|

市場調查報告書

商品編碼

1750488

纖維素奈米晶體與奈米纖維市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cellulose Nanocrystals and Nanofibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

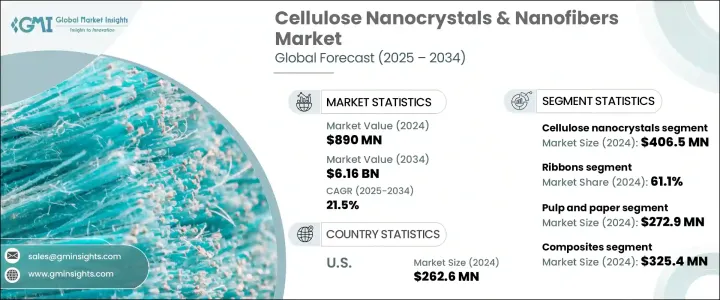

2024年,全球纖維素奈米晶體和奈米纖維市場價值為8.9億美元,預計2034年將以21.5%的複合年成長率成長,達到61.6億美元。這得益於產業對再生、可生物分解材料日益成長的需求,這些材料可作為石油基產品的永續替代品。奈米纖維素源自木漿和農業廢棄物,正成為眾多旨在減少碳足跡並採取環保做法的行業的誘人選擇。這些植物性奈米材料不僅具有環保效益,還具備卓越的功能性,能夠滿足複合材料、電子、醫療器材和綠色包裝等新興應用的性能需求。

材料科學的持續進步將纖維素奈米材料的性能推向了新的領域。其高抗張強度、高剛性、低熱膨脹性,以及優異的阻隔性能(例如耐油和耐氧性),使其適用於要求嚴苛的應用場景。各行各業也正在轉向多功能配方,使材料集抗菌保護、耐熱性甚至導電性於一體。這些不斷發展的特性使其在航太、建築、電子和生命科學等領域獲得了更廣泛的商業應用。監管支持力度的增強以及公眾對永續替代品日益成長的需求,持續推動該領域的廣泛創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 8.9億美元 |

| 預測值 | 61.6億美元 |

| 複合年成長率 | 21.5% |

纖維素奈米晶體細分市場在2024年創造了4.065億美元的收入,預計到2034年複合年成長率將達到22.1%。其透過酸水解獲得的高度結晶結構,具有優異的增強性能。這些特性使CNC成為高級塗料、薄膜和結構複合材料的理想選擇。另一方面,透過機械或酵素製程生產的纖維素奈米纖維具有柔韌性,非常適合用於包裝、過濾和個人護理產品。其網路結構在保持生物分解性的同時,也具有耐久性,為注重環保性能的終端市場增添了價值。

2024年,紙漿和造紙細分市場佔市場佔有率的2.729億美元,預計複合年成長率為22.4%。該細分市場將持續利用奈米纖維素的輕質、堅固和可堆肥特性。奈米纖維素在永續包裝中的應用與消費品和工業領域對可生物分解替代品日益成長的需求相契合。企業擴大在紙張塗層、阻隔層和模塑包裝解決方案中採用纖維素奈米材料,以減少對塑膠的依賴,同時保持產品的耐用性和性能。隨著一次性塑膠監管的收緊,食品、飲料和零售業對標籤、包裝和容器中基於奈米纖維素的替代品的需求持續成長。

2024年,美國纖維素奈米晶體和奈米纖維市場價值達2.626億美元,預計到2034年將以20.9%的複合年成長率成長。這一成長得益於創新中心、研究合作以及電子、醫療保健和永續包裝領域的應用。雄厚的聯邦研究資金、大學與私人企業之間的戰略合作夥伴關係以及向循環經濟模式的轉變,共同推動著這一領域的發展。美國市場擁有強大的技術商業化生態系統,受益於醫療設備、智慧包裝和軟性電子基板領域的早期應用,從而在奈米纖維素創新領域保持全球領先地位。

Sappi Limited、日本製紙株式會社、Borregaard ASA、CelluForce Inc. 和 American Process Inc. 等主要公司正在透過擴建研發設施、開發可擴展的生產流程以及與終端產業建立策略合作夥伴關係來鞏固其市場地位。這些公司正在投資下一代配方和大量生產,以滿足全球市場不斷變化的需求,並推動具有成本效益的商業化。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 市場定義與演變

