|

市場調查報告書

商品編碼

1755261

癌症治療設施市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cancer Treatment Facilities Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

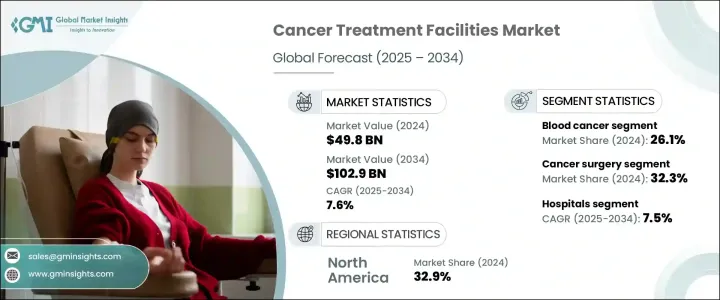

2024年,全球癌症治療設施市場規模達498億美元,預估年複合成長率達7.6%,2034年將達1,029億美元。癌症治療中心是專注於各類癌症診斷、治療和持續管理的專業醫療機構。這些中心通常提供化療、放射治療、免疫治療、外科手術和術後護理等服務。它們擁有由腫瘤科醫生、外科醫生、放射科醫生和護理人員組成的多學科專業團隊,以確保為每位患者提供量身定做的護理。

全球癌症發生率的上升是推動這一市場發展的主要動力。人口老化是癌症確診數量不斷成長的重要原因,這反過來又增加了對專科癌症治療的需求。為了滿足這些需求,治療機構正在加強基礎設施建設,並採用精準腫瘤學和多學科治療模式等先進技術。這些創新旨在滿足日益成長的老年人口的需求,而老年人口尤其容易患癌症。此外,醫療旅遊業也促進了癌症治療市場的擴張,尤其是在那些治療方案價格合理、吸引尋求低成本高品質醫療服務的國際患者的地區。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 498億美元 |

| 預測值 | 1029億美元 |

| 複合年成長率 | 7.6% |

2024年,血癌領域佔最大佔有率,達26.1%。這一成長得益於持續的臨床需求以及治療血液癌症所需的廣泛基礎設施,包括專科治療設施。此外,複雜、昂貴且通常密集的治療方案(包括化療、骨髓移植和免疫療法)也是市場擴張的主要推動因素。此外,對長期追蹤護理的需求、多學科醫療團隊的參與以及對先進診斷能力的需求,進一步凸顯了這些專科治療中心相對於專注於其他類型癌症的治療中心的重要性。

2024年,醫院佔據最大的市場佔有率,達到67.5%,預計將以7.5%的複合年成長率持續成長。醫院對癌症治療設施的需求源於其擁有先進的檢測工具以及包括化療、放療和荷爾蒙療法在內的多種治療方案。患者更青睞醫院,因為醫院提供全面的服務,並能獲得多專業照護團隊的協助。

2024年,美國癌症治療市場規模達149億美元,預計隨著人口老化和癌症病例增加,該市場將持續成長。這促進了綜合癌症中心的發展,這些中心提供機器人手術、免疫療法和精準醫療等尖端治療方案。 HCA Healthcare等主要產業參與者正在透過合作和人工智慧技術拓展業務範圍。政府措施和基於價值的醫療模式進一步推動了市場成長。

全球癌症治療設施市場的關鍵參與者包括 Alliance HealthCare Services、美國腫瘤研究所、阿波羅醫院企業、美國癌症治療中心、Compass Oncology、Curie Oncology、Fortis Healthcare、GenesisCare、HCA Healthcare、Healthcare Global Enterprises、IHH Healthcare Berhad、Narayana Hrudayalaya、OncoLife Hospitals、Ramcare Global Enterprises、IHH Healthcare Berhad、Narayana Hrudayalaya、OncoLife Hospitals、Ramsay Health Care 和 Tenet Healthcare。為了鞏固市場地位,癌症治療設施領域的公司正專注於整合人工智慧、機器人手術和精準醫療等先進技術。他們還透過與其他醫療保健提供者和組織建立策略合作夥伴關係來擴展服務。基於價值的照護模式的日益普及有助於改善患者的治療效果並降低成本。許多組織正在建立綜合癌症護理中心,提供從診斷到治療後護理的全方位服務。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 癌症發生率上升

