|

市場調查報告書

商品編碼

1766347

鉛酸電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lead Acid Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

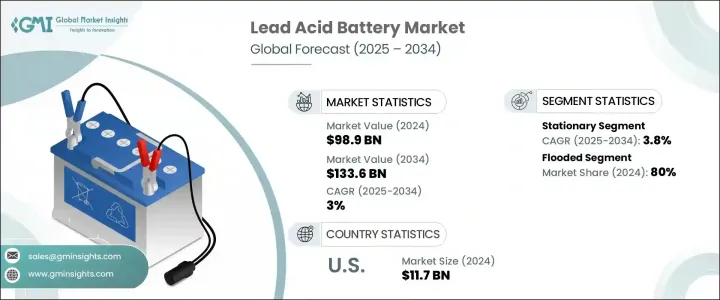

2024年,全球鉛酸電池市場規模達989億美元,預計2034年將以3%的複合年成長率成長,達到1,336億美元。這項穩定成長得益於增強型富液電池和吸收性玻璃纖維隔板(AGM)技術的持續創新,這些技術提升了啟動停止系統和其他汽車輔助功能的效率。碳增強添加劑和鈣合金板柵等電極材料的現代進步,顯著提高了導電性、增強了放電能力,並延長了電池的整體壽命。這些改進正在推動電池在工業、電信和能源領域的更廣泛應用,因為在這些領域,極端溫度下的穩定性能至關重要。

隨著新興市場對電池生產設施的投資不斷增加,鉛酸電池技術的普及程度不斷提高。這些電池擴大與再生能源系統整合,成為平衡供需的可靠儲能解決方案,尤其是在離網或偏遠地區。其成本效益、可回收性和長期的良好業績使其成為工業和住宅儲能的環保解決方案。此外,發展中國家汽車製造業的蓬勃發展也推高了對啟動、照明和點火 (SLI) 電池的需求,因為它們仍然是內燃機驅動車的首選。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 989億美元 |

| 預測值 | 1336億美元 |

| 複合年成長率 | 3% |

預計到2034年,固定式鉛酸蓄電池市場的複合年成長率將達到3.8%,這得益於資料密集型環境中對不間斷穩定電源日益成長的需求。數位基礎設施的快速發展以及5G網路的加速部署,正在催生對經濟高效且可靠的儲能解決方案的強勁需求。這些電池在支援電信網路、緊急系統、資料中心和其他關鍵任務運作方面發揮著至關重要的作用,確保在停電或電網波動期間持續供電。它們能夠提供長時間備用電源、維護要求低以及與各種備用系統的兼容性,這些特性使其在市場上持續保持競爭力。

預計到2034年,VRLA(閥控式鉛酸電池)市場規模將達到250億美元,這得益於其在工業設備和重要設施中的廣泛應用。這類電池因其密封、免維護的設計和出色的電量保持能力而備受青睞,非常適合封閉式或受限場所的安裝。 VRLA電池在高壓條件下表現出色,在醫療保健、IT基礎設施和能源管理等對高正常運行時間要求的行業中,正變得不可或缺。隨著全球各產業擴大採用自動化和遠端監控系統,VRLA電池因其高效且具有故障保護功能的備用電源,其需求也持續攀升。

2024年,美國鉛酸電池市場規模達117億美元,顯示出強勁的需求,這主要得益於其在汽車、工業機械、再生能源儲存和緊急電源系統等領域的廣泛應用。鉛酸電池在價格、可靠性和可回收性方面無與倫比的平衡性支撐了這一成長。隨著新的環境績效基準訂定,監管力度也隨之加強,對電池製造商各個生產環節的鉛排放進行了更嚴格的控制。

積極參與鉛酸電池市場的值得注意的公司包括 GS Yuasa International、Furukawa Battery、Zibo Torch Energy、East Penn Manufacturing Company、Amara Raja Group、EnerSys、Leoch International Technology、Narada Power、MUTLU、BB Battery、Clarios、NorthStar Battery、Pattery、Y文化YY東西、CNNer、Pattery。 Battery、Shandong Sacred Sun Power Sources 和 Chaowei Power Holdings。鉛酸電池市場公司採用的關鍵策略是透過技術升級和設計改進來加強其產品組合。許多公司正在投資研發支援快速充電、延長使用壽命和提高能量密度的高性能電池。該公司還專注於在能源和汽車需求不斷成長的地區擴大製造足跡。策略夥伴關係、合併和合資企業是增加區域滲透率和市場佔有率的常用方法。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 戰略儀表板

