|

市場調查報告書

商品編碼

1797717

溶小體貯積症治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lysosomal Storage Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

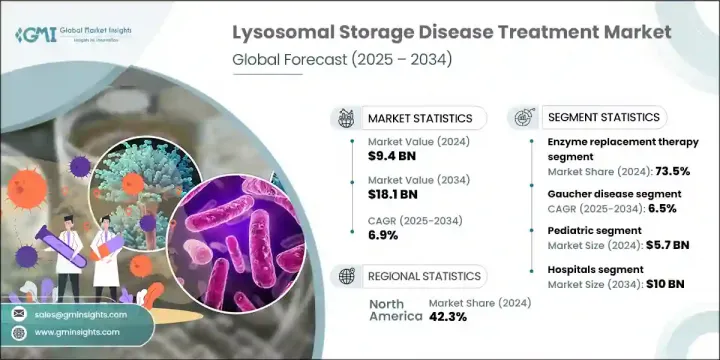

2024年,全球溶小體貯積症治療市場規模達94億美元,預計2034年將以6.9%的複合年成長率成長,達到181億美元。法布瑞氏症、戈謝氏症和龐貝氏症等罕見遺傳疾病的發生率不斷上升,是市場成長的重要驅動力。酵素替代療法和基因療法的進展,加上授予孤兒藥資格的監管框架,正在加速這些疾病的治療發展。目前的治療領域包括酵素替代療法、小分子藥物和基於基因的干涉措施,所有這些措施都旨在改善患者的生活品質和臨床療效。

賽諾菲、Amicus Therapeutics、BioMarin、武田製藥和Orchard Therapeutics等領先公司正積極參與全球分銷擴張和新型治療模式的創新。新生兒篩檢計畫的擴大和更廣泛的認知計劃正在促進早期診斷和干涉,這對於獲得最佳治療效果和長期預後至關重要。早期檢測的增加正在刺激對診斷和治療的需求,重塑市場動態並推動產品線成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 94億美元 |

| 預測值 | 181億美元 |

| 複合年成長率 | 6.9% |

2024年,酵素替代療法市場佔有73.5%的佔有率。此療法的普及得益於診斷程序的改進和疾病認知的提高,其應用範圍也隨之擴大。這些療法在治療酵素缺乏性溶小體疾病方面療效顯著,顯著改善了患者的病情,促使製藥公司透過合作和內部開發等方式投資擴展和增強這些療法。

2024年,黏多醣症治療領域佔27.4%的市場。監管激勵措施支持黏多醣症治療市場的擴張,包括加速核准途徑和孤兒藥條款提供的稅收抵免。製藥和生物技術公司在細胞療法、工程化B細胞療法和基因編輯方法方面的投資正在快速成長,這需要加強實驗室基礎設施、開發檢測方法並大力支持臨床試驗。

2024年,北美溶小體貯積症治療市場佔42.3%的佔有率。美國和加拿大憑藉其對高成本罕見疾病治療的強大保險覆蓋以及LSD研究的大量公共資金,佔據領先地位。美國國立衛生研究院(NIH)和加拿大衛生研究機構等機構為研究提供了大量資助,從而促進了治療創新和未來治療方案的拓展。

活躍於溶小體貯積症治療市場的主要公司包括 Sigilon Therapeutics、輝瑞、Orphazyme、Alexion Pharmaceuticals、Sangamo Therapeutics、JCR Pharmaceuticals、Avrobio、健讚(賽諾菲)、Orchard Therapeutics、武田製藥、BioMarin 和 Amicus Therapeutics。領先的公司正在透過投資基因編輯平台和下一代酵素替代療法等創新療法來鞏固其地位。與學術機構和生物技術公司的策略合作正在拓展其研究能力。各公司也正在建立強大的全球分銷網路以確保市場准入,同時參與有針對性的宣傳和篩選計劃,以提高早期診斷率。透過公私合作夥伴關係和基於註冊的研究,各公司正在加速臨床試驗並加強患者招募。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 新生兒篩檢計畫促進診斷率提高