- 老年人口不斷增加

- 醫療旅遊興起

- 政府措施和宣傳計劃增多

- 產業陷阱與挑戰

- 缺乏熟練的腫瘤學人員

- 先進治療和技術成本高昂

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

- 報銷場景

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依治療類型,2021 年至 2034 年

- 主要趨勢

- 癌症手術

- 化療

- 放射治療

- 免疫療法

- 骨髓移植

- 其他治療類型

第6章:市場估計與預測:按癌症類型,2021 年至 2034 年

- 主要趨勢

- 血癌

- 乳癌

- 攝護腺癌

- 胃腸道癌症

- 大腸直腸癌

- 肺癌

- 其他癌症類型

第7章:市場估計與預測:依供應商分類,2021 年至 2034 年

- 主要趨勢

- 醫院

- 癌症中心

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Alliance HealthCare Services

- American Oncology Institute

- Apollo Hospitals Enterprise

- Cancer Treatment Centers of America

- Compass Oncology

- Curie Oncology

- Fortis Healthcare

- GenesisCare

- HCA Healthcare

- Healthcare Global Enterprises

- IHH Healthcare Berhad

- Narayana Hrudayalaya

- OncoLife Hospitals

- Ramsay Health Care

- Tenet Healthcare

The Global Cancer Treatment Facilities Market was valued at USD 49.8 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 102.9 billion by 2034. Cancer treatment centers are specialized healthcare institutions focused on the diagnosis, treatment, and ongoing management of various cancer types. These centers typically offer services such as chemotherapy, radiation therapy, immunotherapy, surgical treatments, and aftercare. They employ multidisciplinary teams of professionals, including oncologists, surgeons, radiologists, and nursing staff, to ensure tailored care for each patient.

The rising global prevalence of cancer is the main driver for this market. Aging populations significantly contribute to the growing number of cancer diagnoses, which in turn is increasing the demand for specialized cancer care. To meet these needs, treatment facilities are enhancing their infrastructure and adopting advanced technologies, such as precision oncology and multidisciplinary treatment models. These innovations aim to cater to the growing elderly demographic, which is particularly vulnerable to cancer. Additionally, medical tourism is contributing to the expansion of the cancer treatment market, particularly in regions where affordable treatment options attract international patients seeking high-quality care at lower costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $49.8 Billion |

| Forecast Value | $102.9 Billion |

| CAGR | 7.6% |

The blood cancer segment held the largest share of 26.1% in 2024. This growth is driven by the ongoing clinical demand and the extensive infrastructure required to treat hematological cancers, including specialized treatment facilities. Moreover, the complex, costly, and often intensive treatment protocols, which involve chemotherapy, bone marrow transplants, and immunotherapy, are major contributors to the market's expansion. Moreover, the requirement for long-term follow-up care, the involvement of multidisciplinary medical teams, and the need for advanced diagnostic capabilities further emphasize the importance of these specialized treatment centers over those focused on other cancer types.

In 2024, the hospitals segment held the largest market share, accounting for 67.5% share, and is expected to continue growing at a CAGR of 7.5%. The demand for cancer treatment facilities in hospitals is driven by the availability of advanced detection tools and a wide range of treatment options, including chemotherapy, radiation, and hormone therapy. Patients prefer hospitals for their comprehensive services and access to multidisciplinary care teams.

U.S. Cancer Treatment Market was valued at USD 14.9 billion in 2024 and is expected to see continued growth due to an aging population and an increase in cancer cases. This has led to the development of integrated cancer centers that provide cutting-edge treatments like robotic surgery, immunotherapy, and precision medicine. Major industry players, such as HCA Healthcare, are expanding their reach through partnerships and incorporating AI technologies. Government initiatives and value-based care models further drive market growth.