- 策略舉措

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 固定式

- 電信

- UPS

- 控制和開關設備

- 其他

- 動機

- 速連

- 汽車

- 摩托車

第6章:市場規模及預測:依建築類型,2021 - 2034 年

- 主要趨勢

- 淹沒

- 閥控鉛酸蓄電池

- 年度股東大會

- 凝膠

第7章:市場規模及預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 義大利

- 西班牙

- 奧地利

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 泰國

- 菲律賓

- 越南

- 新加坡

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 埃及

- 土耳其

- 摩洛哥

- 南非

- 奈及利亞

- 阿爾及利亞

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 智利

第9章:公司簡介

- Amara Raja Group

- BB Battery

- C&D Technologies

- Chaowei Power Holdings

- Clarios

- Crown Battery

- East Penn Manufacturing Company

- EnerSys

- Exide Industries

- First National Battery

- Furukawa Battery

- GS Yuasa International

- HOPPECKE Battery

- Leoch International Technology

- Middle East Battery

- MUTLU

- Narada Power

- NorthStar Battery

- Shandong Sacred Sun Power Sources

- Zibo Torch Energy

The Global Lead Acid Battery Market was valued at USD 98.9 billion in 2024 and is estimated to grow at a CAGR of 3% to reach USD 133.6 billion by 2034. This steady growth is fueled by ongoing innovations in enhanced flooded batteries and absorbent glass mat (AGM) technology, which offer improved efficiency for start-stop systems and other auxiliary automotive functions. Modern advancements in electrode materials, such as carbon-enhanced additives and calcium-alloy grids, have significantly boosted conductivity, enhanced discharge capabilities, and extended overall battery life. These improvements are driving broader adoption across industrial, telecom, and energy sectors, where consistent performance in extreme temperatures is essential.

As investment into battery production facilities increases across emerging markets, accessibility to lead acid battery technology continues to improve. These batteries are increasingly integrated with renewable energy systems, serving as reliable storage solutions to balance supply and demand, especially in off-grid or remote settings. Their cost-effectiveness, recyclability, and long-standing track record make them an eco-friendly solution for both industrial and residential energy storage. Moreover, rising vehicle manufacturing in developing countries is pushing up demand for starting, lighting, and ignition (SLI) batteries, as they remain the preferred choice for internal combustion engine-powered vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $98.9 Billion |

| Forecast Value | $133.6 Billion |

| CAGR | 3% |

The stationary lead acid battery segment is expected to grow at a CAGR of 3.8% through 2034, driven by the increasing demand for uninterrupted and stable power supply across data-intensive environments. The rapid development of digital infrastructure, along with the accelerated rollout of 5G networks, is creating strong demand for cost-effective and reliable energy storage solutions. These batteries play a crucial role in supporting telecommunication networks, emergency systems, data centers, and other mission-critical operations by ensuring consistent power availability during outages or grid fluctuations. Their ability to provide long-duration backup, low maintenance requirements, and compatibility with diverse backup systems contributes to their continued market relevance.

The VRLA (valve-regulated lead acid) battery segment is projected to reach USD 25 billion by 2034, fueled by widespread integration in industrial setups and essential facilities. These batteries are favored for their sealed, maintenance-free design and excellent charge retention, which make them suitable for enclosed or limited-access installations. With their track record of delivering reliable performance under high-stress conditions, VRLA batteries are becoming indispensable in industries that demand high uptime, such as healthcare, IT infrastructure, and energy management. As global industries increasingly adopt automation and remote monitoring systems, the demand for VRLA batteries continues to climb due to their ability to deliver efficient and fail-safe power backup.

United States Lead Acid Battery Market generated USD 11.7 billion in 2024, showing robust demand driven by widespread use in automobiles, industrial machinery, renewable energy storage, and emergency power systems. This growth is supported by the unmatched balance of affordability, reliability, and recyclability that lead acid batteries offer. Regulatory oversight has also intensified, as new environmental performance benchmarks have been introduced for battery manufacturers, placing tighter control over lead emissions across various production processes.

