|

市場調查報告書

商品編碼

1782131

生成式人工智慧解決方案市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Generative AI solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

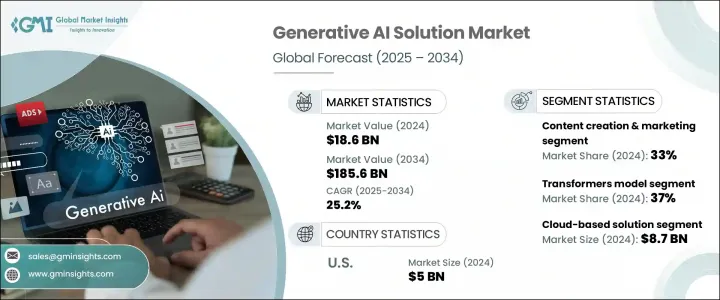

2024年,全球生成式人工智慧解決方案市場規模達186億美元,預計到2034年將以25.2%的複合年成長率成長,達到1856億美元。這一成長主要源於媒體、醫療保健、汽車和企業軟體等行業對超個人化、自動化和創意內容生成日益成長的需求。生成模型(例如生成對抗網路 (GAN)、擴散網路和大型語言模型)曾經被限制在實驗室和創意領域,如今已成為企業創新工作的核心。遵循嚴格規則的傳統人工智慧正被能夠產生類似人類的文字、圖像、音訊和程式碼的生成系統所取代。這種演變正在提高效率、增強設計流程並豐富產品體驗。專注於應用的公司與領先的人工智慧實驗室之間的合作正在加速人工智慧的普及。

因此,針對特定行業挑戰而量身定做的垂直解決方案正成為常態,這標誌著人工智慧應用向產業客製化方向的轉變。這一日益成長的趨勢反映了行業對精準度、相關性和實際適用性的更廣泛需求,而千篇一律的模型已無法滿足複雜的營運需求。各組織越來越重視與其監管環境、資料類型和客戶期望緊密契合的人工智慧工具。從金融、醫療保健到零售和製造業,這些針對特定領域最佳化的人工智慧系統正在協助加快部署速度、增強決策能力並提高投資報酬率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 186億美元 |

| 預測值 | 1856億美元 |

| 複合年成長率 | 25.2% |

基於Transformer的模型細分市場在2024年佔據了37%的佔有率,預計到2034年將以26%的複合年成長率成長。這些架構支撐著幾乎所有現代生成式解決方案,例如GPT、PaLM、LLaMA和Claude。它們的可擴展性、靈活性和性能使其在各行各業中廣泛應用。 Transformer如今為辦公室軟體、程式碼產生工具以及法律、金融和行銷等領域的企業應用程式中的AI副駕駛提供支持,鞏固了其作為生成式AI支柱的地位。

2024年,內容創作和行銷佔了33%的市場佔有率,預計2025年至2034年的複合年成長率將達到25%。企業越來越依賴產生工具來大規模製作SEO最佳化的部落格文章、廣告活動、產品描述、電子郵件內容和促銷多媒體內容。這些系統可協助行銷人員實現工作流程自動化,同時保持品牌基調,並根據消費者洞察提供客製化的訊息。這種轉變正在幫助品牌有效率地滿足日益成長的內容需求,提升參與度,並最佳化行銷活動的效果。

美國生成式人工智慧解決方案市場佔85%的市場佔有率,2024年市場規模達50億美元。這一領先地位源於其豐富的技術基礎設施、先進的學術和企業研究環境以及大量的公私投資。由於主要的人工智慧創新者總部設在美國,並得到世界一流大學、新創公司和研究中心的支持,美國在生成式變壓器的開發和大規模部署方面始終處於領先地位。

該市場的領先公司包括Google、英偉達、Adobe、亞馬遜網路服務、微軟、IBM 和 OpenAI。這些公司正在推動創新並為產業設定策略方向。為了鞏固市場主導地位,生成人工智慧領域的主要參與者正在推行幾項核心策略。首先,他們正積極拓展研發,開發融合文字、影像、音訊和視訊功能的下一代架構和多模式模型。其次,與行業領導者合作,提供客製化解決方案,滿足從醫療診斷到汽車設計的垂直領域需求。第三,致力於使人工智慧存取更加民主化,例如提供開放 API、開發者平台和免費增值服務,這些舉措正在擴大用戶參與度並加速其普及。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 電子元件供應商

