|

市場調查報告書

商品編碼

1766371

光電逆變器市場機會、成長動力、產業趨勢分析及2025-2034年預測PV Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

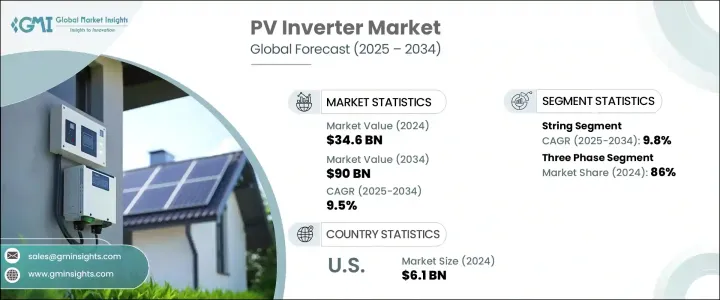

2024年,全球光電逆變器市場規模達346億美元,預計2034年將以9.5%的複合年成長率成長,達到900億美元。全球能源格局正在發生顯著轉變,再生能源日益受到重視。這項轉變正在加速高效能光電系統的普及,而逆變器如今已成為現代太陽能裝置的核心。隨著各國努力減少對化石燃料的依賴,光電逆變器正以更快的速度融入能源基礎設施。這些設備不僅能將直流電轉換為交流電,還能提高系統可靠性和能源產量,使其成為各種應用中不可或缺的一部分。

對永續性的日益關注,加上有利的能源政策和公共和私營部門的支持性投資,正在為光伏逆變器的部署創造有利環境。旨在減少碳排放和最佳化能源消耗的法規正在加強向先進太陽能解決方案的轉變。此外,受規模經濟和製造流程穩定改善的推動,太陽能技術成本持續下降,使光電系統更具經濟可行性。這種經濟實惠的優勢為那些太陽能資源豐富但在獲取傳統電力基礎設施方面歷來面臨挑戰的地區帶來了機會。分散式能源發電的擴張進一步刺激了對能夠在併網和離網環境中無縫運行的逆變器的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 346億美元 |

| 預測值 | 900億美元 |

| 複合年成長率 | 9.5% |

電網現代化進程也進一步增強了先進逆變器的作用。隨著智慧能源網路的發展,對能夠超越基本功率轉換的逆變器的需求日益成長。遠端診斷、即時監控、電壓調節和頻率支援等功能正成為下一代設備的標準配置。這些功能使其能夠更好地融入智慧電網框架,並幫助公用事業公司在再生能源輸入波動的情況下保持電網穩定。隨著數位化在能源領域的蓬勃發展,配備資料分析和人工智慧驅動能源管理功能的光伏逆變器對於高效配電和性能最佳化至關重要。

在各類產品中,串式逆變器的需求日益成長,預計2034年複合年成長率將達到9.8%。其受歡迎程度源自於其可擴展性、經濟實惠和易於維護的特性。由於其模組化架構有助於快速識別故障並簡化系統升級,因此串式逆變器在住宅和商業領域中被廣泛採用。此外,串式逆變器與儲能單元的兼容性不斷增強,也使其在混合安裝中的吸引力不斷提升。高效的熱管理和緊湊的設計進一步推動了其市場佔有率的提升,尤其是在空間受限的項目中。

光電逆變器市場按相數細分為單相和三相系統。 2024年,三相逆變器佔據了整體市場的86%。這種主導地位可以歸因於新興經濟體工業化和城市化的快速發展,這些國家對更高容量、更多樣化的能源系統的需求。三相逆變器運作效率高,更適合在商業和公用事業規模的應用中大規模部署,因為這些應用對電力的需求巨大且穩定。

截至2024年,北美佔全球光電逆變器市場的18.1%。在該地區,美國繼續扮演重要角色,其市場價值從2022年的48億美元成長至2024年的61億美元。美國重視分散式能源發電,並得到聯邦和州級政府的強力激勵,創造了有利於住宅和商業屋頂太陽能發展的環境。同時,國家電網基礎設施的持續升級正在推動智慧逆變器的整合。隨著用戶側儲能解決方案的興起,尤其是在注重能源彈性的各州,光電逆變器的部署將進一步成長。

製造商正大力投入研發,開發一系列滿足住宅、商業和公用事業規模客戶特定需求的逆變器產品組合。從混合動力車型到專為工業用途設計的高容量逆變器,各家公司都在不斷推出創新產品,以提升性能、提高能源產量並符合全球永續發展目標。此外,將智慧技術融入產品也成為一種顯著趨勢,包括數位介面、雲端連接和預測性維護功能。這些進步不僅提升了使用者體驗,還能讓營運商更深入了解能源使用和系統健康。

為了加強全球佈局,市場參與者正在採取多種策略組合。這些策略包括進入太陽能潛力巨大的新地區、建立聯盟以增強服務能力,以及透過併購來利用新興技術。數位化基礎設施和基於人工智慧的監控工具日益重要,促使利害關係人將智慧功能融入其中,從而在基本能源轉換之外創造更多價值。隨著全球太陽能格局的日趨成熟,這些全面的策略將有助於企業保持競爭力,同時滿足消費者、企業和公用事業公司不斷變化的能源需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率

