|

市場調查報告書

商品編碼

1750514

商用瓦斯鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Commercial Gas Fired Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

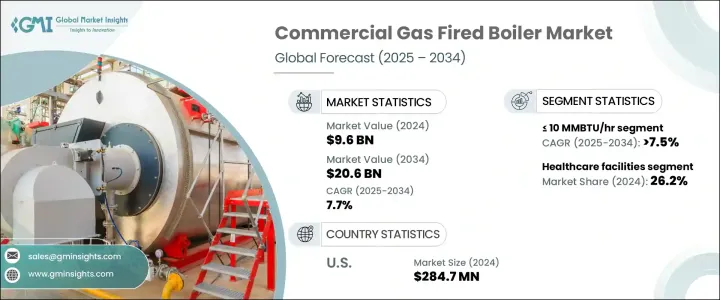

2024年,全球商用瓦斯鍋爐市場規模達96億美元,預計到2034年將以7.7%的複合年成長率成長,達到206億美元。這得益於各行業不斷變化的供暖需求,以及對更智慧、更有效率建築系統的持續追求。物聯網(IoT)在鍋爐系統中的日益普及,實現了遠端監控、即時效能最佳化和預測性維護,從而減少了停機時間並降低了營運成本。該行業受益於氫混合技術的創新,領先的製造商正在設計先進的模型來滿足不斷變化的供暖需求。這些努力旨在支持更清潔的能源轉型,同時保持性能可靠性。

模組化暖氣系統需求的成長正在改變大型園區、公司辦公室和商業設施的能源使用方式。生物技術、製藥和資料基礎設施等領域的持續擴張,推動了對可靠性和適應性兼具的精準供暖解決方案的需求。為了應對供應鏈的不確定性和不斷變化的貿易法規,鍋爐製造商投資於國內生產,以提高供應響應能力並降低地緣政治風險。例如,早期對金屬徵收的關稅顯著影響了製造業的經濟效益,促使企業實施在地化營運並多元化零件採購策略。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 96億美元 |

| 預測值 | 206億美元 |

| 複合年成長率 | 7.7% |

額定功率小於等於 10 MMBTU/小時的系統預計將保持強勁成長勢頭,到 2034 年將以 7.5% 的複合年成長率成長。這些緊湊高效的解決方案非常適合空間受限的環境,例如教育機構、零售店、醫療機構和酒店建築。其可擴展性以及較低的前期和維護成本,提供了一種經濟高效的方式,可在不影響性能或排放標準的情況下提供持續的供暖。

預計到2034年,商業辦公室市場規模將達到35億美元,這得益於對符合現代永續發展基準的智慧節能暖氣系統日益成長的需求。企業正在採用冷凝鍋爐和超低氮氧化物技術,不僅是為了滿足合規要求,也是為了提高營運效率。與建築自動化系統的整合正變得越來越普遍,使設施管理人員能夠控制暖氣負荷並減少能源浪費。

受全國範圍內基礎設施現代化建設和更嚴格的環境法規(旨在減少溫室氣體排放)的推動,美國商用燃氣鍋爐市場在2024年實現了2.847億美元的產值。商業建築,尤其是那些需要供暖升級的老舊建築,正在轉向支援更高熱效率和數位化整合的先進鍋爐系統。政府激勵措施和鼓勵採用清潔能源的區域法規也促進了高性能燃氣替代系統取代傳統系統的趨勢。

BDR Thermea Group、Lochinvar、Viessmann、Ariston Holding、Bosch Industriekessel、Weil-McLain、Bradford White Corporation、AO Smith、Burnham Commercial、大金、Vaillant Group、FERROLI、FONDITAL、Immergas、Remeha、Hoval、Cleaver-Brooks 和 Babcock & Bab.這些策略包括擴展智慧產品線、強化氫能車型研發、改進客戶支援系統以及建立區域製造中心,以提高交付速度並降低成本,同時實現永續發展目標。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 策略舉措

- 公司市佔率分析

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依產能,2021 - 2034 年

- 主要趨勢

- ≤ 10 百萬英熱單位/小時

- > 10 - 50 百萬英熱單位/小時

- > 50 - 100 百萬英熱單位/小時

- > 100 - 250 百萬英熱單位/小時

- > 250 百萬英熱單位/小時

第6章:市場規模及預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 冷凝

- 無凝結

第7章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 辦公室

- 醫療保健設施

- 教育機構

- 住宿

- 零售店

- 其他

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 英國

- 波蘭

- 義大利

- 西班牙

- 奧地利

- 德國

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 菲律賓

- 日本

- 韓國

- 澳洲

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 伊朗

- 阿拉伯聯合大公國

- 奈及利亞

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第9章:公司簡介

- AO Smith

- Ariston Holding

- Babcock & Wilcox Enterprises

- BDR Thermea Group

- Bosch Industriekessel

- Bradford White Corporation

- BURNHAM COMMERCIAL BOILERS

- Cleaver-Brooks

- Daikin

- FERROLI

- FONDITAL

- Hoval

- Immergas

- Lochinvar

- Remeha

- Vaillant Group

- VIESSMANN

- Weil-McLain

The Global Commercial Gas Fired Boiler Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 20.6 billion by 2034, driven by evolving heating needs across sectors and the continued push for smarter, more efficient building systems. The increasing use of Internet of Things (IoT) in boiler systems enables remote monitoring, real-time performance optimization, and predictive maintenance, reducing downtime and cutting operational costs. The sector benefits from hydrogen blending innovations, with leading manufacturers designing advanced models to accommodate dynamic heating demands. These efforts aim to support cleaner energy transitions while maintaining performance reliability.