- 設備製造商

- 服務提供者

- 系統整合商

- 最終用途

- 成本結構

- 利潤率

- 每個階段的增值

- 影響供應鏈的因素

- 破壞者

- 供應商格局

- 對部隊的影響

- 成長動力

- 企業對自動化和效率的需求不斷成長

- 行銷和客戶體驗的超個人化

- 人工智慧代理和副駕駛在企業職能中的擴展

- 模型能力的進步

- 雲端可用性和策略合作夥伴關係

- 產業陷阱與挑戰

- 幻覺和不準確的輸出

- 資料隱私和安全風險

- 市場機會

- 垂直特定大型語言模型 (LLM)

- 多模態生成式人工智慧解決方案(文字+圖像+音訊+影片)

- 中小企業採用基於 SaaS 的 GenAI

- 人工智慧程式碼產生和 DevOps 自動化

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 技術與創新格局

- 現有技術

- 基於 Transformer 的大型語言模型 (LLM)

- 生成對抗網路(GAN)

- 擴散模型

- 變分自動編碼器 (VAE)

- 新興技術

- 多模態生成式人工智慧解決方案

- 檢索增強生成 (RAG) 系統

- 低程式碼/無程式碼 GenAI 開發平台

- 安全、校準和評估工具包

- 現有技術

- 專利分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 成本細分分析

- 永續性分析

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 技術演進與創新路線圖

- 基礎模型和大型語言模型(LLM)

- 多模態人工智慧系統

- 專門的GENAI應用程式

- 新興科技與未來發展

- 定價模型與貨幣化策略

- GenAI定價模型的演變

- 基於訂閱的定價分析

- 免費增值和免費套餐策略

- 企業授權和客製化定價

- 收入最佳化和貨幣化趨勢

- 定價競爭分析

- 未來定價模型的演變

- 企業採用和實施

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 變形金剛模型

- 文字生成

- 程式碼生成

- 總結

- 問答

- 多模態轉換器(文字+圖像/影片)

- 生成對抗網路(GAN)

- 影像生成

- 影片生成

- 條件

- 超解析度

- 風格轉換

- 擴散模型

- 影像合成

- 視訊合成

- 文字到圖像的傳播

- 修復/編輯工具

- 創意設計模型

- 變分自動編碼器 (VAE)

- 潛在空間生成

- 語意資料建模

- 異常檢測生成

- 其他

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 內容創作與行銷

- 數位行銷和廣告

- 社群媒體內容生成

- 部落格和文章寫作

- 創意設計與媒體製作

- 客戶服務與支援

- 人工智慧聊天機器人和虛擬助手

- 自動響應系統

- 客戶查詢解決

- 多語言支援解決方案

- 軟體開發和 IT

- 程式碼生成和完成

- 錯誤檢測和解決

- 文件生成

- API開發和測試

- 研究與分析

- 數據分析和洞察生成

- 科學研究援助

- 市場研究與競爭情報

- 財務分析和報告

- 教育和培訓

- 評估和評價工具

- 專業技能發展

- 其他

第7章:市場估計與預測:按部署,2021 - 2034 年

- 主要趨勢

- 基於雲端

- 本地

- 混合

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫療保健和生命科學

- 藥物發現與開發

- 醫學影像和診斷

- 臨床文件和記錄

- 病人照護和遠距醫療

- 金融服務及銀行業務

- 風險評估與管理

- 詐欺檢測與預防

- 投資研究與分析

- 客戶服務自動化

- 教育和電子學習

- 個人化學習平台

- 內容創作與課程開發

- 學生評估與評價

- 行政流程自動化

- 媒體和娛樂

- 內容創作與製作

- 遊戲與互動媒體

- 音樂和音訊生成

- 視覺效果和動畫

- 法律與專業服務

- 合約生成和管理

- 合規與監理支持

- 零售與電子商務

- 客戶體驗個人化

- 行銷和廣告最佳化

- 製造業和工業

- 品質控制和檢驗

- 預測性維護解決方案

- 其他

第9章:市場估計與預測:依組織規模,2021 - 2034 年

- 主要趨勢

- 大型企業

- 中小企業

第10章:市場估計與預測:按地區,2021 - 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Adobe

