|

市場調查報告書

商品編碼

1741044

陶瓷電容器市場機會、成長動力、產業趨勢分析及2025-2034年預測Ceramic Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

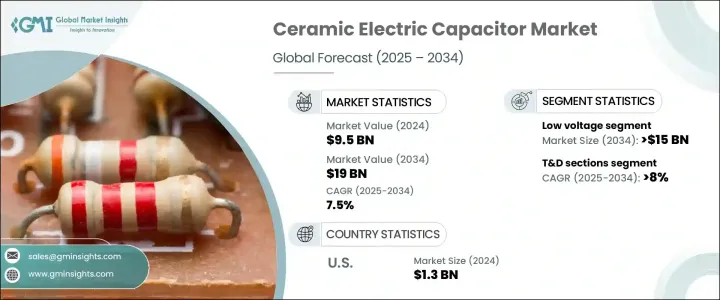

2024年,全球陶瓷電容器市場規模達95億美元,預計年複合成長率將達7.5%,2034年將達到190億美元。這得益於電容器在日益廣泛的電子應用中的日益普及、電力基礎設施投資的增加以及其在現代儲能系統中的重要作用。隨著電容器在新興技術、智慧電子產品和不斷發展的能源生態系統中的重要性日益凸顯,市場正在經歷顯著的變化。隨著電子產業快速朝向小型化和高性能方向發展,對可靠性、效率和高頻耐受性更高的陶瓷電容器的需求也不斷攀升。

電動車的日益普及、5G 和 6G 等新一代通訊網路的推出以及再生能源電網的擴張,大大提升了對先進電容器技術的需求。隨著各行各業對數位化和永續能源管理的關注,陶瓷電容器正處於創新的核心地位,在關鍵應用中提升效率、穩定性和緊湊性。各公司正積極投資研發,以充分利用新材料、更智慧的製造流程以及符合全球脫碳目標的環保生產技術的優勢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 95億美元 |

| 預測值 | 190億美元 |

| 複合年成長率 | 7.5% |

隨著對緊湊型高性能設備的需求不斷成長,小型化和增強電容性能正成為該行業的重要趨勢。製造商正在設計更小但更有效率的電容器,以在嚴苛條件下保持高性能。電動車和下一代通訊技術的普及,持續推動對能夠支援高頻、高溫運作且不影響穩定性或性能的元件的需求。

消費性電子、汽車系統和工業自動化領域的持續投資推動了市場穩步擴張。為了實現成本效益和高輸出性能,各公司正在採用新型介電材料,並開發支援智慧電網、先進電源管理和節能系統的電容器。永續發展的趨勢正在重塑製造實踐,推動產業優先考慮環保工藝和材料。隨著全球對再生能源系統的需求不斷成長,電容器在維持電壓穩定、減少能量損耗和最佳化配電系統方面變得越來越重要。

預計到2034年,低壓陶瓷電容器市場規模將達到150億美元,這得歸功於人們日益關注材料科學和生產創新,旨在提高這些元件的可靠性、效率和使用壽命。陶瓷成分和電極設計的進步有助於滿足下一代電子設備對緊湊外形和在各種操作環境下保持穩定性能的要求。

預計到2034年,輸配電 (T&D) 領域將以8%的複合年成長率成長。隨著全球電網的發展,電容器在維持電能品質、支援負載平衡以及穩定變電站和配電系統的電壓方面發揮著至關重要的作用。除了能源基礎設施外,隨著資料中心、物聯網系統和互聯設備對穩定、高效能元件的需求激增,通訊和科技產業也為市場成長做出貢獻。向數位基礎設施的轉變以及再生能源的整合,持續提升新建和升級系統中對陶瓷電容器的需求。

2024年,美國陶瓷電容器市場規模將達到13億美元,這得益於電信、汽車、工業電子和消費性電子等快速發展的產業對緊湊型高效元件日益成長的需求。 5G基礎設施的擴張、電動車產量的上升以及智慧家庭和穿戴式裝置的普及,使得陶瓷電容器因其優異的溫度穩定性、可靠性和小型化潛力而受到越來越多的依賴。

全球陶瓷電容器市場的主要參與者包括 Vishay Intertechnology, Inc.、三星電機、WIMA GmbH & Co. KG、松下公司、村田製作所、京瓷 AVX Components Corporation、Xuansn Capacitor、施耐德電氣、Cornell Dubilier、ELNA CO., LTD.、太陽誘電株式會社 .K.D.k.T. Corporation, 4AB Corporation, PTD 公司、太陽電株式會。公司正在採取以創新、區域擴張和垂直整合為中心的策略以保持競爭力。許多公司正在大力投資研發先進的介電材料,以支援在較小的封裝中實現更高的電容。策略合作和收購使製造商能夠獲得尖端技術和更廣泛的客戶群。製造商也在擴大其全球生產能力,以服務當地市場並降低供應鏈風險。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 川普政府關稅對貿易和整體產業的影響

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:按電壓,2021 - 2034

- 主要趨勢

- 低的

- 中等的

- 高的

第6章:市場規模及預測:依最終用途,2021-2034

- 主要趨勢

- 消費性電子產品

- 汽車

- 通訊與科技

- 輸配電

- 其他

第7章:市場規模及預測:依地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 奧地利

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第8章:公司簡介

- ABB

- Cornell Dubilier

- ELNA CO., LTD.