Noteworthy companies actively participating in the Lead Acid Battery Market include GS Yuasa International, Furukawa Battery, Zibo Torch Energy, East Penn Manufacturing Company, Amara Raja Group, EnerSys, Leoch International Technology, Narada Power, MUTLU, B.B. Battery, Clarios, NorthStar Battery, Exide Industries, First National Battery, Middle East Battery, C&D Technologies, HOPPECKE Battery, Crown Battery, Shandong Sacred Sun Power Sources, and Chaowei Power Holdings. Key strategies adopted by companies in the lead acid battery market center on strengthening their product portfolios through technological upgrades and design improvements. Many firms are investing in R&D to develop high-performance batteries that support fast charging, extended lifecycle, and enhanced energy density. Companies are also focusing on expanding their manufacturing footprints in regions with growing energy and automotive demands. Strategic partnerships, mergers, and joint ventures are common approaches to increase regional penetration and market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Stationary

- 5.2.1 Telecommunications

- 5.2.2 UPS

- 5.2.3 Control & switchgear

- 5.2.4 Others

- 5.3 Motive

- 5.4 SLI

- 5.4.1 Automobiles

- 5.4.2 Motorcycles

Chapter 6 Market Size and Forecast, By Construction, 2021 - 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Flooded

- 6.3 VRLA

- 6.3.1 AGM

- 6.3.2 GEL

Chapter 7 Market Size and Forecast, By Sales Channel, 2021 - 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Austria

- 8.3.8 Netherlands

- 8.3.9 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Thailand

- 8.4.9 Philippines

- 8.4.10 Vietnam

- 8.4.11 Singapore

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Iran

- 8.5.4 Egypt

- 8.5.5 Turkey

- 8.5.6 Morocco

- 8.5.7 South Africa

- 8.5.8 Nigeria

- 8.5.9 Algeria

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Mexico

- 8.6.4 Chile

Chapter 9 Company Profiles

- 9.1 Amara Raja Group

- 9.2 B.B. Battery

- 9.3 C&D Technologies

- 9.4 Chaowei Power Holdings

- 9.5 Clarios

- 9.6 Crown Battery

- 9.7 East Penn Manufacturing Company

- 9.8 EnerSys

- 9.9 Exide Industries

- 9.10 First National Battery

- 9.11 Furukawa Battery

- 9.12 GS Yuasa International

- 9.13 HOPPECKE Battery

- 9.14 Leoch International Technology

- 9.15 Middle East Battery

- 9.16 MUTLU

- 9.17 Narada Power

- 9.18 NorthStar Battery

- 9.19 Shandong Sacred Sun Power Sources

- 9.20 Zibo Torch Energy

鉛酸蓄電池市場規模、佔有率及成長分析(按技術、類型、製造方法、最終用戶和地區分類)-2026-2033年產業預測

鉛酸蓄電池市場規模、佔有率及成長分析(按技術、類型、製造方法、最終用戶和地區分類)-2026-2033年產業預測 2025年全球固定式鉛酸蓄電池市場報告

2025年全球固定式鉛酸蓄電池市場報告 全球鉛酸蓄電池市場:依類型、應用和地區劃分-市場規模、產業趨勢、機會分析及預測(2025-2033 年)

全球鉛酸蓄電池市場:依類型、應用和地區劃分-市場規模、產業趨勢、機會分析及預測(2025-2033 年) VRLA電池:全球市佔率和排名、總收入和需求預測(2025-2031年)

VRLA電池:全球市佔率和排名、總收入和需求預測(2025-2031年) 按循環類型、銷售管道和應用分類的先進鉛酸蓄電池市場-2025-2032年全球預測鉛酸蓄電池市場按類型、電壓範圍、技術、分銷類型和最終用戶分類-全球預測,2025-2032年2025年全球先進鉛酸電池市場報告

按循環類型、銷售管道和應用分類的先進鉛酸蓄電池市場-2025-2032年全球預測鉛酸蓄電池市場按類型、電壓範圍、技術、分銷類型和最終用戶分類-全球預測,2025-2032年2025年全球先進鉛酸電池市場報告 2025-2029年全球工業用鉛酸電池市場

2025-2029年全球工業用鉛酸電池市場 管狀電池市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、地區和競爭細分,2020-2030 年)

管狀電池市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、地區和競爭細分,2020-2030 年) AGM VRLA 電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

AGM VRLA 電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測