|

市場調查報告書

商品編碼

1773474

肋骨骨折修復系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Rib Fracture Repair Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

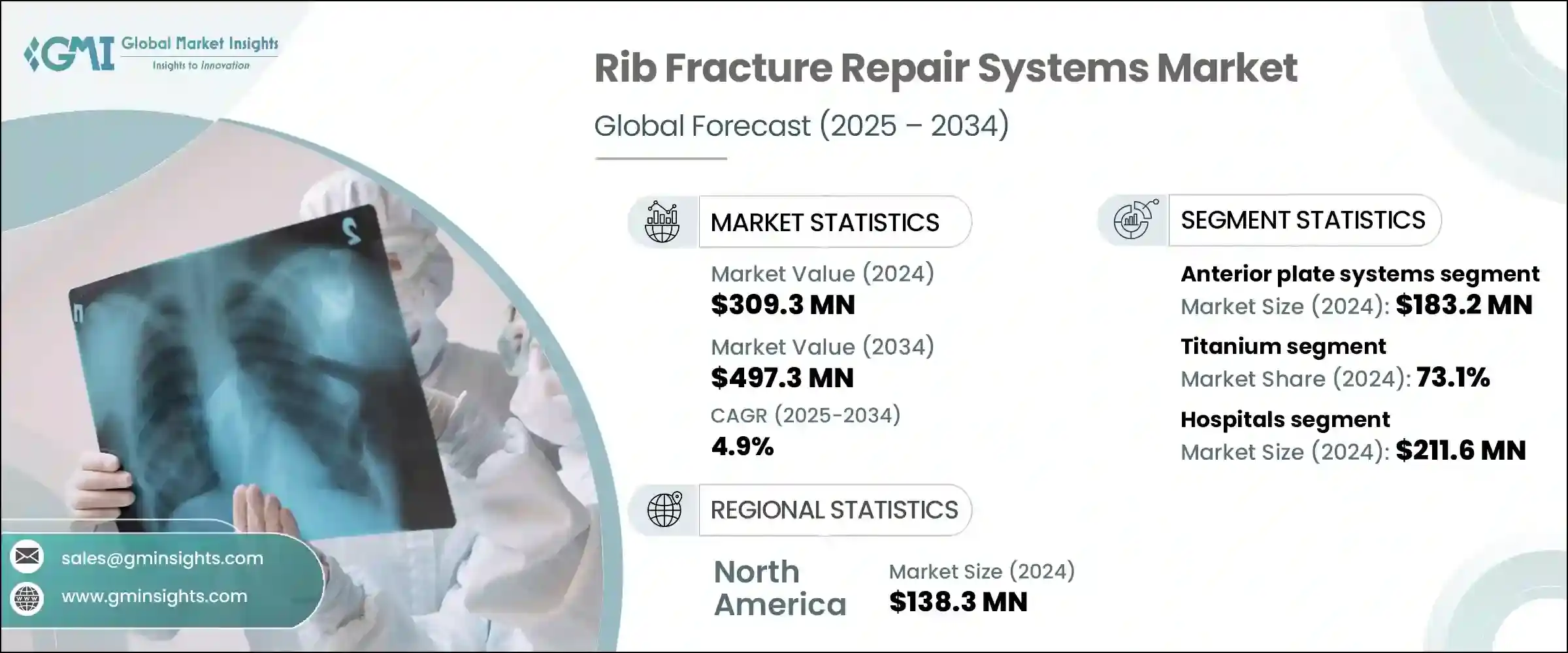

2024 年全球肋骨骨折修復系統市值為 3.093 億美元,預計到 2034 年將以 4.9% 的複合年成長率成長至 4.973 億美元。這些用於穩定和復位骨折肋骨的系統隨著全球創傷相關損傷的持續增加而需求日益成長。車禍、運動傷害和跌倒等事故(尤其是老年人事故)增加了對可靠胸部創傷干預措施的需求。隨著醫療服務提供者優先考慮更快康復和減少術後併發症,對先進肋骨固定技術的關注度日益提高。醫院和創傷科正在投資微創系統,這些系統不僅可以最大限度地縮短手術時間,還可以改善病患的復原效果。增強型植入物設計,例如符合人體解剖學的骨板和低調鈦系統,正在提高手術精確度,同時減少疼痛和住院時間。