- 戰略儀表板

- 策略舉措

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依產品,2021 - 2034

- 主要趨勢

- 細繩

- 微

- 中央

第6章:市場規模及預測:依階段,2021 - 2034

- 主要趨勢

- 單相

- 三相

第7章:市場規模及預測:依連結性,2021 - 2034

- 主要趨勢

- 獨立

- 在電網上

第8章:市場規模及預測:依標稱輸出功率,2021 - 2034

- 主要趨勢

- ≤0.5千瓦

- 0.5 - 3 千瓦

- 3 - 33 千瓦

- 33 - 110 千瓦

- > 110 千瓦

第9章:市場規模及預測:依標稱輸出電壓,2021 - 2034

- 主要趨勢

- ≤ 230 伏

- 230 - 400 伏

- 400 - 600 伏

- > 600 伏

第 10 章:市場規模與預測:按應用,2021 - 2034 年

- 主要趨勢

- 住宅

- 商業和工業

- 公用事業

第 11 章:市場規模與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 義大利

- 波蘭

- 荷蘭

- 奧地利

- 英國

- 法國

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

第12章:公司簡介

- Altenergy Power System

- Canadian Solar

- Darfon Electronics

- Delta Electronics

- Eaton

- Enphase Energy

- Fimer Group

- Fronius International

- General Electric

- Ginlong Technologies

- GoodWe

- Growatt New Energy

- Huawei Technologies

- Panasonic Corporation

- Schneider Electric

- Siemens

- Sineng Electric

- SMA Solar Technology

- SolarEdge Technologies

- Sungrow

- Tabuchi Electric

- TMEIC

The Global PV Inverter Market was valued at USD 34.6 billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 90 billion by 2034. The global energy landscape is undergoing a notable transformation, with increasing emphasis on renewable power sources. This shift is accelerating the adoption of efficient photovoltaic systems, and inverters are now central to modern solar installations. As countries seek to reduce their dependence on fossil fuels, PV inverters are being integrated into energy infrastructure at a faster pace. These devices not only convert DC to AC power but also enhance system reliability and energy yield, making them indispensable across various applications.

The growing focus on sustainability, combined with favorable energy policies and supportive investment from the public and private sectors, is creating a conducive environment for PV inverter deployment. Regulations aimed at cutting carbon emissions and optimizing energy consumption are reinforcing the shift toward advanced solar solutions. Moreover, ongoing declines in solar technology costs-driven by economies of scale and steady improvements in manufacturing-are making PV systems more financially viable. This affordability is opening up opportunities in regions that are rich in solar resources but have historically faced challenges in accessing conventional power infrastructure. The expansion of distributed energy generation further supports the demand for inverters capable of operating seamlessly across grid-connected and off-grid setups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.6 Billion |

| Forecast Value | $90 Billion |

| CAGR | 9.5% |

Modernization efforts within power grids are also amplifying the role of advanced inverters. With the evolution of intelligent energy networks, there is an increased need for inverters that can perform beyond basic power conversion. Features such as remote diagnostics, real-time monitoring, voltage regulation, and frequency support are becoming standard in next-generation devices. These functionalities enable better integration into smart grid frameworks and help utilities maintain grid stability amid fluctuating renewable power inputs. As digitalization gains traction across the energy sector, PV inverters equipped with data analytics and AI-driven energy management capabilities are proving vital for efficient power distribution and performance optimization.

Among the different product types, string inverters are experiencing heightened demand, with expectations of growing at a CAGR of 9.8% through 2034. Their popularity stems from their scalability, affordability, and ease of maintenance. These systems are widely adopted in both residential and commercial sectors, as their modular architecture facilitates quick fault identification and simplified system upgrades. Additionally, the increasing compatibility of string inverters with energy storage units has broadened their appeal across hybrid installations. Their efficient thermal management and compact designs further contribute to their rising market share, especially in space-constrained projects.

The PV inverter market is segmented by phase into single-phase and three-phase systems. In 2024, three-phase inverters accounted for 86% of the overall market. This dominance can be attributed to the rapid pace of industrialization and urban development in emerging economies, which demand higher-capacity and more versatile energy systems. Three-phase inverters offer operational efficiency and are better suited for large-scale deployments in commercial and utility-scale applications, where power requirements are substantial and consistent.

North America, as of 2024, represented 18.1% of the global PV inverter market. Within this region, the United States continues to be a key contributor, with market values rising from USD 4.8 billion in 2022 to USD 6.1 billion in 2024. The country's emphasis on decentralized energy generation, supported by robust federal and state-level incentives, has fostered an environment conducive to rooftop solar growth in both residential and commercial settings. At the same time, ongoing upgrades to the national grid infrastructure are driving the integration of smart inverters. With the rise of behind-the-meter storage solutions, particularly in states focused on energy resilience, the deployment of PV inverters is set to grow further.

