|

市場調查報告書

商品編碼

1750542

蒸汽鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Steam Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

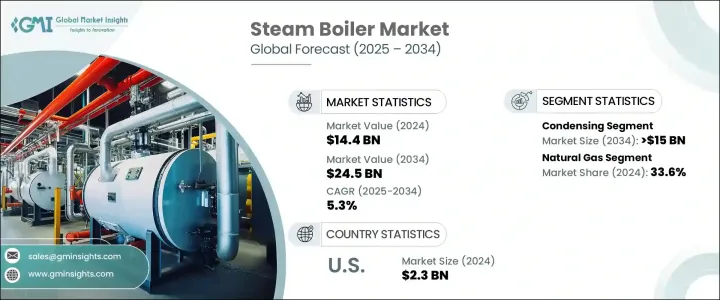

2024年,全球蒸汽鍋爐市場規模達144億美元,預計到2034年將以5.3%的複合年成長率成長,達到245億美元,這得益於全球主要經濟體的快速工業化和能源基礎設施的大量投資。各行各業對高效能蒸汽發電系統的需求日益成長,以及其在商業和工業空間供暖中的應用日益增多,將支撐市場擴張。此外,可支配收入的增加和生活水準的提高(尤其是在寒冷地區),也將推動蒸汽鍋爐的需求成長。這些因素,加上工業生產中對減少碳足跡的日益重視,將進一步推動市場成長。

減排趨勢也在塑造市場方面發揮著至關重要的作用。各國政府正在實施更嚴格的氮氧化物和硫氧化物排放法規,這鼓勵各行各業採用包括高壓鍋爐在內的先進技術。此外,遠端監控、預測性維護和最佳化負載管理等數位技術的融入將提高營運效率,減少非計劃性停機,並增強系統可靠性。這項技術進步也將增加對更先進蒸汽鍋爐的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 144億美元 |

| 預測值 | 245億美元 |

| 複合年成長率 | 5.3% |

受能源價格上漲和日益嚴格的排放法規合規要求的推動,冷凝式蒸汽鍋爐市場規模預計到2034年將達到150億美元。冷凝式鍋爐效率高,與傳統系統相比,燃油經濟性更高,碳排放量更低,因此成為尋求降低營運成本和環境足跡的行業的首選。政府推出的節能技術誘因進一步鼓勵了這些系統的採用,為市場成長增添了動力。

另一方面,預計到2034年,燃油蒸汽鍋爐市場將以4%的複合年成長率成長。這類鍋爐在石化、煉油和熱油加工等重工業領域尤其受歡迎。燃油鍋爐因其高調節比而備受青睞,能夠根據需求變化精確調節蒸汽流量。這種適應性使其成為在各種負荷條件下都需要穩定可靠蒸汽供應的工業應用中不可或缺的一部分。這些系統在高需求環境下的可靠性和性能將繼續推動其持續需求。

2024年,美國蒸汽鍋爐市場規模達23億美元,這得益於新製造設施的大量投資,以及以現代節能鍋爐技術取代過時暖氣系統的持續趨勢。隨著各行各業注重降低能耗和實現永續發展目標,對先進蒸汽鍋爐系統的需求持續成長。此外,美國正在經歷基礎設施的持續現代化,這進一步推動了工業和商業領域對高效蒸汽發電解決方案的需求。

全球蒸汽鍋爐市場中的企業正專注於策略創新和擴張,以提升市場佔有率。例如,一些企業專注於推進鍋爐技術,以滿足嚴格的環境法規並提供更節能的解決方案。這些企業還投資於數位監控工具,以更好地控制營運並延長鍋爐使用壽命。市場的主要參與者包括 Aggreko、ALFA LAVAL、Miura America 和 Thermax,它們都在推動創新,並致力於透過產品多元化和全球擴張來鞏固其市場地位。他們的策略還包括專注於節能解決方案並加強售後支持,以提高客戶滿意度和忠誠度。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 策略舉措

