|

市場調查報告書

商品編碼

1755249

3D 列印義肢市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測3D Printed Prosthetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

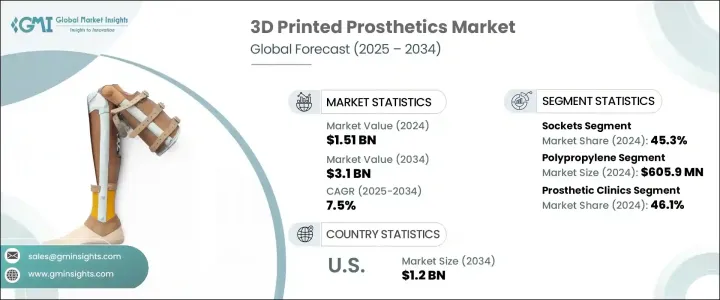

2024年,全球3D列印義肢市場規模達15.1億美元,預計2034年將以7.5%的複合年成長率成長,達到31億美元。這主要得益於患者對高度個人化義肢解決方案日益成長的需求,因為患者尋求根據自身特定解剖結構和日常需求量身定做的義肢。與通常速度慢、成本高且需要多次試戴的傳統製造方法不同,3D列印技術提供了一種更快速、更經濟的方法。這些客製化解決方案不僅提升了整體使用者體驗,也縮短了生產時間。個人化訂製對兒科患者尤其重要,因為他們的需求會隨著成長而不斷變化,需要更頻繁地更換義肢。先進的3D列印義肢技術在滿足全球醫療機構對個人化醫療器材需求方面邁出了一大步。

積層製造技術的進步,包括立體光固化成型 (SLA)、選擇性雷射燒結 (SLS) 和熔融沈積成型 (FDM),正在協助打造耐用、輕巧且功能齊全的義肢組件。隨著美國食品藥物管理局 (FDA) 等監管機構批准多種 3D 列印義肢,該技術正不斷獲得認可和發展。醫用級聚合物和合金等生物相容性材料的出現,進一步提升了義肢的耐用性、舒適性和適應性。這些創新不僅縮短了生產週期,還提高了義肢的品質和精確度,使醫護人員和患者都能更輕鬆地獲得義肢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15.1億美元 |

| 預測值 | 31億美元 |

| 複合年成長率 | 7.5% |

聚丙烯憑藉其良好的強度重量比、抗疲勞性和化學穩定性,在2024年佔據材料領域的領先地位,產值達6.059億美元。聚丙烯廣泛應用於醫療製造領域,因其生物相容性和抗滅菌性能而備受推崇。它被廣泛用於製造義肢接受腔、手術導板和矯形支架。隨著3D列印技術對輕量化和個人化醫療解決方案的需求不斷成長,聚丙烯的應用也隨之不斷擴大。其兼具柔軟性和功能性,使其成為以患者為中心的設計的首選。

2024年,義肢診所市佔率達46.1%。這些專科中心正擴大整合3D列印技術,以應對日益成長的患者數量,尤其是在糖尿病和血管疾病等慢性疾病導致截肢率較高的地區。診所受益於3D列印的高效性,因為它可以快速修改並頻繁更換義肢——這對兒科患者尤其重要。這些機構通常提供一體化服務,包括復健、培訓和後續服務,從而鼓勵更多人採用3D列印義肢。其集中式方法簡化了使用者體驗,並在尋求長期解決方案的患者中建立了信任。

受肥胖、糖尿病和周邊動脈疾病發病率上升的推動,美國3D列印義肢市場預計到2034年將達到12億美元,凸顯了對先進義肢解決方案的迫切需求。遠距醫療、雲端工作流程和遠距病患掃描等數位醫療創新技術的融合,為3D列印義肢的推廣創造了肥沃的土壤。這些發展使臨床醫生能夠提供更準確、更及時的護理,從而促進其在整個醫療保健領域的廣泛應用。