數位影像技術的進步與先進的手術器械相結合,在加速肋骨修復系統的推廣應用方面發揮著至關重要的作用。這些創新為外科醫生提供了更高的手術精準度和更佳的手術視覺效果,從而改善了患者的預後並縮短了康復時間。因此,肋骨骨折修復不僅在創傷護理中,而且在骨科和胸腔外科領域也正成為首選解決方案。在即時成像和改進的植入物設計的支持下,人們對微創技術的信心日益增強,進一步推動了市場擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.093億美元 |

| 預測值 | 4.973億美元 |

| 複合年成長率 | 4.9% |

2024年,前路鋼板系統市場規模達1.832億美元。其日益普及的原因是其解剖學造型,有助於最大程度地減少組織刺激並降低術後併發症的風險。對於需要更高舒適度或注重美觀的患者,此類植入物是首選。隨著外科醫生尋求兼顧功能性和舒適性的高效固定系統,前路鋼板在常規和急診手術中日益受到青睞。

2024年,鈦基系統市場佔了73.1%的佔有率,這主要歸功於其無與倫比的強度重量比。鈦金屬具有剛性,且不會增加硬體體積,從而支持肋骨在呼吸過程中的自然運動。其對胸腔結構的適應性以及久經考驗的機械一致性,有助於在整個癒合過程中有效保持肋骨的排列。鈦金屬卓越的生物相容性以及較低的免疫反應或發炎發生率,使其成為外科修復中安全的長期解決方案,並將繼續在肋骨骨折修復領域佔據主導地位。

由於胸部創傷病例高發生且醫療基礎設施先進,美國肋骨骨折修復系統市場在2024年的價值達到1.248億美元。機動車碰撞、老化相關的跌倒以及運動創傷等頻繁發生的損傷,推動了醫院和創傷中心對肋骨固定解決方案的需求。隨著3D影像系統和微創植入物等高階外科技術的廣泛應用,美國醫療機構已成為尖端肋骨固定技術的早期採用者。這種環境支持了鈦基精密工程植入物在各外科中心的持續整合,從而促進了全國市場的擴張。

該市場的主要參與者包括 Able Medical Devices、Acumed、Arthrex、Jeil Medical、強生、KLS Martin、美敦力、Neuro France Implants、Orthofix、OsteoMed、Selective Surgical、Smith & Nephew、Stryker、Waston Medical 和 Zimmer Biomet。該領域的知名公司正加緊研發創新、低調的植入物設計,以滿足外科醫生的偏好和患者特定的解剖學要求。

他們也強調研發產生物相容性和耐用性材料,例如鈦和混合合金。與創傷中心和教學醫院建立策略合作夥伴關係,有助於推動早期採用和基於回饋的產品改進。各公司正透過FDA和CE認證擴大其全球影響力,進而提升微創植入物在新興區域市場的可及性。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 胸部創傷發生率上升

- 手術固定系統的技術進步

- 門診和流動手術的偏好日益成長

- 新興市場醫療支出和基礎建設增加

- 產業陷阱與挑戰

- 手術和植入系統成本高昂

- 肋骨固定解決方案的認知度和可用性有限

- 市場機會

- 向創傷發生率高的滲透率較低的市場擴張

- 3D列印與個人化植入技術的融合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 專利分析

- 定價分析

- 依產品類型

- 按地區

- 差距分析

- 波特的分析

- PESTLE 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 前板系統

- 碟盤系統

第6章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 鈦

- 聚醚醚酮(PEEK)

- 其他材料

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 專科診所

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Able Medical Devices

- Acumed

- Arthrex

- Jeil Medical

- Johnson & Johnson

- KLS Martin

- Medtronic

- Neuro France Implants

- Orthofix

- OsteoMed

- Selective Surgical

- Smith & Nephew

- Stryker

- Waston Medical

- Zimmer Biomet

The Global Rib Fracture Repair Systems Market was valued at USD 309.3 million in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 497.3 million by 2034. These systems, designed to stabilize and realign fractured ribs, are seeing growing demand as trauma-related injuries continue to rise across the globe. Incidents stemming from vehicular accidents, sports-related injuries, and falls-particularly among the elderly-are increasing the need for reliable chest trauma interventions. As healthcare providers prioritize quicker recovery and reduced post-operative complications, the focus on advanced rib fixation techniques is intensifying. Hospitals and trauma units are investing in minimally invasive systems that not only minimize surgical duration but also improve patient recovery outcomes. Enhanced implant designs, such as anatomically shaped plates and low-profile titanium systems, are improving surgical precision while reducing pain and hospital stays.