- 基因和酵素療法的研發管線不斷擴大

- 基於分子和生物標記的診斷進展

- 擴大轉向疾病改良療法和治癒療法

- 產業陷阱與挑戰

- 治療費用高昂

- 在中低收入國家(LMIC)的普及率有限

- 市場機會

- 基因治療和基因組編輯的需求不斷成長

- 專門的罕見疾病治療中心興起

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 定價分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按治療類型,2021 - 2034 年

- 主要趨勢

- 酵素替代療法

- 幹細胞移植

- 底物還原療法

- 其他治療類型

第6章:市場估計與預測:依疾病類型,2021 - 2034 年

- 主要趨勢

- 戈謝氏症

- 黏多醣病

- 龐貝氏症

- 法布瑞氏症

- 其他疾病類型

第7章:市場估計與預測:按年齡層,2021 - 2034 年

- 主要趨勢

- 兒科

- 成人

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 居家照護環境

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Alexion Pharmaceuticals

- Amicus Therapeutics

- Avrobio

- BioMarin

- JCR Pharmaceuticals

- Johnson & Johnson (Actelion Pharmaceuticals)

- Orchard Therapeutics

- Orphazyme

- Pfizer

- Sanofi (Genzyme Corporation)

- Sigilon Therapeutics

- Sangamo therapeutics

- Takeda Pharmaceutical Company (Shire)

The Global Lysosomal Storage Disease Treatment Market was valued at USD 9.4 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 18.1 billion by 2034. The growing incidence of rare genetic disorders such as Fabry, Gaucher, and Pompe disease is a significant driver of market growth. Advances in enzyme replacement therapies and gene therapies-coupled with regulatory frameworks that grant orphan drug designation-are accelerating therapeutic development for these conditions. The treatment landscape now includes enzyme replacement, small molecule drugs, and gene-based interventions, all aimed at improving patient quality of life and clinical outcomes.

Leading companies like Sanofi, Amicus Therapeutics, BioMarin, Takeda Pharmaceutical, and Orchard Therapeutics are actively involved in global distribution expansion and innovation in novel treatment modalities. Expanding newborn-screening programs and broader awareness initiatives are enabling earlier diagnosis and intervention, which is critical for optimal treatment response and long-term prognosis. Increased early detection is boosting demand for both diagnostics and therapeutics, reshaping market dynamics and driving pipeline growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.4 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 6.9% |

The enzyme replacement therapy segment held a 73.5% share in 2024. Its prevalence is due to widespread adoption through enhanced diagnostic programs and better disease awareness. The high efficacy of these treatments in managing enzyme-deficient lysosomal diseases has led to substantial patient improvement, prompting pharmaceutical companies to invest in expanding and enhancing these therapies through collaborations and in-house development.

The mucopolysaccharidoses therapies segment held a 27.4% share in 2024. Market expansion for MPS treatment is supported by regulatory incentives, including expedited approval pathways and tax credits offered under orphan drug provisions. Investment from pharmaceutical and biotech companies in cell therapy, engineered B-cell treatments, and gene editing approaches is growing rapidly, necessitating enhanced laboratory infrastructure, assay development, and extensive clinical trial support.

North America Lysosomal Storage Disease Treatment Market held a 42.3% share in 2024. The U.S. and Canada lead due to robust insurance coverage for high-cost rare disease treatments and substantial public funding for LSD research. Institutes such as the NIH and Canadian health research agencies provide significant grants to support research, enabling therapeutic innovation and growth of future treatment pipelines.

