|

市場調查報告書

商品編碼

1766251

車輛聲音合成技術市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Vehicle Sound Synthesis Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

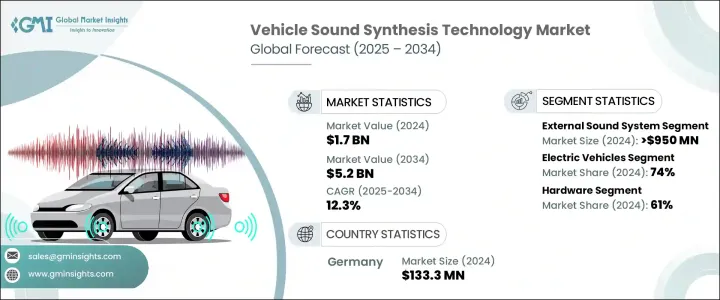

2024 年全球車輛聲音合成技術市場價值為 17 億美元,預計到 2034 年將以 12.3% 的複合年成長率成長,達到 52 億美元。電動和混合動力汽車的廣泛採用在推動市場成長方面發揮著重要作用。電動車 (EV) 由於採用電動馬達而極其安靜,這為車廂舒適度提供了優勢。然而,這種安靜也對行人構成風險,特別是老年人和殘疾人,因為他們可能聽不到車輛靠近。因此,聲學車輛警報系統 (AVAS) 現在在美國、歐盟、日本和中國等多個地區都是強制要求的,用於在低速行駛時產生人工聲音並提醒行人電動車的存在。全球電動車產量的激增進一步刺激了對這些車輛聲音合成系統的需求。

汽車製造商也正在利用聲音設計來提升品牌形象,並與客戶建立情感連結。車輛聲音合成技術已超越安全範疇,如今在品牌塑造和豐富電動車感官體驗方面發揮關鍵作用。許多汽車製造商正在與聲音設計師合作,為他們的車輛開發獨特的音訊配置,從類似引擎的轟鳴聲到舒緩的旋律,這些都有助於增強品牌聯想。這一趨勢正在幫助拓展車輛聲音合成技術的應用範圍。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 17億美元 |

| 預測值 | 52億美元 |

| 複合年成長率 | 12.3% |

2024年,外部音響系統市值達9.5億美元。隨著自動駕駛系統的進步和共享經濟模式的普及,外部音響對於人機互動的需求日益重要。無人駕駛汽車(例如自動駕駛汽車)通常依靠聲音合成來提醒行人,並用合成聲音取代傳統的喇叭。這種必要性使得外部音響系統成為汽車中至關重要的創收功能,製造商投入了大量研發和法律資源來遵守監管標準。由於這些系統是法律強制要求的,汽車製造商正在增加對量產的投資,使其價格更實惠、普及程度更高。

2024年,電動車領域佔據市場主導地位,佔74%的佔有率,預計在預測期內將大幅成長。純電動車 (BEV) 無需內燃機,因此本質上噪音較小,對行人構成安全隱患。為了降低這一風險,BEV 高度依賴 AVAS 技術來產生人工引擎聲音,確保行人更安全的駕駛條件。作為車輛聲音合成技術最先進的細分市場,隨著全球電動車需求的不斷成長,預計該細分市場將繼續成長。

2024年,德國車輛聲音合成技術市場佔21%的市場佔有率,產值達1.333億美元。德國在電動車聲音合成系統的應用方面一直處於領先地位,許多製造商引領潮流。這些公司不僅遵守安全標準,還運用聲音設計來更有效地推廣其電動車。德國強大的汽車工業,以及博世、大陸和海拉等主要參與者,加速了AVAS系統在歐洲的廣泛應用,使其在短時間內實現了標準化和可擴展性。

車輛聲音合成技術市場的主要公司包括 Aptiv、通用汽車、特斯拉、哈曼國際、電裝、大陸集團、現代汽車公司、大眾汽車、德爾福科技和寶馬集團。在車輛聲音合成市場,各公司專注於開發先進的聲音設計和聲學解決方案,以增強安全性、品牌形像以及與客戶的情感連結。許多製造商已經與聲音設計師和作曲家建立了戰略合作關係,為他們的車輛創建客製化的音訊檔案。此外,他們正在增加研發投入,以確保遵守不斷變化的法規。與關鍵一級供應商在硬體和控制系統開發方面的合作也有助於公司擴展其能力。此外,正在採用大規模生產策略,以使聲音合成系統更經濟實惠且更易於消費者使用。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 電動和混合動力車的普及率不斷上升