- 公司市佔率分析

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:按燃料,2021 - 2034

- 主要趨勢

- 天然氣

- 油

- 煤炭

- 其他

第6章:市場規模及預測:依產能,2021 - 2034 年

- 主要趨勢

- ≤ 10 百萬英熱單位/小時

- > 10 - 50 百萬英熱單位/小時

- > 50 - 100 百萬英熱單位/小時

- > 100 - 250 百萬英熱單位/小時

- > 250 百萬英熱單位/小時

第7章:市場規模及預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 冷凝

- 無凝結

第 8 章:市場規模與預測:按應用,2021 - 2034 年

- 主要趨勢

- 商業的

- 容量

- ≤ 10 百萬英熱單位/小時

- > 10 - 50 百萬英熱單位/小時

- > 50 - 100 百萬英熱單位/小時

- > 100 - 250 百萬英熱單位/小時

- > 250 百萬英熱單位/小時

- 燃料

- 天然氣

- 油

- 煤炭

- 其他

- 科技

- 冷凝

- 無凝結

- 容量

- 工業的

- 容量

- ≤ 10 百萬英熱單位/小時

- > 10 - 50 百萬英熱單位/小時

- > 50 - 100 百萬英熱單位/小時

- > 100 - 250 百萬英熱單位/小時

- > 250 百萬英熱單位/小時

- 燃料

- 天然氣

- 油

- 煤炭

- 其他

- 科技

- 冷凝

- 無凝結

- 容量

第9章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 英國

- 波蘭

- 義大利

- 西班牙

- 奧地利

- 德國

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 菲律賓

- 日本

- 韓國

- 澳洲

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 伊朗

- 阿拉伯聯合大公國

- 奈及利亞

- 南非

- 拉丁美洲

- 阿根廷

- 智利

- 巴西

第10章:公司簡介

- Aggreko

- ALFA LAVAL

- Babcock & Wilcox

- Babcock Wanson

- Bosch Industriekessel

- Clayton Industries

- Cleaver-Brooks

- Cochran

- FERROLI

- Forbes Marshall

- Fulton

- GE Vernova

- Hoval

- Hurst Boiler & Welding

- John Cockerill

- Miura America

- PM Lattner Manufacturing

- PARKER BOILER

- Precision Boilers

- Thermax

- VIESSMANN

- Weil-McLain

The Global Steam Boiler Market was valued at USD 14.4 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 24.5 billion by 2034, driven by the rapid industrialization in key global economies and substantial investments in energy infrastructure. A growing demand for efficient steam generation systems across industries, along with their increasing use for space heating in commercial and industrial settings, will support market expansion. Additionally, the rising disposable income and improved living standards, especially in colder regions, will drive the demand for steam boilers. These factors, combined with a heightened focus on reducing carbon footprints in industrial operations, will further boost the market's growth.

The trend toward reducing emissions is also playing a crucial role in shaping the market. Governments are implementing stricter regulations on NOx and SOx emissions, which is encouraging industries to adopt advanced technologies, including high-pressure boilers. Moreover, the incorporation of digital technologies such as remote monitoring, predictive maintenance, and optimized load management will make operations more efficient, reducing unplanned shutdowns and enhancing system reliability. This technological advancement will also increase demand for more sophisticated steam boilers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $24.5 Billion |

| CAGR | 5.3% |

The condensing steam boiler market is projected to reach USD 15 billion by 2034, driven by the rising energy prices and the increasing need to comply with stringent emissions regulations. Condensing boilers are highly efficient, offering better fuel economy and lower carbon emissions compared to traditional systems, making them a preferred choice for industries looking to reduce both operational costs and their environmental footprint. Government incentives promoting energy-efficient technologies are further encouraging the adoption of these systems, adding momentum to the market's growth.

On the other hand, the oil-fueled steam boiler market is anticipated to grow at a CAGR of 4% until 2034. These boilers are particularly popular in heavy industries such as petrochemicals, refineries, and thermal oil processing. Oil-fired boilers are valued for their high turndown ratios, allowing them to adjust steam flow precisely according to changing demand. This adaptability makes them indispensable in industrial applications that require a consistent and reliable steam supply under varying load conditions. The ongoing demand for these systems will continue to be driven by their reliability and performance in high-demand environments.

United States Steam Boiler Market generated USD 2.3 billion in 2024, attributed to substantial investments in new manufacturing facilities and the ongoing trend of replacing outdated heating systems with modern, energy-efficient boiler technologies. As industries focus on reducing energy consumption and meeting sustainability goals, the demand for advanced steam boiler systems continues to rise. Additionally, the U.S. is experiencing an ongoing modernization of infrastructure, further driving the demand for efficient steam generation solutions in both the industrial and commercial sectors.

Companies in the Global Steam Boiler Market are focusing on strategic innovations and expansion to enhance their market share. For example, some players are focusing on advancing boiler technology to meet stringent environmental regulations and provide more energy-efficient solutions. The companies are also investing in digital monitoring tools to offer better control over operations and increase boiler longevity. Key players in the market include Aggreko, ALFA LAVAL, Miura America, and Thermax, all of which are driving innovation and aiming to strengthen their market positions through product diversification and global expansion. Their strategies also include focusing on energy-efficient solutions and strengthening after-sales support to enhance customer satisfaction and loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market scope & definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 5.1 Key trends

- 5.2 Natural gas

- 5.3 Oil

- 5.4 Coal

- 5.5 Others

Chapter 6 Market Size and Forecast, By Capacity, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 6.1 Key trends

- 6.2 ≤ 10 MMBTU/hr

- 6.3 > 10 - 50 MMBTU/hr

- 6.4 > 50 - 100 MMBTU/hr

- 6.5 > 100 - 250 MMBTU/hr

- 6.6 > 250 MMBTU/hr

Chapter 7 Market Size and Forecast, By Technology, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 7.1 Key trends