影響 3D 列印義肢產業的關鍵參與者包括 YouBionic、WillowWood、Mercuris、Limbitless Solutions、Stratasys、Bionic Prosthetics and Orthotics、Create Prosthetics、UNYQ、Protosthetics、Prothea、Open Bionics、Eqwal Group (Steeper Group)、Material Motor、Exthea、Open Bionics、Eqwal Group (Steeper Group)、Materials、Exthea、Material、Exone 和 Motoreper Group)、Material、Exone 和)為鞏固市場地位,3D 列印義肢領域的公司正在實施多種策略方針。主要重點是透過利用先進的軟體和掃描技術擴大產品客製化。公司還在投資研發,以提高材料品質和舒適度。與醫院、復健中心和研究機構的策略合作有助於增加可近性並加速創新。此外,公司正在增強數位化工作流程,例如遠端肢體掃描和基於雲端的設計,以簡化生產並透過線上平台和在地化列印中心進行地理擴展。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 對個人化和可負擔義肢解決方案的需求不斷增加

- 3D列印和材料的技術進步

- 因糖尿病、創傷和血管疾病導致肢體缺失的發生率不斷上升

- 非營利組織和人道主義計劃的支持日益增多

- 產業陷阱與挑戰

- 缺乏標準化法規和品質控制

- 熟練的專業人員和技術知識有限

- 成長動力

- 成長潛力分析

- 差距分析

- 技術格局

- 未來市場趨勢

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 專利分析

- 定價分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 競爭市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 四肢

- 插座

- 關節

- 其他類型

第6章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 聚丙烯

- 聚乙烯

- 丙烯酸樹脂

- 聚氨酯

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 復健中心

- 義肢診所

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Bionic Prosthetics and Orthotics

- Create Prosthetics

- Eqwal Group (Steeper Group)

- Exone

- Limbitless Solutions

- Materialise

- Mercuris

- Motorica

- Open Bionics

- Prothea

- Protosthetics

- Stratasys

- UNYQ

- WillowWood

- YouBionic

The Global 3D Printed Prosthetics Market was valued at USD 1.51 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 3.1 billion by 2034, driven by the increasing demand for highly personalized prosthetic solutions, as patients seek devices tailored to their specific anatomy and day-to-day needs. Unlike conventional manufacturing methods-which are often slow and expensive and involve numerous fitting sessions-3D printing technology offers a faster and more cost-efficient approach. These custom solutions improve the overall user experience while cutting down production time. Personalization is especially valuable for pediatric patients, whose needs change frequently as they grow, requiring replacements more often. Advanced 3D printing in prosthetics is a major leap forward in meeting global healthcare demands for individualized medical devices.

Technological advancements in additive manufacturing, including Stereolithography (SLA), Selective Laser Sintering (SLS), and Fused Deposition Modeling (FDM), are enabling the creation of durable, lightweight, and functional prosthetic components. With the approval of multiple 3D printed prosthetic devices by regulatory bodies like the U.S. FDA, the technology continues gaining credibility and momentum. The availability of biocompatible materials such as medical-grade polymers and alloys has further enhanced the durability, comfort, and adaptability of prosthetic devices. These innovations not only reduce production cycles but also elevate the quality and precision of prosthetics, making them more accessible for medical professionals and patients alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.51 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.5% |

Polypropylene led the material segment generating USD 605.9 million in 2024, owing to its favorable strength-to-weight ratio, fatigue resistance, and chemical stability. Widely adopted in medical manufacturing, polypropylene is valued for its biocompatibility and ability to withstand sterilization. It is extensively used to fabricate prosthetic sockets, surgical guides, and orthotic supports. As demand rises for lightweight and personalized medical solutions via 3D printing, the utilization of polypropylene continues to expand. Its blend of softness and functionality makes it a preferred choice in patient-centric designs.