Key players in the Global Cancer Treatment Facilities Market include Alliance HealthCare Services, American Oncology Institute, Apollo Hospitals Enterprise, Cancer Treatment Centers of America, Compass Oncology, Curie Oncology, Fortis Healthcare, GenesisCare, HCA Healthcare, Healthcare Global Enterprises, IHH Healthcare Berhad, Narayana Hrudayalaya, OncoLife Hospitals, Ramsay Health Care, Tenet Healthcare. To strengthen their market position, companies in the cancer treatment facilities sector are focusing on the integration of advanced technologies such as AI, robotic surgery, and precision medicine. They are also expanding their services through strategic partnerships with other healthcare providers and organizations. The increasing adoption of value-based care models helps improve patient outcomes while reducing costs. Many organizations are building integrated cancer care centers to offer comprehensive services, from diagnosis to post-treatment care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Rise in medical tourism

- 3.2.1.4 Increase in government initiatives and awareness programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled oncology personnel

- 3.2.2.2 High cost of advanced treatments and technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Reimbursement Scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cancer surgery

- 5.3 Chemotherapy

- 5.4 Radiation therapy

- 5.5 Immunotherapy

- 5.6 Bone marrow transplantation

- 5.7 Other treatment types

Chapter 6 Market Estimates and Forecast, By Cancer Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Blood cancer

- 6.3 Breast cancer

- 6.4 Prostate cancer

- 6.5 Gastrointestinal cancer

- 6.6 Colorectal cancer

- 6.7 Lung cancer

- 6.8 Other cancer types

Chapter 7 Market Estimates and Forecast, By Provider, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cancer centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alliance HealthCare Services

- 9.2 American Oncology Institute

- 9.3 Apollo Hospitals Enterprise

- 9.4 Cancer Treatment Centers of America

- 9.5 Compass Oncology

- 9.6 Curie Oncology

- 9.7 Fortis Healthcare

- 9.8 GenesisCare

- 9.9 HCA Healthcare

- 9.10 Healthcare Global Enterprises

- 9.11 IHH Healthcare Berhad

- 9.12 Narayana Hrudayalaya

- 9.13 OncoLife Hospitals

- 9.14 Ramsay Health Care

- 9.15 Tenet Healthcare

光免疫療法市場-全球產業規模、佔有率、趨勢、機會及預測(依治療領域、最終用戶、地區及競爭格局分類,2021-2031年)癌症奈米技術市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭對手分類,2021-2031年

光免疫療法市場-全球產業規模、佔有率、趨勢、機會及預測(依治療領域、最終用戶、地區及競爭格局分類,2021-2031年)癌症奈米技術市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用戶、地區和競爭對手分類,2021-2031年 2025-2029年癌症治療技術領域的成長機會

2025-2029年癌症治療技術領域的成長機會 紫杉葉素:全球市場佔有率和排名、總收入和需求預測(2025-2031年)癌症基因治療:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)癌症光動力療法的全球市場:光敏化劑的臨床試驗預測(2030年)

紫杉葉素:全球市場佔有率和排名、總收入和需求預測(2025-2031年)癌症基因治療:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)癌症光動力療法的全球市場:光敏化劑的臨床試驗預測(2030年) 奈米技術在癌症治療的應用:科技與全球市場

奈米技術在癌症治療的應用:科技與全球市場 癌症治療市場:依治療類型、癌症類型和地區分類

癌症治療市場:依治療類型、癌症類型和地區分類 癌症治療設施市場規模、佔有率、趨勢分析報告:按治療、癌症類型、提供者、地區和細分市場預測,2024-2030 年

癌症治療設施市場規模、佔有率、趨勢分析報告:按治療、癌症類型、提供者、地區和細分市場預測,2024-2030 年