|

市場調查報告書

商品編碼

1782149

免疫球蛋白市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Immunoglobulin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

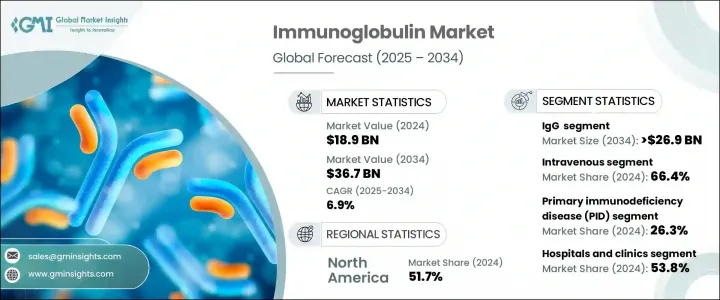

2024年,全球免疫球蛋白市場規模達189億美元,預計到2034年將以6.9%的複合年成長率成長,達到367億美元。這一成長主要歸因於各年齡層原發性和繼發性免疫缺陷疾病發生率的上升。隨著診斷技術的不斷進步和醫護人員意識的不斷提高,慢性發炎性脫髓鞘多發性神經病變和多灶性運動神經病變等複雜疾病的檢出率正在穩步上升。

這些疾病通常需要終身治療,包括免疫球蛋白療法,免疫球蛋白療法在控制症狀和預防感染方面發揮關鍵作用,從而推動了持續的產品需求。免疫球蛋白是免疫系統的重要組成部分,作為抗體,能夠辨識並中和病毒、細菌和毒素等有害病原體。這些糖蛋白由B細胞自然產生,可透過靜脈或皮下注射的方式,用於免疫系統需要額外支持或調節的患者。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 189億美元 |

| 預測值 | 367億美元 |

| 複合年成長率 | 6.9% |

自體免疫和免疫缺陷病例對免疫球蛋白療法的日益依賴,進一步增強了市場前景。這些療法用於糾正抗體缺陷並調節免疫活性,為患者提供可行的長期解決方案。預期壽命的延長,加上全球慢性病發病率的上升,正在創造更廣泛的需要免疫支持的患者群體,從而擴大需求。隨著免疫學研究的進展和產品可及性的提高,免疫球蛋白療法在神經內科、血液科和內科等眾多醫學學科的應用日益受到關注。持續的創新、已開發地區優惠的報銷方案以及對血漿採集網路的策略性投資預計將進一步加速市場成長。

在不同類型的免疫球蛋白中,IgG 繼續佔據主導地位。 2024 年,IgG 佔據了 74.1% 的市場佔有率,預計到 2034 年將超過 269 億美元,複合年成長率為 6.8%。其主導地位源自於廣泛的臨床應用和在多種疾病中均已證實的療效。 IgG 佔循環抗體的比例最高,對於中和病原體、提供被動免疫以及管理免疫相關疾病至關重要。其穩定的療效和廣泛的應用範圍使其成為醫療機構的首選。同時,IgA 領域正在成為成長最快的領域之一,預計到 2034 年的複合年成長率將達到 7.7%。人們對其在黏膜免疫中的作用及其潛在治療應用的日益認知,促進了這一成長勢頭。

從應用角度來看,市場細分為各種疾病,例如慢性發炎性脫髓鞘性多發性神經病變、多灶性運動神經病變、原發性和繼發性免疫缺陷疾病、格林-巴利綜合症、免疫性血小板減少性紫斑症以及其他利基疾病。原發性免疫缺陷症 (PID) 細分市場在 2024 年佔據市場主導地位,市佔率為 26.3%,預計複合年成長率將達到 7.1%。此細分市場的需求源自於疾病的終身性,需要持續的免疫球蛋白治療才能維持足夠的免疫功能。 PID 患者缺乏產生功能性抗體的能力,且極易受到頻繁感染,因此免疫球蛋白注射成為疾病管理的重要組成部分。它在降低感染風險、減少住院率和改善患者整體預後方面發揮關鍵作用。

就最終用途而言,醫院和診所佔據全球市場主導地位,2024 年的市佔率為 53.8%。這些場所是接受免疫球蛋白治療的患者的主要照護場所,尤其是需要醫療監督和專用設備的靜脈注射治療。醫院的受控環境確保了輸液操作的安全,並在出現不良反應時能夠立即介入。由於需要反覆和長期給藥,患者通常依賴醫院和診所進行持續、安全的給藥。

從地區來看,北美成為最大的市場,2024 年佔 51.7% 的佔有率。該地區擁有先進的醫療保健體系、健全的報銷政策以及完善的血漿採集基礎設施。免疫相關疾病的高發病率和持續的臨床創新進一步鞏固了其領先地位。老齡人口的不斷成長和診斷能力的提升也是該地區市場強勁的關鍵因素。