- 川普政府關稅的影響—結構化概述

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計資料(HS 編碼) 註:以上貿易統計僅提供重點國家。

- 主要出口國

- 國家 1

- 國家 2

- 國家 3

- 主要進口國

- 國家 1

- 國家 2

- 國家 3

- 主要出口國

- 產業價值鏈分析

- 原料格局與供應鏈動態

- 原料分析

- 永續採購實踐

- 供應鏈挑戰與解決方案

- 定價分析和成本結構

- 生產成本分析

- 定價趨勢

- 降低成本策略

- 技術格局

- 萃取和生產技術

- 機械方法

- 化學方法

- 酶促方法

- 綜合方法

- 表徵技術

- 技術進步與創新

- 萃取和生產技術

- 市場動態

- 市場促進因素

- 對永續材料的需求不斷成長

- 卓越的機械性能和阻隔性能

- 增加研發投入

- 政府法規有利於生物基材料

- 市場限制

- 生產成本高

- 可擴展性挑戰

- 處理中的技術限制

- 來自傳統材料的競爭

- 市場機會

- 醫療保健和電子領域的新興應用

- 表面改質技術的進展

- 與其他奈米材料的整合

- 尚未開發的區域市場

- 市場挑戰

- 標準化問題

- 分散性和相容性挑戰

- 濕氣敏感性

- 監管障礙

- 市場促進因素

- 監管框架和標準

- 區域監管機構

- 認證和品質標準

- 環境法規的影響

- 創新與永續發展舉措

- 循環經濟一體化

- 減少碳足跡策略

- 廢棄物價值化方法

- PESTEL分析

- 波特五力分析

- 永續性和 ESG 分析

第4章:競爭格局

- 市佔率分析

- 主要利害關係人和策略定位

- 公司市場定位及熱圖分析

- 競爭策略和策略舉措

- 合併、收購和合作

- 新產品發布和創新

- 投資和融資場景

- 新創企業生態系統分析

- 專利分析與智慧財產權格局

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 纖維素奈米晶體(CNC)

- 硫酸化CNCs

- 羧化CNCs

- 磷酸化CNCs

- 其他改裝的CNC

- 纖維素奈米纖維(CNF)

- 機械纖維化的CNF

- TEMPO氧化CNF

- 酵素預處理的CNF

- 其他改性CNF

- 細菌奈米纖維素(BNC)

- 纖維素奈米原纖維(CNF)

- 其他奈米纖維素產品

第6章:市場估計與預測:按來源,2021 - 2034 年

- 主要趨勢

- 木頭

- 軟木

- 硬木

- 非木質植物來源

- 農業殘留物

- 棉布

- 麻

- 亞麻

- 其他植物來源

- 細菌合成

- 藻類和被囊動物

- 回收資源

- 廢紙

- 紡織廢料

- 其他回收資源

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 複合材料

- 聚合物基複合材料

- 水泥複合材料

- 其他複合材料

- 紙張和包裝

- 紙張增強

- 阻隔膜

- 食品包裝

- 其他包裝應用

- 塗料和薄膜

- 光學薄膜

- 阻隔塗層

- 抗菌塗層

- 其他塗料

- 生物醫學和製藥

- 藥物輸送系統

- 傷口癒合材料

- 組織工程支架

- 其他生物醫學應用

- 電子和感測器

- 軟性電子產品

- 生物感測器

- 儲能設備

- 其他電子應用

- 流變改質劑

- 石油和天然氣應用

- 油漆和塗料

- 個人護理產品

- 其他流變學應用

- 過濾和分離

- 氣凝膠和泡沫

- 其他應用

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 紙漿和造紙

- 包裝

- 食品和飲料

- 醫療保健和製藥

- 電子與光電子

- 汽車和運輸

- 建築和建築材料

- 紡織品和服裝

- 個人護理和化妝品

- 石油和天然氣

- 油漆、塗料和黏合劑

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Celluforce

- American Process Inc.