The prosthetic clinics segment held a 46.1% share in 2024. These specialized centers are increasingly integrating 3D printing to manage growing patient volumes, especially in regions with high rates of amputation caused by chronic conditions like diabetes and vascular disease. Clinics benefit from 3D printing's efficiency, as it allows for quick modifications and frequent replacements-particularly vital for pediatric patients. These facilities often serve as all-in-one providers, offering rehabilitation, training, and follow-up services, encouraging greater adoption of 3D printed prosthetics. Their centralized approach simplifies the user experience and builds trust among patients seeking long-term solutions.

U.S. 3D Printed Prosthetics Market is expected to reach USD 1.2 billion by 2034 driven by rising incidences of obesity, diabetes, and peripheral artery disease, underscoring the urgent need for advanced prosthetic solutions. The integration of digital health innovations such as telehealth, cloud-based workflows, and remote patient scanning is creating fertile ground for the expansion of 3D printed prosthetics. These developments allow clinicians to deliver more accurate and timely care, contributing to broader adoption across the healthcare landscape.

Key players shaping the 3D Printed Prosthetics Industry include YouBionic, WillowWood, Mercuris, Limbitless Solutions, Stratasys, Bionic Prosthetics and Orthotics, Create Prosthetics, UNYQ, Protosthetics, Prothea, Open Bionics, Eqwal Group (Steeper Group), Materialise, Exone, and Motorica. To strengthen their market foothold, companies in the 3D printed prosthetics space are implementing multiple strategic approaches. A primary focus is expanding product customization by leveraging advanced software and scanning technologies. Firms are also investing in R&D to improve material quality and comfort. Strategic collaborations with hospitals, rehabilitation centers, and research institutions are helping to increase access and accelerate innovation. In addition, companies are enhancing digital workflows, such as remote limb scanning and cloud-based design, to streamline production and expand geographically through online platforms and localized printing hubs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for personalized and affordable prosthetic solutions

- 3.2.1.2 Technological advancements in 3D printing and materials

- 3.2.1.3 Rising incidence of limb loss due to diabetes, trauma, and vascular diseases

- 3.2.1.4 Growing support from non-profits and humanitarian initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standardized regulations and quality control

- 3.2.2.2 Limited availability of skilled professionals and technical knowledge

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Gap analysis

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Limbs

- 5.3 Sockets

- 5.4 Joints

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polypropylene

- 6.3 Polyethylene

- 6.4 Acrylics

- 6.5 Polyurethane

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Rehabilitation centers

- 7.4 Prosthetic clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bionic Prosthetics and Orthotics

- 9.2 Create Prosthetics

- 9.3 Eqwal Group (Steeper Group)

- 9.4 Exone

- 9.5 Limbitless Solutions

- 9.6 Materialise

- 9.7 Mercuris

- 9.8 Motorica

- 9.9 Open Bionics

- 9.10 Prothea

- 9.11 Protosthetics

- 9.12 Stratasys

- 9.13 UNYQ

- 9.14 WillowWood

- 9.15 YouBionic

3D列印義肢市場:按技術、材料、類型、應用和最終用戶分類-2026-2032年全球市場預測

3D列印義肢市場:按技術、材料、類型、應用和最終用戶分類-2026-2032年全球市場預測 全球3D列印整形外科植入市場研究報告(2026年版)

全球3D列印整形外科植入市場研究報告(2026年版) 2026年全球3D列印義肢市場報告2026年全球3D整形外科和義肢市場報告2026年全球個人化膝關節植入市場報告2026年全球整形外科3D列印設備市場報告

2026年全球3D列印義肢市場報告2026年全球3D整形外科和義肢市場報告2026年全球個人化膝關節植入市場報告2026年全球整形外科3D列印設備市場報告 全球3D列印義肢市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印骨科材料市場:按材料類型、列印技術、應用和最終用途分類-2026-2032年全球預測

全球3D列印義肢市場規模、佔有率、趨勢和成長分析報告(2026-2034年)3D列印骨科材料市場:按材料類型、列印技術、應用和最終用途分類-2026-2032年全球預測 3D列印整形外科器械的全球市場

3D列印整形外科器械的全球市場 2025-2029年全球整形外科3D列印設備市場

2025-2029年全球整形外科3D列印設備市場