- Amazon Web Services (AWS)

- Apple

- Anthropic

- Baidu

- DeepMind

- Genie AI

- IBM

- Intel

- Meta

- Microsoft

- MOSTLY AI

- NVIDIA

- OpenAI

- Oracle

- Salesforce

- SAP

- Synthesia

- UiPath

- Unity Technologies

The Global Generative AI solution Market was valued at USD 18.6 billion in 2024 and is estimated to grow at a CAGR of 25.2% to reach USD 185.6 billion by 2034. The expansion is driven by increased demand for hyper-personalization, automation, and creative content generation across industries like media, healthcare, automotive, and enterprise software. Generative models, once confined to labs and creative niches-such as GANs, diffusion networks, and large language models-have become central to corporate innovation efforts. Traditional AI that followed rigid rules is being replaced by generative systems capable of producing human-like text, images, audio, and code. This evolution is driving efficiency, enhancing design processes, and enriching product experiences. Collaborations between application-focused firms and leading AI labs are accelerating adoption.

As a result, vertical-specific solutions tailored to distinct industry challenges are becoming the norm, signaling a shift towards sector-tailored AI implementations. This growing trend reflects a broader industry demand for precision, relevance, and real-world applicability, where one-size-fits-all models no longer meet complex operational needs. Organizations are increasingly prioritizing AI tools that align closely with their regulatory environments, data types, and customer expectations. From finance and healthcare to retail and manufacturing, these domain-optimized AI systems are enabling faster deployment, enhanced decision-making, and better return on investment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.6 Billion |

| Forecast Value | $185.6 Billion |

| CAGR | 25.2% |

The transformer-based models segment held a 37% share in 2024 and is expected to grow at a CAGR of 26% through 2034. These architectures underpin nearly all modern generative solutions, such as GPT, PaLM, LLaMA, and Claude. Their scalability, flexibility, and performance have enabled widespread adoption across industries. Transformers now power AI copilots in office software, code generation tools, and enterprise applications in sectors such as legal, finance, and marketing, cementing their position as the backbone of generative AI.

Content creation and marketing held a 33% share in 2024 and is forecast to grow at a CAGR of 25% from 2025 to 2034. Businesses increasingly rely on generative tools to produce SEO-optimized blog posts, ad campaigns, product descriptions, email content, and promotional multimedia at scale. These systems help marketers automate workflows while maintaining brand tone and delivering tailored messaging based on consumer insights. This shift is helping brands efficiently meet growing content demands, improve engagement, and optimize campaign performance.

U.S. Generative AI Solution Market held 85% share and generated USD 5 billion in 2024. This leadership stems from a rich tech infrastructure, advanced academic and corporate research environments, and substantial public-private investment. With major AI innovators headquartered in the U.S., supported by world-class universities, startups, and research hubs, the country remains at the forefront of generative transformer development and deployment at scale.

Leading firms in this market include Google, NVIDIA, Adobe, Amazon Web Services, Microsoft, IBM, and OpenAI. These companies are driving innovation and setting strategic direction for the industry. To solidify their market dominance, major players in the generative AI space are pursuing several core strategies. First, they are aggressively expanding R&D into next-generation architectures and multimodal models that fuse text, image, audio, and video capabilities. Second, partnerships with industry-specific leaders enable tailored solutions that meet vertical needs, from healthcare diagnostics to automotive design. Third, efforts to democratize AI access, such as offering open APIs, developer platforms, and freemium services, are widening user engagement and accelerating adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 Deployment

- 2.2.5 End use industry

- 2.2.6 Organization size

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Electronic component suppliers

- 3.1.1.2 Equipment manufacturers

- 3.1.1.3 Service providers

- 3.1.1.4 System integrators

- 3.1.1.5 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising enterprise demand for automation and efficiency

