|

市場調查報告書

商品編碼

1766221

標籤及編碼設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Labeling and Coding Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

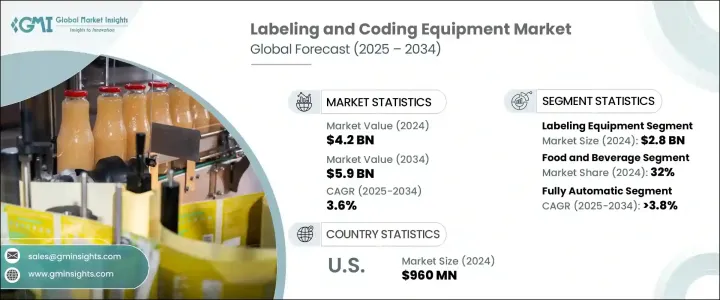

2024年,全球標籤和編碼設備市場規模達42億美元,預計到2034年將以3.6%的複合年成長率成長,達到59億美元。市場成長的動力源自於電子商務和物流的持續擴張、技術進步以及對精確度和品質保證的重視。雷射編碼、熱噴墨和連續噴墨列印等列印技術的改進顯著提高了標籤列印的效率和準確性。此外,人工智慧 (AI) 與物聯網 (IoT) 的結合徹底改變了該行業,提供了即時監控、預測性維護和更高水準的自動化,從而減少了停機時間和營運成本。

標籤和編碼設備在化學品、化妝品、製藥、食品飲料、農業和電子等各個行業中都至關重要,用於將標籤貼到容器、瓶子和小瓶上。由於對高速、高效和自動化貼標系統的需求不斷成長,自動貼標機市場正在迅速擴張。這些能夠自動剔除貼錯標籤產品的機器需求旺盛,尤其是在亞太地區和北美地區,這些地區不斷壯大的中產階級和不斷成長的可支配收入正在推動這些行業的擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 42億美元 |

| 預測值 | 59億美元 |

| 複合年成長率 | 3.6% |

2024年,標籤設備市場規模達28億美元,預計2034年的複合年成長率將達到3.9%。持續成長的關鍵因素在於標籤設備的重大技術進步。人工智慧 (AI) 和機器視覺系統的整合等創新顯著提升了標籤流程。這些技術使機器能夠掃描標籤並即時檢測潛在的錯誤或錯位,確保標籤正確貼上並符合監管標準。這種自動化程度不僅可以最大限度地減少人為錯誤,還能確保符合嚴格的行業法規,使這些機器更加可靠、高效。

2024年,食品飲料產業的市佔率將達到32%。隨著食品安全法規合規性要求的日益嚴格,包括美國食品藥物管理局(FDA)的《食品安全現代化法案》(FSMA)和歐盟的標籤標準,對精準高速標籤技術的需求也日益成長。這些法規促使食品飲料行業的製造商採用先進的標籤系統,例如熱噴墨和雷射打碼機,以確保產品的可追溯性並為消費者提供準確的資訊。這些技術不僅有助於確保合規性,還能提高生產效率。憑藉更快的列印速度、更少的停機時間和更少的標籤錯誤,它們在改進整體包裝流程方面發揮著至關重要的作用,從而縮短了產品週轉時間,並確保產品能夠正確、快速地貼上標籤並投放市場。

美國標籤和編碼設備市場佔據82%的市場佔有率,2024年市場規模達9.6億美元。電子商務和物流的快速成長,加上技術的進步,是美國標籤和編碼設備市場的主要驅動力。在客戶需求不斷成長、全球電子商務和貿易協定的推動下,物流行業實現了顯著成長,這鼓勵了美國製造商和零售商投資創新的物流解決方案。這種轉變使企業能夠利用其供應鏈能力來提供更優質的服務。

全球標籤和編碼設備市場的一些知名公司包括 Ambrose Packaging、CVC Technologies、BellatRx、BW Integrated Systems、Markem-Imaje、Hitachi IESA 和 Videojet。這些公司不斷創新,開發更有效率、更可靠的標籤解決方案,以滿足各行各業日益成長的需求。為了鞏固市場地位,標籤和編碼設備行業的公司正在採取多種策略。其中包括高度重視人工智慧整合和機器視覺系統等技術進步,以提高標籤流程的精確度和速度。該公司還透過提供各種可自訂的解決方案來擴展其產品組合,包括滿足各行各業需求的先進編碼和標籤系統。此外,這些公司還利用策略合作夥伴關係和收購來提高市場滲透率並擴大地理覆蓋範圍。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 電子商務與物流的擴張

