy & Supercon Technologies

- 9.5 Hyper Tech Research

- 9.6 THEVA Dunnschichttechnik

- 9.7 Western Superconducting Technologies

- 9.8 SAMRI Advanced Material

- 9.9 Sam Dong

- 9.10 Cryomagnetics