|

市場調查報告書

商品編碼

1782089

甚高頻空地通訊站市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測VHF Air Ground Communication Stations Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

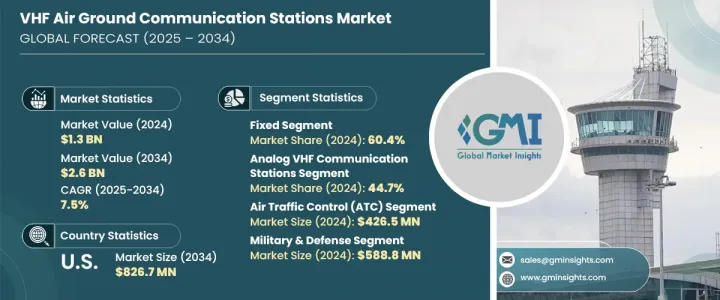

2024 年全球甚高頻空地通訊站市場價值為 13 億美元,預計到 2034 年將以 7.5% 的複合年成長率成長,達到 26 億美元。這一成長軌跡受到幾個關鍵因素的推動,其中最重要的是國際航空旅行的持續成長。隨著全球客運和貨運航班的增加,飛行員和空中交通管制員之間無縫、不間斷通訊的需求變得越來越重要。可靠的通訊系統不僅對於維護飛行安全至關重要,而且對於確保區域和國際航班網路的營運效率也至關重要。隨著航空網路的擴展以及商業和國防相關空中作業頻率的增加,各國被迫投資升級基礎設施,這為固定和攜帶式甚高頻通訊系統創造了機會。

全球空中交通管制框架的現代化在塑造市場格局方面發揮著重要作用。各國政府和監管機構正積極實施政策,強制部署先進的通訊技術,以滿足全球航空安全標準。新興經濟體也在推動市場擴張,特別是透過投資機場建設和升級航空基礎設施來應對不斷成長的客流量。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 26億美元 |

| 複合年成長率 | 7.5% |

對高可靠性通訊解決方案日益成長的需求不僅局限於民航,還涵蓋了緊急應變小組和軍隊。在這些領域,攜帶式甚高頻電台在快速部署、穩定連接和安全傳輸方面具有關鍵優勢,使其成為救災任務和戰術行動中不可或缺的一部分。隨著彈性和靈活性成為策略重點,對可擴展和行動通訊工具的需求也日益成長。

就產品類型而言,市場細分為固定式和攜帶式甚高頻空地通訊系統。 2024年,固定式系統佔據主導地位,佔全球營收的60.4%。這些系統是高流量區域和永久性設施的首選,因為這些區域對不間斷覆蓋和基礎設施級可靠性至關重要。隨著各國擴大機場容量和升級設施,預計對固定式甚高頻站的需求將保持強勁,尤其是在航空業快速成長的地區。攜帶式系統雖然在2024年的市佔率較小,為39.6%,但由於其在遠端或臨時營運中的多功能性,將繼續受到關注。

按技術分類,市場包括類比、數位和混合通訊站。類比甚高頻系統在2024年佔據最大佔有率,達到44.7%,這主要歸功於其廣泛的現有部署以及與舊航空系統的兼容性。在許多小型和區域性機場,尤其是在發展中地區,仍在使用類比站,利害關係人選擇分階段升級,而不是完全過渡到數位基礎設施。這確保了對模擬解決方案的持續需求,尤其是在維護和更換零件方面。

甚高頻空地通訊系統的應用涵蓋多項關鍵航空功能,包括用於固定翼和旋翼飛機的空中交通管制 (ATC)、航空運作管制 (AOC)、飛行資訊服務 (FIS)、緊急通訊和地面支援。其中,空中交通管制 (ATC) 領域在 2024 年創造了 4.265 億美元的市場規模,預計複合年成長率為 8.2%。隨著航空旅行的持續成長,航空當局致力於提高空中交通管理系統內通訊基礎設施的品質和可靠性。這種對營運效率和空域現代化的承諾直接轉化為對甚高頻通訊站的更強勁需求。

根據最終用途,市場進一步細分為商業、政府以及軍事和國防部門。軍事和國防部門在2024年成為最大的市場,市場價值達5.888億美元,預計複合年成長率為8.3%。這一成長歸因於在關鍵任務場景中對安全高效能通訊通道的需求。無論是在戰鬥、後勤或人道支援期間,國防行動都需要強大的空對地通訊能力。固定式和攜帶式甚高頻系統對於確保戰場協調和指揮都至關重要。

從區域來看,北美在2024年引領全球市場,佔全球總佔有率的35.2%,預計複合年成長率為7.3%。該地區的成長得益於對空中交通管制系統升級的持續投資、先進數位技術的部署以及大型系統整合商的湧現。預計到2034年,光是美國就將達到8.267億美元,這得益於基礎建設升級和航空業現代化措施的實施。