- 7.2 Condensing

- 7.3 Non-condensing

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.2.1 Capacity

- 8.2.1.1 ≤ 10 MMBTU/hr

- 8.2.1.2 > 10 - 50 MMBTU/hr

- 8.2.1.3 > 50 - 100 MMBTU/hr

- 8.2.1.4 > 100 - 250 MMBTU/hr

- 8.2.1.5 > 250 MMBTU/hr

- 8.2.2 Fuel

- 8.2.2.1 Natural gas

- 8.2.2.2 Oil

- 8.2.2.3 Coal

- 8.2.2.4 Others

- 8.2.3 Technology

- 8.2.3.1 Condensing

- 8.2.3.2 Non-condensing

- 8.2.1 Capacity

- 8.3 Industrial

- 8.3.1 Capacity

- 8.3.1.1 ≤ 10 MMBTU/hr

- 8.3.1.2 > 10 - 50 MMBTU/hr

- 8.3.1.3 > 50 - 100 MMBTU/hr

- 8.3.1.4 > 100 - 250 MMBTU/hr

- 8.3.1.5 > 250 MMBTU/hr

- 8.3.2 Fuel

- 8.3.2.1 Natural gas

- 8.3.2.2 Oil

- 8.3.2.3 Coal

- 8.3.2.4 Others

- 8.3.3 Technology

- 8.3.3.1 Condensing

- 8.3.3.2 Non-condensing

- 8.3.1 Capacity

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (Units, MMBTU/hr & USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 France

- 9.3.2 UK

- 9.3.3 Poland

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Germany

- 9.3.8 Sweden

- 9.3.9 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Philippines

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Australia

- 9.4.7 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 Iran

- 9.5.3 UAE

- 9.5.4 Nigeria

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Argentina

- 9.6.2 Chile

- 9.6.3 Brazil

Chapter 10 Company Profiles

- 10.1 Aggreko

- 10.2 ALFA LAVAL

- 10.3 Babcock & Wilcox

- 10.4 Babcock Wanson

- 10.5 Bosch Industriekessel

- 10.6 Clayton Industries

- 10.7 Cleaver-Brooks

- 10.8 Cochran

- 10.9 FERROLI

- 10.10 Forbes Marshall

- 10.11 Fulton

- 10.12 GE Vernova

- 10.13 Hoval

- 10.14 Hurst Boiler & Welding

- 10.15 John Cockerill

- 10.16 Miura America

- 10.17 P.M. Lattner Manufacturing

- 10.18 PARKER BOILER

- 10.19 Precision Boilers

- 10.20 Thermax

- 10.21 VIESSMANN

- 10.22 Weil-McLain

全球商用蒸氣鍋爐市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球商用蒸氣鍋爐市場規模、佔有率、趨勢和成長分析報告:2026-2034年 燃氣蒸氣鍋爐系統市場按壓力類型、安裝類型、燃料類型、產品類型、容量範圍和應用分類,全球預測(2026-2032年)

燃氣蒸氣鍋爐系統市場按壓力類型、安裝類型、燃料類型、產品類型、容量範圍和應用分類,全球預測(2026-2032年) 燃氣渦輪機和蒸氣渦輪:全球市場蒸氣鍋爐系統市場:預測(2025-2030 年)蒸氣鍋爐系統市場:按燃料類型、鍋爐類型、最終用途、容量範圍、壓力類型和安裝類型分類 - 2025-2032 年全球預測

燃氣渦輪機和蒸氣渦輪:全球市場蒸氣鍋爐系統市場:預測(2025-2030 年)蒸氣鍋爐系統市場:按燃料類型、鍋爐類型、最終用途、容量範圍、壓力類型和安裝類型分類 - 2025-2032 年全球預測 全球工業用燃氣低溫鍋爐市場

全球工業用燃氣低溫鍋爐市場 蒸汽鍋爐系統市場-全球產業規模、佔有率、趨勢、機會和預測,按鍋爐類型、按組件、按最終用途行業、按地區和競爭情況細分,2020-2030 年

蒸汽鍋爐系統市場-全球產業規模、佔有率、趨勢、機會和預測,按鍋爐類型、按組件、按最終用途行業、按地區和競爭情況細分,2020-2030 年 商用蒸汽鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測燃氣低溫工業鍋爐市場機會、成長動力、產業趨勢分析與預測 2025 - 2034全球蒸汽鍋爐市場規模(按類型、燃料類型、最終用戶、地區、範圍和預測)

商用蒸汽鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測燃氣低溫工業鍋爐市場機會、成長動力、產業趨勢分析與預測 2025 - 2034全球蒸汽鍋爐市場規模(按類型、燃料類型、最終用戶、地區、範圍和預測)