- Borregaard

- Nippon Paper Industries Co., Ltd.

- Stora Enso

- UPM-Kymmene Oyj

- Sappi Limited

- Kruger Inc.

- Daicel Corporation

- Weidmann Fiber Technology

- Melodea Ltd.

- Blue Goose Biorefineries Inc.

- Oji Holdings Corporation

- VTT Technical Research Centre of Finland

- FPInnovations

- Cellucomp Ltd.

- Forest Products Laboratory (FPL)

- Nanografi Nano Technology

- Asahi Kasei Corpo

The Global Cellulose Nanocrystals and Nanofibers Market was valued at USD 890 million in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 6.16 billion by 2034, driven by increasing industry demand for renewable, biodegradable materials that serve as sustainable alternatives to petroleum-based products. Nanocellulose, derived from wood pulp and agricultural residues, is becoming an attractive choice for multiple industries aiming to reduce their carbon footprint and adopt eco-conscious practices. These plant-based nanomaterials not only offer environmental benefits but also deliver superior functionality that supports the performance needs of emerging applications in composites, electronics, medical devices, and green packaging.

Ongoing advances in material science have pushed the capabilities of cellulose nanomaterials into new territories. Their high tensile strength, stiffness, and low thermal expansion, combined with impressive barrier properties-such as oil and oxygen resistance-make them suitable for demanding use cases. Industries are also turning to multifunctional formulations, where the material integrates antimicrobial protection, heat resistance, and even conductivity. These evolving features lead to broader commercial adoption across sectors like aerospace, construction, electronics, and life sciences. Supportive regulatory momentum and growing public pressure for sustainable alternatives continue to drive widespread innovation in this space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $890 Million |

| Forecast Value | $6.16 Billion |

| CAGR | 21.5% |

Cellulose nanocrystals segment generated USD 406.5 million in 2024 and is expected to witness a CAGR of 22.1% through 2034. Their highly crystalline structure, obtained through acid hydrolysis, provides excellent reinforcement capabilities. These properties make CNCs ideal for advanced coatings, films, and structural composites. On the other hand, cellulose nanofibers-produced through mechanical or enzymatic processes-offer flexibility and are well-suited for packaging, filtration, and personal care products. Their network-forming structure supports durability while maintaining biodegradability, adding value in end-use markets focused on eco-friendly performance.

The pulp and paper segment accounted for USD 272.9 million of the market in 2024 and is projected to grow at a CAGR of 22.4%. This segment continues to leverage nanocellulose for its lightweight, strong, and compostable nature. Its application in sustainable packaging aligns with the rising demand for biodegradable alternatives across consumer and industrial sectors. Companies are increasingly adopting cellulose nanomaterials in paper coatings, barrier layers, and molded packaging solutions to reduce reliance on plastics while maintaining durability and performance. As regulations tighten around single-use plastics, demand for nanocellulose-based alternatives in labeling, wrapping, and containers continues to rise across food, beverage, and retail industries.

United States Cellulose Nanocrystals and Nanofibers Market was valued at USD 262.6 million in 2024 and is projected to grow at a 20.9% CAGR through 2034. This growth is supported by innovation hubs, research collaborations, and applications in electronics, healthcare, and sustainable packaging. Strong federal research funding, strategic partnerships between universities and private firms, and a shift toward circular economy models fuel development. With a robust ecosystem for technology commercialization, the U.S. market benefits from early adoption across medical devices, smart packaging, and flexible electronic substrates, helping it maintain a leading position globally in nanocellulose innovation.

Key companies such as Sappi Limited, Nippon Paper Industries Co., Ltd., Borregaard ASA, CelluForce Inc., and American Process Inc. are strengthening their market position by expanding R&D facilities, developing scalable production processes, and forming strategic partnerships across end-use industries. These players are investing in next-gen formulations and high-volume production to meet the evolving needs of global markets and drive cost-effective commercialization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Market definition and evolution

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.1 Price transmission to end markets