- 3.2.1.2 Hyper personalization in marketing and customer experience

- 3.2.1.3 Expansion of AI agents and Copilots across enterprise functions

- 3.2.1.4 Advancements in model capabilities

- 3.2.1.5 Cloud availability and strategic partnerships

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Hallucinations and inaccurate output

- 3.2.2.2 Data privacy and security risks

- 3.2.3 Market Opportunities

- 3.2.3.1 Vertical-specific large language models (LLMs)

- 3.2.3.2 Multimodal Generative AI solution (Text + Image + Audio + Video)

- 3.2.3.3 SaaS-based GenAI adoption among SMEs

- 3.2.3.4 AI-powered code generation & DevOps automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.1.1 Transformer-based large language models (LLMs)

- 3.6.1.2 Generative adversarial networks (GANs)

- 3.6.1.3 Diffusion models

- 3.6.1.4 Variational autoencoders (VAEs)

- 3.6.2 Emerging technologies

- 3.6.2.1 Multimodal Generative AI solution

- 3.6.2.2 Retrieval-Augmented Generation (RAG) Systems

- 3.6.2.3 Low-Code/No-Code GenAI Development Platforms

- 3.6.2.4 Safety, Alignment & Evaluation Toolkits

- 3.6.1 Current technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Cost breakdown analysis

- 3.10 Sustainability analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Technology evolution and innovation roadmap

- 3.11.1 Foundation models and large language models (LLMs)

- 3.11.2 Multimodal AI systems

- 3.11.3 Specialized GENAI applications

- 3.11.4 Emerging technologies and future developments

- 3.12 Pricing models and monetization strategies

- 3.12.1 GenAI pricing model evolution

- 3.12.2 Subscription-based pricing analysis

- 3.12.3 Freemium and free tier strategies

- 3.12.4 Enterprise licensing and custom pricing

- 3.12.5 Revenue optimization and monetization trends

- 3.12.6 Pricing competitive analysis

- 3.12.7 Future pricing model evolution

- 3.13 Enterprise adoption and implementation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Transformers model

- 5.2.1 Text generation

- 5.2.2 Code generation

- 5.2.3 Summarization

- 5.2.4 Question answering (Q&A)

- 5.2.5 Multimodal transformers (text+ image/video)

- 5.3 Generative adversarial networks (GAN)

- 5.3.1 Image generation

- 5.3.2 Video generation

- 5.3.3 Conditional

- 5.3.4 Super resolution

- 5.3.5 Style transfer

- 5.4 Diffusion models

- 5.4.1 Image synthesis

- 5.4.2 Video synthesis

- 5.4.3 Text-to-image diffusion

- 5.4.4 Inpainting/ editing tools

- 5.4.5 Creative design models

- 5.5 Variational autoencoders (VAEs)

- 5.5.1 Latent space generation

- 5.5.2 Semantic data modelling

- 5.5.3 Anomaly detection generation

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Content creation and marketing

- 6.2.1 Digital marketing and advertising

- 6.2.2 Social media content generation

- 6.2.3 Blog and article writing

- 6.2.4 Creative design and media production

- 6.3 Customer service and support

- 6.3.1 AI chatbots and virtual assistants

- 6.3.2 Automated response systems

- 6.3.3 Customer query resolution

- 6.3.4 Multilingual support solutions

- 6.4 Software development and IT

- 6.4.1 Code Generation and Completion

- 6.4.2 Bug Detection and Resolution

- 6.4.3 Documentation Generation

- 6.4.4 API development and testing

- 6.5 Research and analytics

- 6.5.1 Data analytics and insights generation

- 6.5.2 Scientific research assistance

- 6.5.3 Market research and competitive intelligence

- 6.5.4 Financial analysis and reporting

- 6.6 Education and training

- 6.6.1 Assessment and evaluation tools

- 6.6.2 Professional skills development

- 6.6.3 Others

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Healthcare and life sciences

