|

市場調查報告書

商品編碼

1750280

機器人放射治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Robotic Radiotherapy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

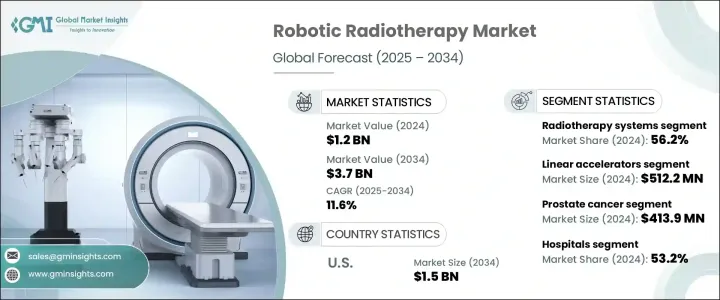

2024年,全球機器人放射治療市場規模達12億美元,預計年複合成長率將達11.6%,到2024年將達到37億美元,這得益於各類腫瘤和癌症對精準放射治療的日益依賴。機器人放射治療能夠提高標靶精準度,進而改善治療效果並減少療程。隨著對非侵入性和門診癌症治療的需求不斷成長,機器人系統因其無需手術或住院即可提供高劑量放射治療的能力而日益受到青睞。這反映出腫瘤治療途徑正朝著價值導向護理和更短復健期的方向發展。

即時影像、運動補償和人工智慧規劃軟體的前沿進展進一步推動了機器人放射治療技術的普及。這些系統可根據患者本身的運動或腫瘤轉移自動調整放射治療劑量,以達到一致、精準的劑量控制。醫療機構更傾向於使用機器人設備來治療位於精細解剖區域的腫瘤,而不會損害附近的健康組織。追求更少的治療療程(即所謂的低分割治療)也推動了這些系統的普及。因此,越來越多的醫護人員和患者選擇結合即時監測、光束調製和智慧影像引導治療的機器人平台。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 37億美元 |

| 複合年成長率 | 11.6% |

2024年,機器人放射治療市場中的放射治療系統佔了56.2%的佔有率。其先進的標靶能力,提供亞毫米級的精度,已成為治療重要器官附近或難以觸及區域的腫瘤不可或缺的工具。透過顯著減少對周圍健康組織的輻射暴露,這些系統改變了臨床醫生處理複雜癌症病例的方式。它們與腫瘤學實踐的整合提高了患者的治療效果和安全性,鞏固了其作為下一代癌症治療標準的地位。

同時,直線加速器 (LINAC) 細分市場在 2024 年創造了 5.122 億美元的市場規模。這些機器人驅動的設備支援影像導引和調強放射治療,可根據腫瘤的動態位置提供高度適形的劑量。其自適應計劃功能對於肺部或肝臟等移動器官中的腫瘤尤其有用,因為這些器官中的腫瘤會因呼吸或消化而頻繁移動。此外,LINAC 在門診癌症治療的應用也日益增多,這使得治療時間更短、更便捷,從而最大限度地減少住院時間並提高患者舒適度。

美國機器人放射治療市場在2024年創收5.083億美元,預計2034年將成長至15億美元。癌症盛行率的上升,尤其是在老年人口中,加劇了對精準高效治療方案的需求。醫院和癌症中心正在增加對機器人平台的投資,以提供恢復時間更短、併發症更少的非侵入性治療。這種以患者為中心的轉變,更傾向於個人化和有針對性的放射治療,持續推動全球技術的應用。

全球機器人放射治療市場的主要參與者優先考慮創新、策略合作和地理擴張,以鞏固其市場地位。 Accuray 和 Elekta 正在大力投資以人工智慧為基礎的治療計劃和自適應治療系統。西門子醫療和通用電氣醫療正在推動整合影像和機器人平台,以提高精準度。 RefleXion 和 ViewRay 正在利用即時腫瘤追蹤來差異化其產品。瓦里安、Brainlab 和日立繼續增強軟體驅動功能,並在新興市場獲得監管部門的批准。聯合影像和 ZAP 正在擴大生產規模以滿足全球日益成長的需求,三菱電機和 Mevion 則專注於經濟實惠和緊湊的系統設計,以開拓中端醫療保健市場。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 全球癌症發生率不斷上升

- 非侵入性和門診治療方法的偏好日益成長

- 成像和運動追蹤技術的進步

- 醫療投資和政府對腫瘤治療基礎設施的資助不斷增加

- 產業陷阱與挑戰

- 機器人放射治療系統和維護成本高昂

- 缺乏熟練的專業人員來操作先進的機器人系統

- 成長動力

- 成長潛力分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 未來市場趨勢

- 監管格局

- 專利分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 競爭市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 放射治療系統