Key companies active in the Lysosomal Storage Disease Treatment Market include Sigilon Therapeutics, Pfizer, Orphazyme, Alexion Pharmaceuticals, Sangamo Therapeutics, JCR Pharmaceuticals, Avrobio, Genzyme (Sanofi), Orchard Therapeutics, Takeda Pharmaceutical Company, BioMarin, and Amicus Therapeutics. Leading players are strengthening their position by investing in innovative therapies like gene editing platforms and next-generation enzyme replacement treatments. Strategic collaborations with academic institutions and biotech firms are expanding research capabilities. Companies are also developing robust global distribution networks to ensure market access, while engaging in targeted awareness and screening initiatives to boost early diagnosis rates. Through public-private partnerships and registry-based research, firms are accelerating clinical trials and enhancing patient recruitment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Disease type trends

- 2.2.4 Age group trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing diagnosis due to newborn-screening programs

- 3.2.1.2 Growing pipeline of gene and enzyme therapies

- 3.2.1.3 Advancement in molecular and biomarker-based diagnosis

- 3.2.1.4 Increasing shift towards disease-modifying and curative therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Limited penetration in low-and middle-income countries (LMICs)

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand of gene therapy and genome editing

- 3.2.3.2 Rise in specialized rare disease treatment centers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Enzyme replacement therapy

- 5.3 Stem cell transplants

- 5.4 Substrate reduction therapy

- 5.5 Other treatment types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gaucher disease

- 6.3 Mucopolysaccharidoses

- 6.4 Pompe disease

- 6.5 Fabry disease

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Homecare settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alexion Pharmaceuticals

- 10.2 Amicus Therapeutics

- 10.3 Avrobio

- 10.4 BioMarin

- 10.5 JCR Pharmaceuticals

- 10.6 Johnson & Johnson (Actelion Pharmaceuticals)

- 10.7 Orchard Therapeutics

- 10.8 Orphazyme

- 10.9 Pfizer

- 10.10 Sanofi (Genzyme Corporation)

- 10.11 Sigilon Therapeutics

- 10.12 Sangamo therapeutics

- 10.13 Takeda Pharmaceutical Company (Shire)

溶小體儲積症市場:按疾病類型、治療類型、治療應用和最終用戶分類 - 全球預測 2026-2032 年

溶小體儲積症市場:按疾病類型、治療類型、治療應用和最終用戶分類 - 全球預測 2026-2032 年 溶小體儲積症治療市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、製程、實施類型、功能及解決方案分類

溶小體儲積症治療市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、製程、實施類型、功能及解決方案分類 溶小體疾病治療市場-全球產業規模、佔有率、趨勢、機會和預測,按疾病類型、療法、給藥途徑、最終用戶、地區和競爭格局分類,2020-2030年預測溶小體貯積症治療市場-全球產業規模、佔有率、趨勢、機會和預測(按治療類型、疾病類型、地區和競爭細分,2020-2030 年)

溶小體疾病治療市場-全球產業規模、佔有率、趨勢、機會和預測,按疾病類型、療法、給藥途徑、最終用戶、地區和競爭格局分類,2020-2030年預測溶小體貯積症治療市場-全球產業規模、佔有率、趨勢、機會和預測(按治療類型、疾病類型、地區和競爭細分,2020-2030 年) 美國溶小體儲積症治療市場規模、佔有率和趨勢分析報告:按類型、疾病類型、國家和細分市場預測,2025 年至 2033 年溶小體儲積症治療市場規模、佔有率和趨勢分析報告:按治療類型、疾病類型、地區和細分市場預測,2025 年至 2033 年

美國溶小體儲積症治療市場規模、佔有率和趨勢分析報告:按類型、疾病類型、國家和細分市場預測,2025 年至 2033 年溶小體儲積症治療市場規模、佔有率和趨勢分析報告:按治療類型、疾病類型、地區和細分市場預測,2025 年至 2033 年 溶小體儲積症治療的全球市場,規模,佔有率,趨勢,產業分析報告:各疾病類型,各治療類型,各終端用戶,各地區 - 市場預測,2025年~2034年溶小體貯積症治療市場 - 全球產業規模、佔有率、趨勢、機會和預測,按治療、適應症、按最終用戶、按地區和競爭進行細分,2020-2030 年預測

溶小體儲積症治療的全球市場,規模,佔有率,趨勢,產業分析報告:各疾病類型,各治療類型,各終端用戶,各地區 - 市場預測,2025年~2034年溶小體貯積症治療市場 - 全球產業規模、佔有率、趨勢、機會和預測,按治療、適應症、按最終用戶、按地區和競爭進行細分,2020-2030 年預測