為甚高頻空地通訊站市場競爭格局做出貢獻的關鍵參與者包括泰雷茲集團、霍尼韋爾國際公司、柯林斯航太、埃爾比特系統公司、通用動力公司、萊昂納多公司、MORCOM國際公司、羅德與施瓦茨公司和Spectra集團。這些公司持續創新,拓展全球業務,增強了市場的長期成長潛力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 全球空中交通需求不斷成長

- 空中交通管制基礎設施現代化

- 嚴格的監管和安全標準

- 新興市場機場網路的擴張

- 國防和災難應變對靈活、快速部署解決方案的需求日益成長

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 監管複雜性與頻譜管理挑戰

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 未來市場趨勢

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021-2034

- 主要趨勢

- 固定的

- 便攜的

第6章:市場估計與預測:依技術,2021-2034 年

- 主要趨勢

- 類比甚高頻通訊站

- 數位甚高頻通訊站

- 混合甚高頻通訊站

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 空中交通管制(ATC)

- 航空運作管制(AOC)

- 航班資訊服務(FIS)

- 應急與災難通訊

- 地面支援行動

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 軍事與國防

- 政府

- 國土安全

- 公共行政

- 商業的

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳新銀行

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- AEROTHAI Business

- Becker Avionics Gmbh

- Collins Aerospace

- Elbit Systems

- General Dynamics Corporation

- Honeywell International Inc

- IACIT

- Jotron

- Leonardo SpA

- MORCOM International, Inc.

- Rohde & Schwarz

- Spectra Group

- Systems Interface Limited

- Thales Group

- Viasat Inc

The Global VHF Air Ground Communication Stations Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 2.6 billion by 2034. This growth trajectory is fueled by several key factors, the foremost being the continued increase in international air travel. As passenger and cargo flights multiply across the globe, the demand for seamless and uninterrupted communication between pilots and air traffic controllers is becoming more critical. Reliable communication systems are essential not only for maintaining flight safety but also for ensuring operational efficiency across regional and international flight networks. As aviation networks expand and the frequency of commercial and defense-related air operations rises, countries are compelled to invest in infrastructure upgrades, creating opportunities for both fixed and portable VHF communication systems.

The modernization of air traffic control frameworks worldwide plays a significant role in shaping the market landscape. Governments and regulatory authorities are actively implementing policies that enforce the deployment of advanced communication technologies to meet global aviation safety standards. Emerging economies are also contributing to market expansion, particularly by investing in airport development and upgrading their aviation infrastructure to accommodate rising passenger volumes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 7.5% |

This growing demand for high-reliability communication solutions extends beyond civilian aviation to include emergency response teams and military forces. In these sectors, portable VHF stations offer critical advantages in terms of quick deployment, robust connectivity, and secure transmissions, making them indispensable for disaster relief missions and tactical operations. As resilience and flexibility become strategic priorities, the need for scalable and mobile communication tools is gaining momentum.

In terms of product types, the market is segmented into fixed and portable VHF air ground communication systems. Fixed systems dominated the landscape in 2024, accounting for 60.4% of the global revenue. These systems are the preferred choice for high-traffic zones and permanent installations, where uninterrupted coverage and infrastructure-grade reliability are essential. With nations expanding airport capacities and upgrading facilities, the demand for fixed VHF stations is expected to remain strong, especially in regions undergoing rapid aviation growth. Portable systems, while representing a smaller market share of 39.6% in 2024, continue to gain attention due to their versatility in remote or temporary operations.

By technology, the market includes analog, digital, and hybrid communication stations. Analog VHF systems held the largest share at 44.7% in 2024, mainly due to their extensive existing deployment and compatibility with older aviation systems. In many smaller and regional airports, particularly in developing regions, analog stations remain in use, with stakeholders opting for phased upgrades over complete transitions to digital infrastructure. This ensures consistent demand for analog solutions, especially for maintenance and replacement parts.

The application of VHF air ground communication systems spans across several critical aviation functions. These include use in fixed-wing and rotary-wing aircraft for air traffic control (ATC), aeronautical operational control (AOC), flight information services (FIS), emergency communications, and ground support. Among these, the ATC segment generated USD 426.5 million in 2024 and is projected to grow at a CAGR of 8.2%. With air travel continuing to rise, aviation authorities are focused on improving the quality and reliability of communication infrastructure within air traffic management systems. This commitment to operational efficiency and airspace modernization directly translates to stronger demand for VHF communication stations.

The market is further segmented based on end use into commercial, government, and military & defense sectors. The military & defense segment emerged as the largest in 2024, with a market value of USD 588.8 million, and is forecast to grow at a CAGR of 8.3%. This growth is attributed to the need for secure and high-performance communication channels in mission-critical scenarios. Defense operations, whether during combat, logistics, or humanitarian support, require robust air-to-ground communication capabilities. Both fixed and portable VHF systems are vital in ensuring coordination and command in the field.