- 8.2.1 Drug discovery and development

- 8.2.2 Medical imaging and diagnostics

- 8.2.3 Clinical documentation and records

- 8.2.4 Patient care and telemedicine

- 8.3 Financial services and banking

- 8.3.1 Risk assessment and management

- 8.3.2 Fraud detection and prevention

- 8.3.3 Investment research and analysis

- 8.3.4 Customer service automation

- 8.4 Education and E-learning

- 8.4.1 Personalized learning platforms

- 8.4.2 Content creation and curriculum development

- 8.4.3 Student assessment and evaluation

- 8.4.4 Administrative process automation

- 8.5 Media and entertainment

- 8.5.1 Content creation and production

- 8.5.2 Gaming and interactive media

- 8.5.3 Music and audio generation

- 8.5.4 Visual effects and animation

- 8.6 Legal and professional services

- 8.6.1 Contract generation and management

- 8.6.2 Compliance and regulatory support

- 8.7 Retail and E-commerce

- 8.7.1 Customer experience personalization

- 8.7.2 Marketing and advertising optimization

- 8.8 Manufacturing and Industrial

- 8.8.1 Quality control and inspection

- 8.8.2 Predictive maintenance solutions

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Large Enterprises

- 9.3 Small and Medium Enterprises (SMEs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 South Korea

- 10.3.5 Australia

- 10.3.6 Singapore

- 10.3.7 Malaysia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Adobe

- 11.2 Amazon Web Services (AWS)

- 11.3 Apple

- 11.4 Anthropic

- 11.5 Baidu

- 11.6 DeepMind

- 11.7 Genie AI

- 11.8 Google

- 11.9 IBM

- 11.10 Intel

- 11.11 Meta

- 11.12 Microsoft

- 11.13 MOSTLY AI

- 11.14 NVIDIA

- 11.15 OpenAI

- 11.16 Oracle

- 11.17 Salesforce

- 11.18 SAP

- 11.19 Synthesia

- 11.20 UiPath

- 11.21 Unity Technologies

2026年人力資源領域生成式人工智慧(AI)全球市場報告2026年全球生成式人工智慧媒體軟體市場報告

2026年人力資源領域生成式人工智慧(AI)全球市場報告2026年全球生成式人工智慧媒體軟體市場報告 3D建模類型AIGC市場:按組件、技術、輸入方法、應用和部署方式分類,全球預測,2026-2032年基於影像的AIGC市場:按影像類型、模型類型、部署方式、應用領域和最終用戶分類,全球預測,2026-2032年

3D建模類型AIGC市場:按組件、技術、輸入方法、應用和部署方式分類,全球預測,2026-2032年基於影像的AIGC市場:按影像類型、模型類型、部署方式、應用領域和最終用戶分類,全球預測,2026-2032年 生成式人工智慧市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類

生成式人工智慧市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類 AI在3D資產生成和紋理繪製領域的市場規模、佔有率和預測:依資產類型、AI模型、整合方式和最終用戶(遊戲、元宇宙、視覺特效)劃分 - 全球預測(2026-2036)AI音樂生成與作曲軟體市場規模、佔有率及預測:依音樂類型、客製化選項、授權模式(免版稅、獨家)及最終用戶(內容創作者、遊戲開發者) - 全球預測(2026-2036)

AI在3D資產生成和紋理繪製領域的市場規模、佔有率和預測:依資產類型、AI模型、整合方式和最終用戶(遊戲、元宇宙、視覺特效)劃分 - 全球預測(2026-2036)AI音樂生成與作曲軟體市場規模、佔有率及預測:依音樂類型、客製化選項、授權模式(免版稅、獨家)及最終用戶(內容創作者、遊戲開發者) - 全球預測(2026-2036) 全球生成式人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球生成式人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 生成式人工智慧市場機會、成長要素、產業趨勢分析及2026年至2035年預測

生成式人工智慧市場機會、成長要素、產業趨勢分析及2026年至2035年預測 生成式人工智慧晶片組市場規模、佔有率和趨勢分析報告:按晶片組類型、應用、最終用途、地區和細分市場預測(2026-2033 年)

生成式人工智慧晶片組市場規模、佔有率和趨勢分析報告:按晶片組類型、應用、最終用途、地區和細分市場預測(2026-2033 年)