- 3D相機

- 軟體

- 其他產品

第6章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 直線加速器

- 立體定位放射治療系統

- 射波刀

- 伽瑪刀

- 粒子治療

- 質子束治療

- 重離子束治療

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 攝護腺癌

- 乳癌

- 肺癌

- 頭頸癌

- 大腸直腸癌

- 其他應用

第8章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 癌症治療中心

- 學術和研究機構

- 專科診所

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Accuray

- Brainlab

- Elekta

- GE Healthcare

- Hitachi

- Ion Beam Applications

- Mevion

- Mitsubishi Electric

- RefleXion

- Shinva

- Siemens Healthineers

- United Imaging

- Varian

- ViewRay

- ZAP

The Global Robotic Radiotherapy Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 3.7 billion by 2024, driven by the increasing reliance on precision-driven radiation therapies for various tumors and cancers. Robotic radiotherapy enables enhanced targeting accuracy, leading to better treatment outcomes and reduced therapy sessions. As demand for non-invasive and outpatient cancer treatments grows, robotic systems are gaining favor for their ability to deliver high-dose radiation without the need for surgery or hospitalization. This reflects a broader shift toward value-based care and shorter recovery periods in oncology treatment pathways.

Cutting-edge advances in real-time imaging, motion compensation, and AI-powered planning software are further fueling the adoption of robotic radiotherapy technologies. These systems automatically adapt radiation delivery to patient-specific movement or tumor shifts, enabling consistent, accurate dosing. Facilities prefer robotic equipment to treat tumors in delicate anatomical regions without harming nearby healthy tissue. The push for fewer treatment sessions, known as hypofractionation, is also contributing to the popularity of these systems. As a result, both healthcare providers and patients are increasingly opting for robotic platforms that combine real-time monitoring, beam modulation, and smart image-guided therapy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 11.6% |

In 2024, the radiotherapy systems segment in the robotic radiotherapy market held a 56.2% share. Their advanced targeting capabilities, offering sub-millimeter precision, have become indispensable in treating tumors located near vital organs or in hard-to-reach areas. By significantly reducing radiation exposure to surrounding healthy tissue, these systems have transformed the way clinicians manage complex cancer cases. Their integration into oncology practices has elevated patient outcomes and safety profiles, solidifying their role as a standard in next-generation cancer treatment.

Meanwhile, linear accelerators (LINACs) segment generated USD 512.2 million in 2024. These robotic-enabled devices support image-guided and intensity-modulated radiotherapy, delivering highly conformal doses tailored to dynamic tumor positions. Their adaptive planning features are especially valuable for tumors in mobile organs such as the lungs or liver, where breathing or digestion introduces frequent positional shifts. Additionally, LINACs are increasingly utilized in outpatient cancer care, allowing for shorter, more convenient treatment sessions that minimize hospital stays and maximize patient comfort.

U.S. Robotic Radiotherapy Market generated USD 508.3 million in 2024 and is projected to grow to USD 1.5 billion by 2034. Rising cancer prevalence-especially in an aging population-has intensified the need for precise, efficient treatment solutions. Hospitals and cancer centers are expanding investments in robotic platforms to offer non-invasive therapies with reduced recovery times and fewer complications. This patient-centric shift, favoring customized and targeted radiation approaches, continues to fuel technology adoption worldwide.

Key players in the Global Robotic Radiotherapy Market prioritize innovation, strategic collaborations, and geographic expansion to solidify their market standing. Accuray and Elekta are investing heavily in AI-based treatment planning and adaptive therapy systems. Siemens Healthineers and GE Healthcare are advancing integrated imaging and robotic platforms to boost precision. RefleXion and ViewRay are leveraging real-time tumor tracking to differentiate their offerings. Varian, Brainlab, and Hitachi continue to enhance software-driven functionalities and secure regulatory approvals in emerging markets. United Imaging and ZAP are scaling up production to meet growing demand globally, Mitsubishi Electric and Mevion focus on affordability and compact system design to tap mid-tier healthcare segments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cancer worldwide

- 3.2.1.2 Growing preference for non-invasive and outpatient treatment methods

- 3.2.1.3 Technological advancements in imaging and motion tracking

- 3.2.1.4 Rising healthcare investments and government funding in oncology care infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of robotic radiotherapy systems and maintenance

- 3.2.2.2 Lack of skilled professionals to operate advanced robotic systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Patent analysis

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Radiotherapy systems

- 5.3 3D cameras

- 5.4 Software

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Linear accelerators

- 6.3 Stereotactic radiation therapy systems

- 6.4 Cyberknife

- 6.5 Gamma knife

- 6.6 Particle therapy

- 6.7 Proton beam therapy

- 6.8 Heavy ion beam therapy

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prostate cancer

- 7.3 Breast cancer

- 7.4 Lung cancer

- 7.5 Head and neck cancer

- 7.6 Colorectal cancer

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Cancer treatment centers

- 8.4 Academic and research institutions

- 8.5 Specialty clinics

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Mexico

- 9.5.2 Brazil

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Accuray

- 10.2 Brainlab

- 10.3 Elekta

- 10.4 GE Healthcare

- 10.5 Hitachi

- 10.6 Ion Beam Applications

- 10.7 Mevion

- 10.8 Mitsubishi Electric

- 10.9 RefleXion

- 10.10 Shinva

- 10.11 Siemens Healthineers

- 10.12 United Imaging

- 10.13 Varian

- 10.14 ViewRay

- 10.15 ZAP