- 政府有關行人安全的規定

- 數位聲音設計的技術進步

- 車內聲學體驗的需求日益成長

- 產業陷阱與挑戰

- 與傳統平台和電動車轉換的整合

- 小型原始設備製造商和二線市場的認知度有限

- 市場機會

- 電動和混合動力汽車的擴張

- 行人安全監理規定

- 對可定製品牌聲音特徵的需求

- 與先進車輛架構整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 內部音響系統

- 外部音響系統

第6章:市場估計與預測:以推進方式,2021 - 2034 年

- 主要趨勢

- 內燃機(ICE)

- 電動車(EV)

- 純電動車(BEV)

- 插電式混合動力車(PHEV)

- 混合動力電動車(HEV)

第7章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 聲音產生器/模組

- 揚聲器/換能器

- 擴大機

- 控制器/ECU

- 軟體

- 聲音設計和設定檔軟體

- 聲音合成演算法

- 車輛整合軟體

- 聲學模擬和調音工具

- 服務

- 部署與整合

- 諮詢

- 支援與維護

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- 原始設備製造商

- 售後市場

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 11 章:公司簡介

- Aptiv

- Audi

- BMW Group

- Brigade Electronics

- BYD Auto Co.

- Continental

- Delphi Technologies

- Denso Corporation

- ECCO Safety Group

- Ford Motor Company

- General Motors Company

- Harman International

- Honda Motor Co.

- Hyundai Motor Company

- KUFATEC

- Mando Hella Electronics Corp

- Nissan Motor Corporation

- STMicroelectronics

- Tesla

- Volkswagen

The Global Vehicle Sound Synthesis Technology Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 5.2 billion by 2034. The widespread adoption of electric and hybrid vehicles plays a major role in driving market growth. Electric vehicles (EVs) are incredibly quiet due to their electric motor, which provides an advantage in cabin comfort. However, this silence also poses a risk to pedestrians, particularly the elderly and disabled, as they may not hear the vehicle approaching. As a result, Acoustic Vehicle Alerting Systems (AVAS) are now mandatory in several regions, including the US, EU, Japan, and China, to generate artificial sounds at low speeds and alert pedestrians of an EV's presence. The surge in global EV production further boosts the demand for these vehicle sound synthesis systems.

Automotive manufacturers are also using sound design to enhance brand identity and create emotional connections with customers. Vehicle sound synthesis has evolved beyond safety and now plays a key role in branding and enriching the sensory experience of electric vehicles. Many car manufacturers are working with sound designers to develop unique audio profiles for their vehicles, ranging from engine-like roars to calming melodies, which also serve to strengthen brand association. This trend is helping expand the scope of vehicle sound synthesis technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 12.3% |

The external sound system segment was valued at USD 950 million in 2024. As autonomous driving systems progress and the shared economy model gains ground, the need for exterior sounds is becoming more critical for human-machine interactions. Vehicles that lack a driver, such as self-driving cars, often rely on sound synthesis to alert pedestrians, replacing the traditional horn with synthetic sounds. This necessity has made external sound systems a crucial, revenue-generating feature in vehicles, with manufacturers dedicating significant research, development, and legal resources to comply with regulatory standards. Since these systems are legally required, automakers are increasingly investing in mass production, making them more affordable and widely available.

The electric vehicle segment dominated the market in 2024, capturing a 74% share, and it is expected to grow significantly during the forecast period. Battery Electric Vehicles (BEVs) operate without an internal combustion engine and are therefore silent by nature, posing a safety concern for pedestrians. To mitigate this risk, BEVs rely heavily on AVAS technology to produce artificial engine sounds, ensuring safer driving conditions for pedestrians. This market segment, which is the most advanced adopter of vehicle sound synthesis, is expected to see continued growth as the demand for EVs expands worldwide.

Germany Vehicle Sound Synthesis Technology Market held a 21% share in 2024 and generated USD 133.3 million. The country has been at the forefront of adopting sound synthesis systems for electric vehicles, with many manufacturers leading the charge. Not only do these companies comply with safety standards, but they also use sound design to market their electric vehicles more effectively. Germany's strong automotive industry, with key players such as Bosch, Continental, and HELLA, has accelerated the widespread adoption of AVAS systems across Europe, making them standardized and scalable within a short period.

