|

市場調查報告書

商品編碼

1773410

危險品包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hazmat Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

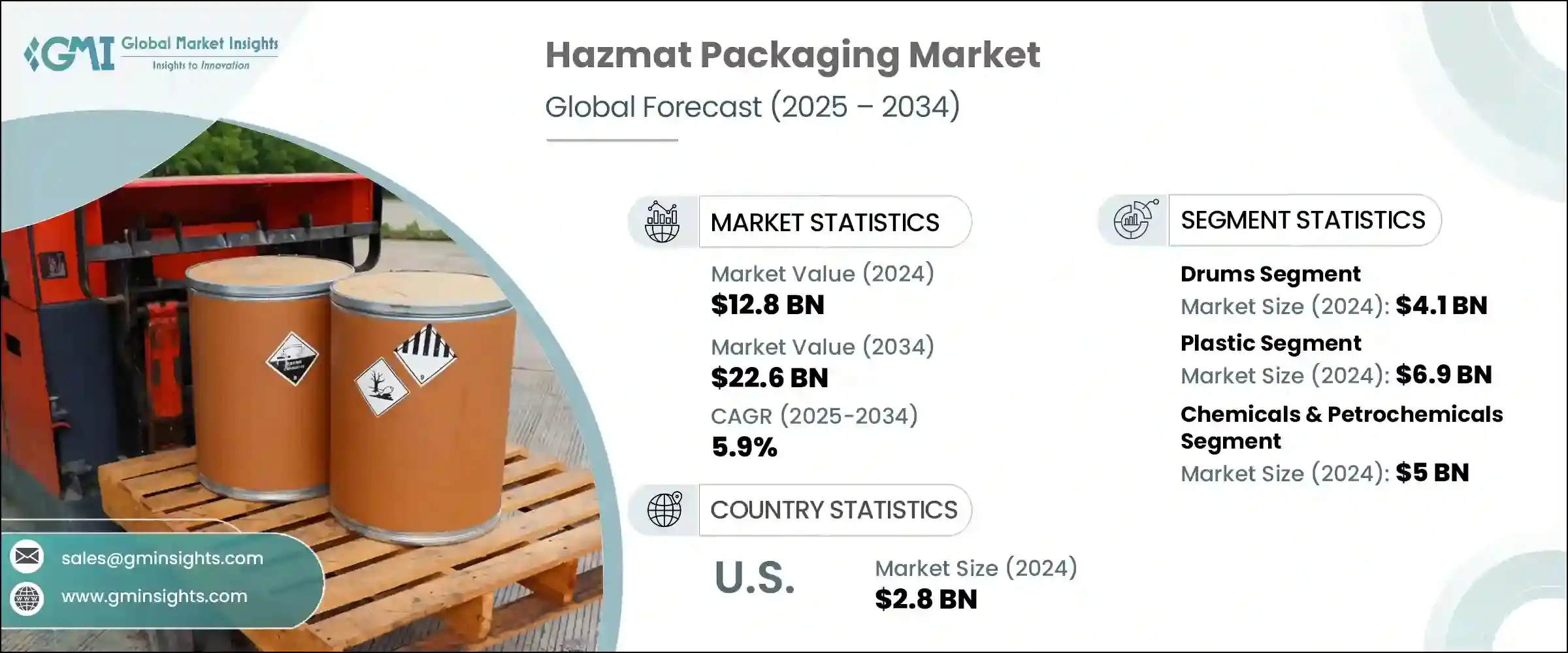

2024年,全球危險品包裝市場規模達128億美元,預計到2034年將以5.9%的複合年成長率成長,達到226億美元。這一穩定成長源於化學和製藥生產的不斷擴張,以及電子商務和跨境貿易的蓬勃發展。由於許多產品被歸類為易燃、有毒或腐蝕性產品,各行各業越來越依賴專用的危險物品包裝來滿足嚴格的儲存和運輸要求。美國職業安全與健康管理局(OSHA)、美國環保署(EPA)等監管機構以及國際機構對容器、標籤和運輸實施嚴格的標準,從而推動了市場更廣泛的採用。