- 3.2.2.2 Market share dynamics

- 3.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

- 3.4 Industry value chain analysis

- 3.5 Raw material landscape and supply chain dynamics

- 3.5.1 Feedstock analysis

- 3.5.2 Sustainable sourcing practices

- 3.5.3 Supply chain challenges and solutions

- 3.6 Pricing analysis and cost structure

- 3.6.1 Production cost analysis

- 3.6.2 Pricing trends

- 3.6.3 Cost reduction strategies

- 3.7 Technology landscape

- 3.7.1 Extraction and production technologies

- 3.7.1.1 Mechanical methods

- 3.7.1.2 Chemical methods

- 3.7.1.3 Enzymatic methods

- 3.7.1.4 Combined approaches

- 3.7.2 Characterization techniques

- 3.7.3 Technological advancements and innovations

- 3.7.1 Extraction and production technologies

- 3.8 Market dynamics

- 3.8.1 Market drivers

- 3.8.1.1 Growing demand for sustainable materials

- 3.8.1.2 Superior mechanical and barrier properties

- 3.8.1.3 Increasing R&D investments

- 3.8.1.4 Government regulations favoring bio-based materials

- 3.8.2 Market restraints

- 3.8.2.1 High production costs

- 3.8.2.2 Scalability challenges

- 3.8.2.3 Technical limitations in processing

- 3.8.2.4 Competition from conventional materials

- 3.8.3 Market opportunities

- 3.8.3.1 Emerging applications in healthcare and electronics

- 3.8.3.2 Advancements in surface modification techniques

- 3.8.3.3 Integration with other nanomaterials

- 3.8.3.4 Untapped regional markets

- 3.8.4 Market challenges

- 3.8.4.1 Standardization issues

- 3.8.4.2 Dispersion and compatibility challenges

- 3.8.4.3 Moisture sensitivity

- 3.8.4.4 Regulatory hurdles

- 3.8.1 Market drivers

- 3.9 Regulatory framework and standards

- 3.9.1 Regional regulatory landscape

- 3.9.2 Certification and quality standards

- 3.9.3 Environmental regulations impact

- 3.10 Innovation and sustainability initiatives

- 3.10.1 Circular economy integration

- 3.10.2 Carbon footprint reduction strategies

- 3.10.3 Waste valorization approaches

- 3.11 PESTEL analysis

- 3.12 Porter's five forces analysis

- 3.13 Sustainability and ESG analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Key stakeholders and strategic positioning

- 4.3 Company market positioning and heat map analysis

- 4.4 Competitive strategies and strategic initiatives

- 4.5 Mergers, acquisitions, and collaborations

- 4.6 New product launches and innovations

- 4.7 Investment and funding scenario

- 4.8 Start-up ecosystem analysis

- 4.9 Patent analysis and intellectual property landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cellulose nanocrystals (CNCs)

- 5.2.1 Sulfated CNCs

- 5.2.2 Carboxylated CNCs

- 5.2.3 Phosphorylated CNCs

- 5.2.4 Other Modified CNCs

- 5.3 Cellulose nanofibers (CNFs)

- 5.3.1 Mechanically fibrillated CNFs

- 5.3.2 TEMPO-oxidized CNFs

- 5.3.3 Enzymatically pretreated CNFs

- 5.3.4 Other modified CNFs

- 5.4 Bacterial nanocellulose (BNC)

- 5.5 Cellulose nanofibrils (CNF)