- 技術進步

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 網路安全和資料完整性風險

- 機會

- 產品可追溯性需求不斷成長

- 永續性和環保包裝的興起

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 貼標設備

- 壓敏貼標機

- 列印貼標系統

- 套標機

- 其他(捲筒貼標機等)

- 噴碼設備

- 噴墨打碼機

- 熱轉印打碼機

- 雷射打碼機

- 其他(熱噴墨印表機等)

第6章:市場估計與預測:依營運模式,2021 年至 2034 年

- 主要趨勢

- 手動的

- 半自動

- 全自動

第7章:市場估計與預測:依印刷媒介,2021 - 2034 年

- 主要趨勢

- 初級包裝

- 二次包裝

- 三級包裝

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 食品和飲料

- 製藥

- 化妝品和個人護理

- 電子產品

- 物流與零售

- 其他

第9章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 直銷

- 間接銷售

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 11 章:公司簡介

- Ambrose Packaging

- BellatRx

- BW Integrated Systems

- CVC Technologies

- Domino Printing Sciences

- HERMA

- Hitachi IESA

- Leibinger

- Markem-Imaje

- Pack Leader USA

- PrintJet Corporation

- ProMach

- Sneed Coding Solutions

- Squid Ink

- Videojet

The Global Labeling and Coding Equipment Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 5.9 billion by 2034. The market growth is being driven by the continued expansion of e-commerce and logistics, technological advancements, and a focus on precision and quality assurance. Improvements in printing technologies, such as laser coding, thermal inkjet, and continuous inkjet printing, have significantly increased the effectiveness and accuracy of labeling processes. Furthermore, the combination of artificial intelligence (AI) and the Internet of Things (IoT) has revolutionized the industry, offering real-time monitoring, predictive maintenance, and higher levels of automation that reduce downtime and operating costs.

Labeling and coding equipment is essential in various industries such as chemicals, cosmetics, pharmaceuticals, food and beverage, agriculture, and electronics, where it is used to attach labels on containers, bottles, and vials. The market for automatic labeling machines is expanding rapidly due to the rising demand for high-speed, efficient, and automated labeling systems. These machines, capable of rejecting mislabeled products automatically, are in high demand, especially in regions such as Asia Pacific and North America, where the growing middle class and increased disposable income are driving the expansion of these industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 3.6% |

In 2024, the labeling equipment segment generated USD 2.8 billion, and it is anticipated to grow at a CAGR of 3.9% throughout 2034. A key factor behind this continued growth is the significant technological progress in labeling equipment. Innovations such as the integration of artificial intelligence (AI) and machine vision systems have significantly enhanced labeling processes. These technologies enable machines to scan labels and detect potential errors or misalignments in real-time, ensuring that labels are properly applied and that they meet regulatory standards. This level of automation not only minimizes human error but also ensures compliance with stringent industry regulations, making these machines more reliable and efficient.

The food & beverage segment held a 32% share in 2024. The demand for precise and high-speed labeling technologies is driven by the growing emphasis on compliance with food safety regulations, including the FDA's Food Safety Modernization Act (FSMA) and the European Union's labeling standards. These regulations have pushed manufacturers in the food and beverage sector to adopt advanced labeling systems, such as thermal inkjet and laser coding machines, to ensure product traceability and provide consumers with accurate information. Not only do these technologies help ensure regulatory compliance, but they also boost production efficiency. With faster printing speeds, reduced downtime, and fewer labeling errors, they play an essential role in improving the overall packaging process, thereby enhancing product turnaround times and ensuring that goods are labeled correctly and swiftly for the market.