包括生物製劑和疫苗在內的藥品,對能夠處理危險物質的溫控包裝解決方案提出了更高的需求。此外,電子商務通路的穩定發展也使危險物品的處理和運輸變得更加複雜。如今,線上平台為受管製商品的大宗和小批量訂單提供了便利,這加劇了對可靠、符合法規的包裝的需求,以確保安全交付並最大限度地降低運輸過程中的風險。這種轉變促使包裝製造商在設計能夠承受長途運輸、倉庫搬運和各種氣候條件且不影響監管標準的包裝時,將安全性和物流效率放在首位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 128億美元 |

| 預測值 | 226億美元 |

| 複合年成長率 | 5.9% |

2024年,桶裝容器市場產值達41億美元。這些容器對於油漆、化學品和油類等工業液體的安全運輸和儲存仍然至關重要。其耐用的結構、防洩漏和易於堆疊的特性使其成為多個行業重型應用的首選。日益嚴格的安全規程和政府強制標準進一步推動了桶裝容器生產中對合規材料(例如高級塑膠、纖維複合材料和鋼筋)的需求。

2024年,塑膠市場規模達69億美元,且需求成長動能強勁。塑膠輕質的特性顯著降低了運輸成本,而其耐化學性使其成為儲存腐蝕性或敏感物質的理想選擇。此外,塑膠可輕鬆適應各種容器類型,包括中型散裝容器(IBC)、罐裝容器和罐式容器,這確保了其在危險品處理中對靈活性、高效性和安全性有嚴格要求的行業中持續佔據重要地位。

2024年,美國危險物品包裝市場價值達28億美元。這一領先地位體現了墨西哥灣沿岸等地區化工和石化生產活動的強勁成長,以及蓬勃發展的製藥和生物技術行業對特種藥物和生物製劑安全包裝的需求。此外,製造業和醫療保健行業產生的大量危險廢物也使得對合規包裝的需求持續成長,以便其能夠安全地運輸至處理設施。

全球危險品包裝市場的主要參與者包括 HazmatPac、Greif, Inc.、Berlin Packaging、Label Master、Craters & Freighters、Air Sea Containers、Enpac、Mauser Packaging Solutions、CL Smith、Nefab Group、Schutz GmbH & Co. KGaA、FibreStar、LPSt、MJS Packag Group、Schutz GmbH & Co. KGaA、FibreStar、LPSPS. THIELMANN US LLC。領先的危險物品包裝公司正專注於產品創新,以滿足不斷變化的監管標準,例如開發模組化、防漏的桶裝系統和溫控容器。

他們也在材料科學方面進行投資,青睞輕質複合材料和耐腐蝕塑膠,以降低成本並提高耐用性。與化學、製藥和電子商務公司建立策略合作夥伴關係,使其能夠提供客製化解決方案並簽訂長期合約。在營運方面,製造商正在透過擴大關鍵地區的工廠來擴大生產規模,以提高交付速度和成本效益。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 化學和製藥產量不斷成長

- 電子商務與全球貿易擴張

- 醫療保健和製藥業的成長

- 嚴格的監管框架

- 包裝材料的技術進步

- 產業陷阱與挑戰

- 專業包裝成本高

- 環境問題與永續發展壓力

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 歷史價格分析(2021-2024)

- 價格趨勢促進因素

- 區域價格差異

- 價格預測(2025-2034年)

- 定價策略

- 新興商業模式

- 合規性要求

- 永續性措施

- 永續材料評估

- 碳足跡分析

- 循環經濟實施

- 永續性認證和標準

- 永續性投資報酬率分析

- 全球消費者情緒分析

- 專利分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 鼓

- 中型散裝容器(IBC)

- 桶

- 瓶子和罐子

- 盒子和紙箱

- 其他

第6章:市場估計與預測:按材料類型,2021 - 2034 年

- 主要趨勢

- 塑膠

- 高密度聚乙烯

- 低密度聚乙烯

- 聚丙烯

- PVC

- 其他

- 金屬

- 瓦楞

第7章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 化學品和石化產品

- 製藥

- 石油和天然氣

- 農業

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Air Sea Containers

- Berlin Packaging

- CL Smith

- Craters & Freighters

- Enpac

- FibreStar

- Greif, Inc.

- HazmatPac

- Label Master

- LPS Industries

- Mauser Packaging Solutions

- MJS Packaging

- Nefab Group

- Rhino Container, Inc.

- Schutz GmbH & Co. KGaA

- Sohner Kunststofftechnik GmbH

- THIELMANN US LLC

The Global Hazmat Packaging Market was valued at USD 12.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 22.6 billion by 2034. This steady growth stems from expanding chemical and pharmaceutical production, as well as surging ecommerce and cross-border trade. With many products classified as flammable, toxic, or corrosive, industries increasingly rely on purpose-built hazmat packaging to meet stringent storage and transport requirements. Regulatory agencies such as OSHA, the EPA, and international bodies enforce rigorous standards for containment, labeling, and shipping, prompting broader market adoption.