- 5.6 Other nanocellulose products

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Wood

- 6.2.1 Softwood

- 6.2.2 Hardwood

- 6.3 Non-wood plant sources

- 6.3.1 Agricultural residues

- 6.3.2 Cotton

- 6.3.3 Hemp

- 6.3.4 Flax

- 6.3.5 Other plant sources

- 6.4 Bacterial synthesis

- 6.5 Algae and tunicates

- 6.6 Recycled sources

- 6.6.1 Paper waste

- 6.6.2 Textile waste

- 6.6.3 Other recycled sources

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Composites

- 7.2.1 Polymer matrix composites

- 7.2.2 Cement composites

- 7.2.3 Other composites

- 7.3 Paper and packaging

- 7.3.1 Paper strengthening

- 7.3.2 Barrier films

- 7.3.3 Food packaging

- 7.3.4 Other packaging applications

- 7.4 Coatings and films

- 7.4.1 Optical films

- 7.4.2 Barrier coatings

- 7.4.3 Antimicrobial coatings

- 7.4.4 Other coatings

- 7.5 Biomedical and pharmaceutical

- 7.5.1 Drug delivery systems

- 7.5.2 Wound healing materials

- 7.5.3 Tissue engineering scaffolds

- 7.5.4 Other biomedical applications

- 7.6 Electronics and sensors

- 7.6.1 Flexible electronics

- 7.6.2 Biosensors

- 7.6.3 Energy storage devices

- 7.6.4 Other electronic applications

- 7.7 Rheology modifiers

- 7.7.1 Oil and gas applications

- 7.7.2 Paints and coatings

- 7.7.3 Personal care products

- 7.7.4 Other rheological applications

- 7.8 Filtration and separation

- 7.9 Aerogels and foams

- 7.10 Other applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pulp and paper

- 8.3 Packaging

- 8.4 Food and beverage

- 8.5 Healthcare and pharmaceuticals

- 8.6 Electronics and optoelectronics

- 8.7 Automotive and transportation

- 8.8 Construction and building materials

- 8.9 Textiles and apparel

- 8.10 Personal care and cosmetics

- 8.11 Oil and gas

- 8.12 Paints, coatings, and adhesives

- 8.13 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Celluforce

- 10.2 American Process Inc.

- 10.3 Borregaard

- 10.4 Nippon Paper Industries Co., Ltd.

- 10.5 Stora Enso

- 10.6 UPM-Kymmene Oyj

- 10.7 Sappi Limited

- 10.8 Kruger Inc.

- 10.9 Daicel Corporation

- 10.10 Weidmann Fiber Technology

- 10.11 Melodea Ltd.

- 10.12 Blue Goose Biorefineries Inc.

- 10.13 Oji Holdings Corporation

- 10.14 VTT Technical Research Centre of Finland

- 10.15 FPInnovations

- 10.16 Cellucomp Ltd.

- 10.17 Forest Products Laboratory (FPL)

- 10.18 Nanografi Nano Technology

- 10.19 Asahi Kasei Corpo

奈米纖維素市場:按類型、原料、形態、應用和最終用途產業分類-2026-2032年全球市場預測

奈米纖維素市場:按類型、原料、形態、應用和最終用途產業分類-2026-2032年全球市場預測 3D列印奈米纖維素市場:策略性洞察與預測(2026-2031年)奈米纖維素市場:策略性洞察與預測(2026-2031年)

3D列印奈米纖維素市場:策略性洞察與預測(2026-2031年)奈米纖維素市場:策略性洞察與預測(2026-2031年) 微纖化纖維素市場:依生產流程、應用和地區分類纖維素奈米晶體市場:按類型、原料、形態、製造流程、應用、終端用戶產業分類,全球預測(2026-2032年)

微纖化纖維素市場:依生產流程、應用和地區分類纖維素奈米晶體市場:按類型、原料、形態、製造流程、應用、終端用戶產業分類,全球預測(2026-2032年) 奈米纖維素在複合材料和塗料領域的市場:機會、成長動力、產業趨勢分析和預測(2026-2035年)

奈米纖維素在複合材料和塗料領域的市場:機會、成長動力、產業趨勢分析和預測(2026-2035年) 日本奈米纖維素市場報告(按產品類型(奈米原纖化纖維素、奈米晶纖維素、細菌纖維素、微纖化纖維素及其他)、應用和地區分類,2026-2034年)奈米纖維素市場機會、成長要素、產業趨勢分析及2026年至2035年預測

日本奈米纖維素市場報告(按產品類型(奈米原纖化纖維素、奈米晶纖維素、細菌纖維素、微纖化纖維素及其他)、應用和地區分類,2026-2034年)奈米纖維素市場機會、成長要素、產業趨勢分析及2026年至2035年預測 全球奈米纖維素市場(至 2035 年):依奈米纖維素、應用、分銷管道、地區、產業趨勢和預測

全球奈米纖維素市場(至 2035 年):依奈米纖維素、應用、分銷管道、地區、產業趨勢和預測 纖維素奈米晶體增強生物聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

纖維素奈米晶體增強生物聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)