市場參與者憑藉強大的供應鏈、持續的產品創新和策略合作夥伴關係保持領先地位。他們在血漿分離方面的專業知識以及對治療一致性的關注賦予了他們競爭優勢。各公司也在投資新興市場,以挖掘新的需求並減少對傳統製造技術的依賴,從而為更廣泛的全球市場滲透鋪平道路。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 免疫缺陷疾病發生率上升

- 擴大在神經系統疾病和自體免疫疾病的應用

- 全球人口老化

- 改進診斷意識和篩檢計劃

- 產業陷阱與挑戰

- 治療費用高昂

- 血漿供應限制

- 市場機會

- 重組免疫球蛋白的開發

- 新興經濟體需求不斷成長

- 成長動力

- 成長潛力分析

- 監管格局

- 技術進步

- 當前的技術趨勢

- 新興技術

- 報銷場景

- 未來市場趨勢

- 差距分析

- 管道分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 免疫球蛋白G

- 免疫球蛋白A

- 免疫球蛋白M

- 免疫球蛋白D

- 免疫球蛋白E

第6章:市場估計與預測:按管理路線,2021 - 2034 年

- 主要趨勢

- 靜脈注射(IVIg)

- 皮下(SCIg)

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 慢性發炎性脫髓鞘多發性神經病變(CIDP)

- 多灶性運動神經病變(MMN)

- 原發性免疫缺陷症(PID)

- 繼發性免疫缺陷症(SID)

- 格林-巴利綜合症

- 免疫性血小板減少性紫斑症(ITP)

- 其他應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院和診所

- 門診手術中心

- 居家照護環境

- 其他最終用戶

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ADMA Biologics

- Baxter international

- Bio Products Laboratory

- CSL Behring

- Emergent BioSolutions

- Grifols SA

- Johnson & Johnson (Omrix Biopharmaceuticals)

- Kedrion Biopharma

- LFB Group

- Octapharma AG

- Pfizer

- Shanghai RAAS Blood Products

- Takeda Pharmaceutical Company

The Global Immunoglobulin Market was valued at USD 18.9 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 36.7 billion by 2034. This expansion is largely attributed to the rising occurrence of immunodeficiency disorders, both primary and secondary, across various age groups. With continued advancements in diagnostics and greater awareness among healthcare providers, detection rates of complex conditions like chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy are steadily increasing.

These conditions often require lifelong treatment involving immunoglobulin therapies, which play a key role in controlling symptoms and preventing infections, thereby fueling consistent product demand. Immunoglobulins are essential components of the immune system, functioning as antibodies that recognize and neutralize harmful pathogens such as viruses, bacteria, and toxins. Produced naturally by B cells, these glycoproteins are administered either intravenously or subcutaneously to patients whose immune systems require additional support or modulation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.9 Billion |

| Forecast Value | $36.7 Billion |

| CAGR | 6.9% |

The growing reliance on immunoglobulin-based therapies in autoimmune and immune deficiency cases continues to strengthen the market outlook. These therapies are used to correct antibody deficiencies and regulate immune activity, offering patients a viable long-term solution. Increasing life expectancy, coupled with a rise in chronic disease incidence globally, is creating a broader patient base that requires immune support, thereby adding to the demand pool. As immunology research progresses and product accessibility improves, the use of immunoglobulin therapy is gaining traction across numerous medical disciplines, including neurology, hematology, and internal medicine. Continuous innovation, favorable reimbursement scenarios in developed regions, and strategic investments in plasma collection networks are expected to further accelerate market growth.

Among the different immunoglobulin classes, IgG continues to hold the dominant position. In 2024, the IgG segment captured a market share of 74.1% and is anticipated to surpass USD 26.9 billion by 2034, with a CAGR of 6.8%. Its dominance stems from broad clinical usage and well-established efficacy in a wide range of conditions. IgG represents the highest proportion of circulating antibodies and is essential for neutralizing pathogens, offering passive immunity, and managing immune-related conditions. Its consistent therapeutic performance and wide application range make it the preferred choice across healthcare settings. Meanwhile, the IgA segment is emerging as one of the fastest-growing, projected to grow at a CAGR of 7.7% through 2034. Growing recognition of its role in mucosal immunity and its potential therapeutic applications is contributing to this increased momentum.

From an application perspective, the market is segmented into various conditions such as chronic inflammatory demyelinating polyneuropathy, multifocal motor neuropathy, primary and secondary immunodeficiency diseases, Guillain-Barre syndrome, immune thrombocytopenic purpura, and other niche disorders. The primary immunodeficiency disease (PID) segment led the market in 2024 with a share of 26.3% and is forecasted to expand at a CAGR of 7.1%. The demand in this segment is driven by the lifelong nature of the condition, which requires consistent immunoglobulin therapy to maintain adequate immune function. Patients with PID lack the ability to produce functional antibodies and are highly vulnerable to frequent infections, making immunoglobulin administration a vital component of disease management. It plays a critical role in reducing infection risks, limiting hospital admissions, and enhancing overall patient outcomes.