Regionally, North America led the global market in 2024, accounting for 35.2% of the total share and projected to expand at a CAGR of 7.3%. The region's growth is driven by continuous investments in upgrading air traffic control systems, the deployment of advanced digital technologies, and the presence of major system integrators. The United States alone is anticipated to reach USD 826.7 million by 2034, supported by infrastructure upgrades and the implementation of modernization initiatives in the aviation sector.

Key players contributing to the competitive dynamics of the VHF air ground communication stations market include Thales Group, Honeywell International Inc., Collins Aerospace, Elbit Systems, General Dynamics Corporation, Leonardo S.p.A., MORCOM International, Inc., Rohde & Schwarz, and Spectra Group. These companies continue to innovate and expand their global footprint, reinforcing the market's long-term growth potential.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.2 Disruptions

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global air traffic demands

- 3.3.1.2 Modernization of air traffic control infrastructure

- 3.3.1.3 Stringent regulatory and safety standards

- 3.3.1.4 Expansion of airport networks in emerging markets

- 3.3.1.5 Growing need for flexible, rapid-deployment solutions in defense and disaster response

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment and maintenance costs

- 3.3.2.2 Regulatory complexity and spectrum management challenges

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Pricing strategies

- 3.12 Emerging business models

- 3.13 Compliance requirements

- 3.14 Defense budget analysis

- 3.15 Global defense spending trends

- 3.16 Regional defense budget allocation

- 3.16.1 North America

- 3.16.2 Europe

- 3.16.3 Asia Pacific

- 3.16.4 Middle East and Africa

- 3.16.5 Latin America

- 3.17 Key defense modernization programs

- 3.18 Budget forecast (2025-2034)

- 3.18.1 Impact on industry growth

- 3.18.2 Defense budgets by country

- 3.19 Supply chain resilience

- 3.20 Geopolitical analysis

- 3.21 Workforce analysis

- 3.22 Digital transformation

- 3.23 Mergers, acquisitions, and strategic partnerships landscape

- 3.24 Risk assessment and management

- 3.25 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Portable

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Analog VHF communication stations

- 6.3 Digital VHF communication station

- 6.4 Hybrid VHF communication station

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Air traffic control (ATC)

- 7.3 Aeronautical operational control (AOC)

- 7.4 Flight information service (FIS)

- 7.5 Emergency & disaster communication

- 7.6 Ground support operations

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Military & Defense

- 8.3 Government

- 8.3.1 Homeland security

- 8.3.2 Public administration

- 8.4 Commercial

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AEROTHAI Business

- 10.2 Becker Avionics Gmbh

- 10.3 Collins Aerospace

- 10.4 Elbit Systems

- 10.5 General Dynamics Corporation

- 10.6 Honeywell International Inc

- 10.7 IACIT

- 10.8 Jotron

- 10.9 Leonardo S.p.A.

- 10.10 MORCOM International, Inc.

- 10.11 Rohde & Schwarz

- 10.12 Spectra Group

- 10.13 Systems Interface Limited

- 10.14 Thales Group

- 10.15 Viasat Inc

超高頻通訊市場規模、佔有率和成長分析:按頻段、組件、應用、最終用戶和地區分類-2026-2033年產業預測

超高頻通訊市場規模、佔有率和成長分析:按頻段、組件、應用、最終用戶和地區分類-2026-2033年產業預測 超高頻通訊市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、頻率範圍、雷達罩類型、地區和競爭格局分類,2021-2031年

超高頻通訊市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、頻率範圍、雷達罩類型、地區和競爭格局分類,2021-2031年 2026年甚高頻機載和地面通訊站全球市場報告

2026年甚高頻機載和地面通訊站全球市場報告 全球高頻通訊市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球高頻通訊市場規模、佔有率、趨勢和成長分析報告(2026-2034) VHF航空地面通訊站市場規模、佔有率和成長分析(按機場等級、類型、機場類別、應用和地區分類)-產業預測,2026-2033年

VHF航空地面通訊站市場規模、佔有率和成長分析(按機場等級、類型、機場類別、應用和地區分類)-產業預測,2026-2033年 甚高頻資料交換系統(VDES)-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

甚高頻資料交換系統(VDES)-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 甚高頻航空地面通訊站的全球市場全球超高頻通訊市場

甚高頻航空地面通訊站的全球市場全球超高頻通訊市場 超高頻通訊市場(按頻寬、組件、應用和地區):趨勢、競爭格局和預測(2019-2031年)

超高頻通訊市場(按頻寬、組件、應用和地區):趨勢、競爭格局和預測(2019-2031年) 到 2030 年 VHF 航空地面通訊站市場預測:按站類型、組件類型、部署類型、技術、應用、最終用戶和地區進行的全球分析

到 2030 年 VHF 航空地面通訊站市場預測:按站類型、組件類型、部署類型、技術、應用、最終用戶和地區進行的全球分析