A rise in demand for modular heating systems is transforming how large campuses, corporate offices, and commercial facilities approach energy use. The continued expansion of sectors like biotechnology, pharmaceuticals, and data infrastructure has pushed for precision heating solutions that offer reliability and adaptability. In response to supply chain uncertainties and shifting trade regulations, boiler manufacturers invest in domestic production to enhance supply responsiveness and reduce geopolitical risks. For instance, earlier tariff implementations on metals significantly impacted manufacturing economics, motivating companies to localize operations and diversify component sourcing strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $20.6 Billion |

| CAGR | 7.7% |

Systems rated at <= 10 MMBTU/hr are expected to maintain a strong growth trajectory, expanding at a CAGR of 7.5% through 2034. These compact, high-efficiency solutions are well-suited for space-constrained environments such as educational institutions, retail outlets, healthcare facilities, and hospitality buildings. Their scalability and lower upfront and maintenance costs offer a cost-effective way to deliver consistent heating without compromising performance or emissions standards.

The commercial office segment is projected to reach USD 3.5 billion by 2034, fueled by increased demand for intelligent, energy-efficient heating systems in line with modern sustainability benchmarks. Organizations are adopting condensing boilers and ultra-low NOx technology not only to meet compliance requirements but also to enhance operational efficiency. Integration with building automation systems is becoming more common, allowing facility managers to control heating loads and reduce energy waste.

United States Commercial Gas Fired Boiler Market generated USD 284.7 million in 2024, driven by the nationwide infrastructure modernization efforts and stricter environmental mandates reducing greenhouse gas emissions. Commercial buildings-especially aging structures in need of heating upgrades-are switching to advanced boiler systems that support higher thermal efficiency and digital integration. Government incentives and regional regulations encouraging clean energy adoption have also contributed to the increased replacement of conventional systems with high-performance gas-fired alternatives.

Leading manufacturers such as BDR Thermea Group, Lochinvar, Viessmann, Ariston Holding, Bosch Industriekessel, Weil-McLain, Bradford White Corporation, A.O. Smith, Burnham Commercial, Daikin, Vaillant Group, FERROLI, FONDITAL, Immergas, Remeha, Hoval, Cleaver-Brooks, and Babcock & Wilcox are adopting key strategies to stay competitive. These include expanding smart product lines, boosting R&D in hydrogen-ready models, improving customer support systems, and building regional manufacturing hubs to increase delivery speed and reduce costs while meeting sustainability targets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 10 MMBTU/hr

- 5.3 > 10 - 50 MMBTU/hr

- 5.4 > 50 - 100 MMBTU/hr

- 5.5 > 100 - 250 MMBTU/hr

- 5.6 > 250 MMBTU/hr

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Condensing

- 6.3 Non-condensing

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Offices

- 7.3 Healthcare facilities

- 7.4 Educational institutions

- 7.5 Lodgings

- 7.6 Retail stores

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 UK

- 8.3.3 Poland

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Germany

- 8.3.8 Sweden

- 8.3.9 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Philippines

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Australia

- 8.4.7 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Iran

- 8.5.3 UAE

- 8.5.4 Nigeria

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 A.O. Smith

- 9.2 Ariston Holding

- 9.3 Babcock & Wilcox Enterprises

- 9.4 BDR Thermea Group

- 9.5 Bosch Industriekessel

- 9.6 Bradford White Corporation

- 9.7 BURNHAM COMMERCIAL BOILERS

- 9.8 Cleaver-Brooks

- 9.9 Daikin

- 9.10 FERROLI

- 9.11 FONDITAL

- 9.12 Hoval

- 9.13 Immergas

- 9.14 Lochinvar

- 9.15 Remeha

- 9.16 Vaillant Group

- 9.17 VIESSMANN

- 9.18 Weil-McLain

組合式鍋爐市場:2026-2032年全球市場預測(依產品類型、燃料類型、技術、容量、最終用戶和分銷管道分類)

組合式鍋爐市場:2026-2032年全球市場預測(依產品類型、燃料類型、技術、容量、最終用戶和分銷管道分類) 2026年全球公用鍋爐市場報告煤粉煤炭氣化市場:依氧源、應用、終端用戶產業、營運壓力、工廠容量和煤炭類型分類,全球預測,2026-2032年

2026年全球公用鍋爐市場報告煤粉煤炭氣化市場:依氧源、應用、終端用戶產業、營運壓力、工廠容量和煤炭類型分類,全球預測,2026-2032年 鍋爐市場機會、成長要素、產業趨勢分析及2026-2035年預測。

鍋爐市場機會、成長要素、產業趨勢分析及2026-2035年預測。 2026-2030年全球冷凝式燃氣鍋爐市場

2026-2030年全球冷凝式燃氣鍋爐市場 全球暖氣鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球燃氣低溫商用鍋爐市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球暖氣鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球燃氣低溫商用鍋爐市場規模、佔有率、趨勢和成長分析報告:2026-2034年全球鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本鍋爐市場規模、佔有率、趨勢和預測:按鍋爐類型、最終用戶和地區分類,2026-2034年

日本鍋爐市場規模、佔有率、趨勢和預測:按鍋爐類型、最終用戶和地區分類,2026-2034年 2026-2030年全球鍋爐冷凝器市場

2026-2030年全球鍋爐冷凝器市場