Major companies in the Vehicle Sound Synthesis Technology Market include Aptiv, General Motors, Tesla, Harman International, Denso, Continental, Hyundai Motor Company, Volkswagen, Delphi Technologies, and BMW Group. In the vehicle sound synthesis market, companies are focusing on developing advanced sound design and acoustic solutions that enhance the safety, branding, and emotional connection with customers. Many manufacturers have adopted strategic collaborations with sound designers and composers to create bespoke audio profiles for their vehicles. Additionally, they are increasing investments in research and development to ensure compliance with evolving regulations. Partnerships with key Tier 1 suppliers for hardware and control system development are also helping companies expand their capabilities. Furthermore, mass production strategies are being employed to make sound synthesis systems more affordable and widely accessible to consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Component

- 2.2.5 Application

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of electric and hybrid vehicles

- 3.2.1.2 Regulations by the government for pedestrian safety

- 3.2.1.3 Technological advancements in digital sound design

- 3.2.1.4 Increasing demands for in-car acoustic experiences

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration with legacy platforms and EV conversions

- 3.2.2.2 Limited awareness among smaller OEMs and tier-2 markets

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric and hybrid vehicles

- 3.2.3.2 Regulatory mandates for pedestrian safety

- 3.2.3.3 Demand for customizable brand sound signatures

- 3.2.3.4 Integration with advanced vehicle architectures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD, Million, Units)

- 5.1 Key trends

- 5.2 Internal sound system

- 5.3 External sound system

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 (USD, Million, Units)

- 6.1 Key trends

- 6.2 Internal combustion engine (ICE)

- 6.3 Electric vehicles (EV)

- 6.3.1 Battery electric vehicles (BEV)

- 6.3.2 Plug-in hybrid electric vehicles (PHEV)

- 6.3.3 Hybrid electric vehicles (HEV)

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 (USD, Million, Units)

- 7.1 Key trends

- 7.2 Hardware

- 7.2.1 Sound generators/modules

- 7.2.2 Speakers/transducers

- 7.2.3 Amplifiers

- 7.2.4 Controllers / ECUs

- 7.3 Software

- 7.3.1 Sound design & profile software

- 7.3.2 Sound synthesis algorithms

- 7.3.3 Vehicle integration software

- 7.3.4 Acoustic simulation & tuning tools

- 7.4 Services

- 7.4.1 Deployment & integration

- 7.4.2 Consulting

- 7.4.3 Support & maintenance

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD, Million, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchbacks

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCV)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales channel, 2021 - 2034 (USD, Million, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Audi

- 11.3 BMW Group

- 11.4 Brigade Electronics

- 11.5 BYD Auto Co.

- 11.6 Continental

- 11.7 Delphi Technologies

- 11.8 Denso Corporation

- 11.9 ECCO Safety Group

- 11.10 Ford Motor Company

- 11.11 General Motors Company

- 11.12 Harman International

- 11.13 Honda Motor Co.

- 11.14 Hyundai Motor Company

- 11.15 KUFATEC

- 11.16 Mando Hella Electronics Corp

- 11.17 Nissan Motor Corporation

- 11.18 STMicroelectronics

- 11.19 Tesla

- 11.20 Volkswagen

2026-2034年全球電動車聲音產生器市場規模、佔有率、趨勢與成長分析報告

2026-2034年全球電動車聲音產生器市場規模、佔有率、趨勢與成長分析報告 電動汽車揚聲器市場:按揚聲器類型、安裝位置、輸出功率、價格範圍、車輛類型和銷售管道的全球預測,2026-2032年

電動汽車揚聲器市場:按揚聲器類型、安裝位置、輸出功率、價格範圍、車輛類型和銷售管道的全球預測,2026-2032年 電動車聲音產生器市場,按推進方式、按車輛、按組件、按速度範圍、按銷售管道、按國家和地區 - 行業分析、市場規模、市場佔有率及預測(2024 年至 2032 年)

電動車聲音產生器市場,按推進方式、按車輛、按組件、按速度範圍、按銷售管道、按國家和地區 - 行業分析、市場規模、市場佔有率及預測(2024 年至 2032 年) 電動車聲音產生器市場-成長、未來展望與競爭分析(2025-2033)

電動車聲音產生器市場-成長、未來展望與競爭分析(2025-2033) 電動車聲音產生器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

電動車聲音產生器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 電動車聲音產生器系統的全球市場電動車用聲音產生器的全球市場-產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

電動車聲音產生器系統的全球市場電動車用聲音產生器的全球市場-產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)