In terms of end use, the hospital and clinic segment dominated the global market with a market share of 53.8% in 2024. These settings serve as the primary point of care for patients receiving immunoglobulin therapy, particularly intravenous forms that demand medical supervision and specialized equipment. The controlled environment of hospitals ensures safe infusion practices and allows immediate intervention in case of adverse reactions. Given the requirement for repeated and long-term dosing, patients often rely on hospitals and clinics for consistent and secure administration.

Regionally, North America emerged as the largest market, commanding a share of 51.7% in 2024. The region benefits from advanced healthcare systems, robust reimbursement policies, and a well-established infrastructure for plasma collection. The high prevalence of immune-related disorders and ongoing clinical innovation further contribute to its leading position. The expanding elderly population and improved diagnostic capabilities are also key contributors to the region's market strength.

Market players are maintaining their leadership through strong supply chains, continuous product innovation, and strategic partnerships. Their expertise in plasma fractionation and focus on therapeutic consistency give them a competitive edge. Companies are also investing in emerging markets to tap into new demand and reduce dependence on traditional manufacturing techniques, paving the way for broader global market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Route of administration trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of immunodeficiency disorders

- 3.2.1.2 Expanding applications in neurological and autoimmune diseases

- 3.2.1.3 Global aging population

- 3.2.1.4 Improved diagnostic awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of therapy

- 3.2.2.2 Plasma supply constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recombinant immunoglobulins

- 3.2.3.2 Rising demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Pipeline analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 IgG

- 5.3 IgA

- 5.4 IgM

- 5.5 IgD

- 5.6 IgE

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Intravenous (IVIg)

- 6.3 Subcutaneous (SCIg)

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chronic inflammatory demyelinating polyneuropathy (CIDP)

- 7.3 Multifocal motor neuropathy (MMN)

- 7.4 Primary immunodeficiency disease (PID)

- 7.5 Secondary immunodeficiency disease (SID)

- 7.6 Guillain-Barre syndrome

- 7.7 Immune thrombocytopenic purpura (ITP)

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Ambulatory surgical centers

- 8.4 Homecare settings

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ADMA Biologics

- 10.2 Baxter international

- 10.3 Bio Products Laboratory

- 10.4 CSL Behring

- 10.5 Emergent BioSolutions

- 10.6 Grifols SA

- 10.7 Johnson & Johnson (Omrix Biopharmaceuticals)

- 10.8 Kedrion Biopharma

- 10.9 LFB Group

- 10.10 Octapharma AG

- 10.11 Pfizer

- 10.12 Shanghai RAAS Blood Products

- 10.13 Takeda Pharmaceutical Company

免疫球蛋白產品市場:依產品類型、原料、給藥途徑及應用分類-2026-2032年全球市場預測

免疫球蛋白產品市場:依產品類型、原料、給藥途徑及應用分類-2026-2032年全球市場預測 免疫球蛋白市場規模、佔有率、趨勢和預測:按產品、應用、給藥途徑和地區分類,2026-2034年

免疫球蛋白市場規模、佔有率、趨勢和預測:按產品、應用、給藥途徑和地區分類,2026-2034年 免疫球蛋白市場規模、佔有率、成長及全球產業分析:按類型和應用、區域的洞察,2026-2034年的預測IgE過敏血液檢測市場:依檢測類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測

免疫球蛋白市場規模、佔有率、成長及全球產業分析:按類型和應用、區域的洞察,2026-2034年的預測IgE過敏血液檢測市場:依檢測類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測 靜脈注射免疫球蛋白市場機會、成長要素、產業趨勢分析及2026-2035年預測。全球免疫球蛋白市場規模、佔有率、趨勢和成長分析報告(2026-2034年)人類高免疫球蛋白市場按產品類型、給藥途徑、應用和最終用戶分類-2026-2032年全球預測按給藥途徑、適應症、通路和最終用戶分類的高免疫球蛋白產品市場—2026-2032年全球預測特異性IgE血液檢測過敏檢測市場(按檢測類型、過敏原類型、過敏類型、應用和最終用戶分類),全球預測,2026-2032年

靜脈注射免疫球蛋白市場機會、成長要素、產業趨勢分析及2026-2035年預測。全球免疫球蛋白市場規模、佔有率、趨勢和成長分析報告(2026-2034年)人類高免疫球蛋白市場按產品類型、給藥途徑、應用和最終用戶分類-2026-2032年全球預測按給藥途徑、適應症、通路和最終用戶分類的高免疫球蛋白產品市場—2026-2032年全球預測特異性IgE血液檢測過敏檢測市場(按檢測類型、過敏原類型、過敏類型、應用和最終用戶分類),全球預測,2026-2032年 免疫球蛋白市場規模、佔有率和成長分析(按產品類型、劑型、給藥途徑、應用、分銷管道和地區分類)-2026-2033年產業預測

免疫球蛋白市場規模、佔有率和成長分析(按產品類型、劑型、給藥途徑、應用、分銷管道和地區分類)-2026-2033年產業預測