Advancements in digital imaging technologies combined with state-of-the-art surgical instruments are playing a crucial role in accelerating the use of rib repair systems. These innovations provide surgeons with enhanced precision and better visualization during procedures, which leads to improved patient outcomes and shorter recovery times. As a result, rib fracture repair is becoming a preferred solution not only in trauma care but also within orthopedic and thoracic surgery units. The growing confidence in minimally invasive techniques, supported by real-time imaging and improved implant designs, is further driving market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $309.3 Million |

| Forecast Value | $497.3 Million |

| CAGR | 4.9% |

The anterior plate systems segment was valued at USD 183.2 million in 2024. Their growing popularity comes from their anatomical shaping, which helps minimize tissue irritation and reduce the chance of post-surgical complications. These implants are preferred in patients who require enhanced comfort or for those where aesthetics is a consideration. With surgeons seeking efficient fixation systems that balance functionality and comfort, anterior plates are increasingly selected for both routine and emergency procedures.

The titanium-based systems segment captured a 73.1% share in 2024, largely due to the material's unmatched strength-to-weight ratio. Titanium offers rigidity without excess hardware bulk, supporting the rib's natural motion during respiration. Its adaptability to the thoracic structure and proven mechanical consistency help maintain rib alignment effectively throughout the healing process. Titanium's exceptional biocompatibility and low likelihood of causing immune responses or inflammation make it a safe long-term solution in surgical repairs, fueling its continued dominance in rib fracture repair solutions.

United States Rib Fracture Repair Systems Market was valued at USD 124.8 million in 2024 due to its high rate of chest trauma cases and its advanced healthcare infrastructure. Frequent injuries caused by motor vehicle collisions, aging-related falls, and sports trauma are driving hospital and trauma center demand for rib fixation solutions. With the widespread adoption of high-end surgical technologies, including 3D imaging systems and minimally invasive implants, U.S. institutions are early adopters of cutting-edge rib stabilization technologies. This environment supports the continuous integration of titanium-based, precision-engineered implants throughout surgical centers, contributing to national market expansion.

Key players involved in the market include Able Medical Devices, Acumed, Arthrex, Jeil Medical, Johnson & Johnson, KLS Martin, Medtronic, Neuro France Implants, Orthofix, OsteoMed, Selective Surgical, Smith & Nephew, Stryker, Waston Medical, Zimmer Biomet. Prominent companies in this space are intensifying their focus on developing innovative, low-profile implant designs that meet both surgeon preferences and patient-specific anatomical requirements.

They are also emphasizing R&D to produce biocompatible and durable materials like titanium and hybrid alloys. Strategic partnerships with trauma centers and teaching hospitals help drive early adoption and feedback-driven product refinement. Firms are expanding their global footprint through FDA and CE approvals, enhancing access to minimally invasive implants in new regional markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chest trauma injuries

- 3.2.1.2 Technological advancements in surgical fixation systems

- 3.2.1.3 Growing preference for outpatient and ambulatory surgical procedures

- 3.2.1.4 Increased healthcare spending and infrastructure development in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical procedures and implant systems

- 3.2.2.2 Limited awareness and availability of rib fixation solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into underpenetrated markets with high trauma incidence

- 3.2.3.2 Integration of 3D printing and personalized implant technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anterior plate systems

- 5.3 U-plate systems

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Other materials

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profile

- 9.1 Able Medical Devices

- 9.2 Acumed

- 9.3 Arthrex

- 9.4 Jeil Medical

- 9.5 Johnson & Johnson

- 9.6 KLS Martin

- 9.7 Medtronic

- 9.8 Neuro France Implants

- 9.9 Orthofix

- 9.10 OsteoMed

- 9.11 Selective Surgical

- 9.12 Smith & Nephew

- 9.13 Stryker

- 9.14 Waston Medical

- 9.15 Zimmer Biomet