Manufacturers are investing heavily in R&D to develop a broad portfolio of inverters tailored to specific customer needs across residential, commercial, and utility-scale sectors. From hybrid models to high-capacity inverters designed for industrial use, companies are rolling out innovations that improve performance, enhance energy yield, and align with global sustainability goals. There is also a noticeable trend toward embedding intelligent technologies into products, including digital interfaces, cloud connectivity, and predictive maintenance capabilities. These advancements not only improve user experience but also offer operators deeper insights into energy usage and system health.

To strengthen their global footprint, market participants are leveraging a combination of strategies. These include entering new geographic regions with high solar potential, forming alliances to enhance service offerings, and pursuing mergers to tap into emerging technologies. The increasing relevance of digital infrastructure and AI-based monitoring tools is leading stakeholders to incorporate smart features that add value beyond basic energy conversion. As the global solar landscape matures, these comprehensive strategies will help companies remain competitive while addressing the evolving energy demands of consumers, businesses, and utilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 String

- 5.3 Micro

- 5.4 Central

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Connectivity, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 Standalone

- 7.3 On grid

Chapter 8 Market Size and Forecast, By Nominal Output Power, 2021 - 2034 (USD Billion & MW)

- 8.1 Key trends

- 8.2 ≤ 0.5 kW

- 8.3 0.5 - 3 kW

- 8.4 3 - 33 kW

- 8.5 33 - 110 kW

- 8.6 > 110 kW

Chapter 9 Market Size and Forecast, By Nominal Output Voltage, 2021 - 2034 (USD Billion & MW)

- 9.1 Key trends

- 9.2 ≤ 230 V

- 9.3 230 - 400 V

- 9.4 400 - 600 V

- 9.5 > 600 V

Chapter 10 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion & MW)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial & industrial

- 10.4 Utility

Chapter 11 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MW)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 Italy

- 11.3.3 Poland

- 11.3.4 Netherlands

- 11.3.5 Austria

- 11.3.6 UK

- 11.3.7 France

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Australia

- 11.4.3 India

- 11.4.4 Japan

- 11.4.5 South Korea

- 11.5 Middle East & Africa

- 11.5.1 Israel

- 11.5.2 Saudi Arabia

- 11.5.3 UAE

- 11.5.4 South Africa

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Mexico

- 11.6.3 Chile

Chapter 12 Company Profiles

- 12.1 Altenergy Power System

- 12.2 Canadian Solar

- 12.3 Darfon Electronics

- 12.4 Delta Electronics

- 12.5 Eaton

- 12.6 Enphase Energy

- 12.7 Fimer Group

- 12.8 Fronius International

- 12.9 General Electric

- 12.10 Ginlong Technologies

- 12.11 GoodWe

- 12.12 Growatt New Energy

- 12.13 Huawei Technologies

- 12.14 Panasonic Corporation

- 12.15 Schneider Electric

- 12.16 Siemens

- 12.17 Sineng Electric

- 12.18 SMA Solar Technology

- 12.19 SolarEdge Technologies

- 12.20 Sungrow

- 12.21 Tabuchi Electric

- 12.22 TMEIC

太陽能逆變器外殼市場:按逆變器類型、外殼材料、冷卻方式、安裝方式和應用分類 - 全球預測(2026-2032 年)

太陽能逆變器外殼市場:按逆變器類型、外殼材料、冷卻方式、安裝方式和應用分類 - 全球預測(2026-2032 年) 住宅太陽能光電逆變器市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、相數、連接方式、地區及競爭格局分類,2021-2031年預測)

住宅太陽能光電逆變器市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、相數、連接方式、地區及競爭格局分類,2021-2031年預測) 太陽能逆變器市場預測至2032年:按產品類型、相數、連接方式、應用、最終用戶和地區分類的全球分析

太陽能逆變器市場預測至2032年:按產品類型、相數、連接方式、應用、最終用戶和地區分類的全球分析 中央逆變器市場-2025年至2030年預測

中央逆變器市場-2025年至2030年預測 智慧逆變器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)光伏逆變器市場按產品、組件、類型、相數、輸出功率、銷售管道和應用分類-2025-2032年全球預測

智慧逆變器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)光伏逆變器市場按產品、組件、類型、相數、輸出功率、銷售管道和應用分類-2025-2032年全球預測 2025年全球光電逆變器市場現狀2032 年智慧逆變器市場預測:按類型、連接性、應用、最終用戶和地區進行的全球分析太陽能逆變器市場(按逆變器類型、相型、額定功率、系統類型、輸出電壓、應用、安裝類型和銷售管道)——2025-2030 年全球預測

2025年全球光電逆變器市場現狀2032 年智慧逆變器市場預測:按類型、連接性、應用、最終用戶和地區進行的全球分析太陽能逆變器市場(按逆變器類型、相型、額定功率、系統類型、輸出電壓、應用、安裝類型和銷售管道)——2025-2030 年全球預測 全球商業和工業光伏逆變器市場

全球商業和工業光伏逆變器市場