United States Labeling and Coding Equipment Market held an 82% share and generated USD 960 million in 2024. The rapid growth of e-commerce and logistics, combined with advancements in technology, is a key driver of the U.S. labeling and coding equipment market. The logistics industry, fueled by rising customer demands, global e-commerce, and trade agreements, has seen significant growth, encouraging U.S.-based manufacturers and retailers to invest in innovative logistics solutions. This shift is enabling companies to leverage their supply chain capabilities for greater service delivery.

Some of the prominent companies operating in the Global Labeling and Coding Equipment Market include Ambrose Packaging, CVC Technologies, BellatRx, BW Integrated Systems, Markem-Imaje, Hitachi IESA, and Videojet. These companies are constantly innovating to develop more efficient and reliable labeling solutions to cater to the increasing demand from various industries. To strengthen their market position, companies in the labeling and coding equipment industry are adopting several strategies. These include a strong focus on technological advancements such as AI integration and machine vision systems, which improve the precision and speed of labeling processes. Companies are also expanding their product portfolios by offering a diverse range of customizable solutions, including advanced coding and labeling systems that cater to various industries. Furthermore, strategic partnerships and acquisitions are being used to increase market penetration and expand the geographical reach of these companies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 End use industry

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of e-commerce and logistics

- 3.2.1.2 Technological advancement

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Cybersecurity and data integrity risks

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for product traceability

- 3.2.3.2 Rising sustainability and eco-friendly packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Labeling equipment

- 5.2.1 Pressure-sensitive labelers

- 5.2.2 Print-and-apply labeling systems

- 5.2.3 Sleeve labelers

- 5.2.4 Others (roll-fed labelers etc.)

- 5.3 Coding equipment

- 5.3.1 Inkjet coding machine

- 5.3.2 Thermal transfer coders

- 5.3.3 Laser coders

- 5.3.4 Others (thermal inkjet printers etc.)

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates & Forecast, By Print Medium, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Primary packaging

- 7.3 Secondary packaging

- 7.4 Tertiary packaging

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Food and beverages

- 8.3 Pharmaceutical

- 8.4 Cosmetics and personal care

- 8.5 Electronics

- 8.6 Logistics and retail

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Ambrose Packaging

- 11.2 BellatRx

- 11.3 BW Integrated Systems

- 11.4 CVC Technologies

- 11.5 Domino Printing Sciences

- 11.6 HERMA

- 11.7 Hitachi IESA

- 11.8 Leibinger

- 11.9 Markem-Imaje

- 11.10 Pack Leader USA

- 11.11 PrintJet Corporation

- 11.12 ProMach

- 11.13 Sneed Coding Solutions

- 11.14 Squid Ink

- 11.15 Videojet

全球標籤和產品裝飾市場(2026 年)

全球標籤和產品裝飾市場(2026 年) 機器人自動化貼標系統市場:按技術、部署類型、組件、貼標輸出類型、自動化程度、服務、最終用戶產業和應用分類-全球預測,2026-2032年

機器人自動化貼標系統市場:按技術、部署類型、組件、貼標輸出類型、自動化程度、服務、最終用戶產業和應用分類-全球預測,2026-2032年 Sensamatic標籤市場規模、佔有率和成長分析:按產品類型、材料類型、技術、最終用戶和地區分類-2026-2033年產業預測

Sensamatic標籤市場規模、佔有率和成長分析:按產品類型、材料類型、技術、最終用戶和地區分類-2026-2033年產業預測 2026年全球醫療設備標籤市場報告

2026年全球醫療設備標籤市場報告 包裝標籤市場分析及預測(至2035年):依類型、產品類型、技術、材料類型、應用、形式、最終用戶、組件及功能分類標籤市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、組件、最終用戶、形式及解決方案分類

包裝標籤市場分析及預測(至2035年):依類型、產品類型、技術、材料類型、應用、形式、最終用戶、組件及功能分類標籤市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、組件、最終用戶、形式及解決方案分類 全球雙向拉伸聚丙烯(BOPP)標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球雙向拉伸聚丙烯(BOPP)標籤市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2025-2029年全球人工智慧資料標註市場自黏標籤市場:按材料、標籤類型、應用和最終用途產業分類,全球預測(2026-2032年)

2025-2029年全球人工智慧資料標註市場自黏標籤市場:按材料、標籤類型、應用和最終用途產業分類,全球預測(2026-2032年) 標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)