Pharmaceuticals, including biologics and vaccines, introduce demand for temperature-controlled packaging solutions capable of handling hazardous materials. Additionally, the steady rise of digital commerce channels has introduced greater complexity in the handling and transport of hazardous goods. Online platforms now facilitate bulk and small-quantity orders of regulated items, which has intensified the need for reliable, regulation-compliant packaging that ensures safe delivery and minimizes risk during transit. This shift is pushing packaging manufacturers to prioritize both safety and logistical efficiency by designing packaging that can endure long-distance shipping, warehouse handling, and varying climate conditions, without compromising regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $22.6 Billion |

| CAGR | 5.9% |

The drums segment generated USD 4.1 billion in 2024. These containers remain essential for the safe transport and storage of industrial liquids such as paints, chemicals, and oils. Their durable structure, leak resistance, and ease of stacking make them the preferred choice for heavy-duty applications across several sectors. Increasing safety protocols and government-mandated standards are further driving demand for compliant materials like high-grade plastics, fiber composites, and reinforced steel in drum production.

The plastic segment accounted USD 6.9 billion in 2024, and its demand shows no signs of slowing. Its lightweight nature significantly reduces freight costs, while its chemical resistance makes it ideal for storing corrosive or sensitive substances. Moreover, the adaptability of plastic into different container formats-including IBCs, canisters, and jerricans-ensures its continued relevance across industries that require flexibility, efficiency, and safety in hazardous material handling.

U.S. Hazmat Packaging Market was valued at USD 2.8 billion in 2024. This leadership reflects strong activity in chemical and petrochemical production-in regions like the Gulf Coast-as well as a booming pharmaceutical and biotech sector needing safe packaging for specialty drugs and biologics. Additionally, the high volume of hazardous waste generated by manufacturing and healthcare operations creates sustained demand for compliant packaging for safe transport to treatment facilities.

Key players in the Global Hazmat Packaging Market include HazmatPac, Greif, Inc., Berlin Packaging, Label Master, Craters & Freighters, Air Sea Containers, Enpac, Mauser Packaging Solutions, CL Smith, Nefab Group, Schutz GmbH & Co. KGaA, FibreStar, LPS Industries, MJS Packaging, Rhino Container, Inc., Sohner Kunststofftechnik GmbH, THIELMANN US LLC. Leading hazmat packaging firms are focusing on product innovation to meet evolving regulatory standards-developing modular, leak-proof drum systems and temperature-controlled containers.

They are also investing in materials science, favoring lightweight composites and corrosion-resistant plastics to reduce costs and enhance durability. Strategic partnerships with chemical, pharmaceutical, and e-commerce companies are enabling tailored solutions and long-term contracts. Operationally, manufacturers are scaling production by expanding facilities in key regions to improve delivery speed and cost efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Product type trends

- 2.2.3 Material type trends

- 2.2.4 End use industry trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising chemical & pharmaceutical production

- 3.2.1.2 E-commerce & global trade expansion

- 3.2.1.3 Growth in the healthcare & pharmaceutical sector

- 3.2.1.4 Stringent regulatory frameworks

- 3.2.1.5 Technological advancements in packaging materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of specialized packaging

- 3.2.2.2 Environmental concerns & sustainability pressures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability ROI analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Drums

- 5.3 Intermediate bulk containers (IBCs)

- 5.4 Pails

- 5.5 Bottles & jars

- 5.6 Boxes & cartons

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Plastics

- 6.2.1 HDPE

- 6.2.2 LDPE

- 6.2.3 PP

- 6.2.4 PVC

- 6.2.5 Others

- 6.3 Metal

- 6.4 Corrugated

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Chemicals & petrochemicals

- 7.3 Pharmaceuticals

- 7.4 Oil and gas

- 7.5 Agriculture

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Air Sea Containers

- 9.2 Berlin Packaging

- 9.3 CL Smith

- 9.4 Craters & Freighters

- 9.5 Enpac

- 9.6 FibreStar

- 9.7 Greif, Inc.

- 9.8 HazmatPac

- 9.9 Label Master

- 9.10 LPS Industries

- 9.11 Mauser Packaging Solutions

- 9.12 MJS Packaging

- 9.13 Nefab Group

- 9.14 Rhino Container, Inc.

- 9.15 Schutz GmbH & Co. KGaA

- 9.16 Sohner Kunststofftechnik GmbH

- 9.17 THIELMANN US LLC