- Havells India Ltd.

- KEMET Corporation

- KYOCERA AVX Components Corporation

- Murata Manufacturing Co., Ltd.

- Panasonic Corporation

- SAMSUNG ELECTRO-MECHANICS

- Schneider Electric

- Siemens

- TAIYO YUDEN CO., LTD.

- TDK Corporation

- Vishay Intertechnology, Inc.

- WIMA GmbH & Co. KG

- Xuansn Capacitor

The Global Ceramic Electric Capacitor Market was valued at USD 9.5 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 19 billion by 2034, fueled by the rising integration of capacitors into an expanding range of electronic applications, greater investment in electrical infrastructure, and their vital role in modern energy storage systems. The market is witnessing a notable transformation as capacitors become increasingly crucial across emerging technologies, smart electronics, and evolving energy ecosystems. With the electronics industry rapidly advancing toward miniaturization and higher performance, the demand for ceramic capacitors offering greater reliability, efficiency, and high-frequency tolerance is scaling new heights.

Growing adoption of electric vehicles, rollout of next-gen communication networks like 5G and 6G, and expansion of renewable energy grids are significantly enhancing the need for advanced capacitor technologies. As industries focus on digitization and sustainable energy management, ceramic capacitors stand at the center of innovation, driving efficiency, stability, and compactness in critical applications. Companies are aggressively investing in research and development to leverage the benefits of new materials, smarter manufacturing processes, and eco-friendly production technologies that align with global decarbonization goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $19 Billion |

| CAGR | 7.5% |

As the demand for compact, high-performance devices rises, miniaturization and enhanced capacitance capabilities are becoming essential industry trends. Manufacturers are responding by designing smaller yet more efficient capacitors that maintain high functionality under demanding conditions. The adoption of electric vehicles and next-generation communication technologies continues to boost the need for components that can support high-frequency, high-temperature operations without compromising stability or performance.

Continued investment in consumer electronics, automotive systems, and industrial automation contributes to the market's steady expansion. With a focus on achieving cost-efficient, high-output performance, companies are adopting new dielectric materials and developing capacitors that support smart grids, advanced power management, and energy-efficient systems. The move toward sustainability is reshaping manufacturing practices, pushing the industry to prioritize eco-friendly processes and materials. As the global demand for renewable energy systems grows, capacitors are becoming increasingly critical for maintaining voltage stability, reducing energy loss, and optimizing power distribution systems.

The low-voltage ceramic capacitors segment is expected to reach USD 15 billion by 2034, driven by the rising focus on materials science and production innovation aimed at increasing the reliability, efficiency, and longevity of these components. Advancements in ceramic compositions and electrode designs are helping meet the demands of next-generation electronic devices that require compact form factors and consistent performance across wide operating environments.

The transmission and distribution (T&D) segment is projected to grow at a CAGR of 8% through 2034. As global power grids evolve, capacitors play a vital role in maintaining power quality, supporting load balancing, and stabilizing voltage in substations and distribution systems. Alongside energy infrastructure, the communication and tech industries contribute to market growth as demand surges for stable, high-performance components in data centers, IoT systems, and connected devices. The shift toward digital infrastructure and the integration of renewable energy sources continue to elevate the need for ceramic capacitors in new and upgraded systems.

The United States Ceramic Electric Capacitor Market generated USD 1.3 billion in 2024, driven by the increasing demand for compact, high-efficiency components in rapidly evolving industries such as telecommunications, automotive, industrial electronics, and consumer technology. The expansion of 5G infrastructure, rising production of electric vehicles, and the proliferation of smart home and wearable devices contribute to greater reliance on ceramic capacitors due to their excellent temperature stability, reliability, and miniaturization potential.

Key players in the Global Ceramic Electric Capacitor Market include Vishay Intertechnology, Inc., SAMSUNG ELECTRO-MECHANICS, WIMA GmbH & Co. KG, Panasonic Corporation, Murata Manufacturing Co., Ltd., KYOCERA AVX Components Corporation, Xuansn Capacitor, Schneider Electric, Cornell Dubilier, ELNA CO., LTD., TAIYO YUDEN CO., LTD., TDK Corporation, Siemens, ABB, Havells India Ltd., and KEMET Corporation. Companies are adopting strategies centered on innovation, regional expansion, and vertical integration to stay competitive. Many are investing heavily in R&D to develop advanced dielectric materials that support higher capacitance in smaller packages. Strategic collaborations and acquisitions enable access to cutting-edge technologies and broader customer bases. Manufacturers are also expanding their global production capabilities to serve local markets and reduce supply chain risk.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Impact of Trump administration tariffs on trade & overall industry

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034, ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034, ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Communications & technology

- 6.5 Transmission & distribution

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Cornell Dubilier

- 8.3 ELNA CO., LTD.

- 8.4 Havells India Ltd.

- 8.5 KEMET Corporation

- 8.6 KYOCERA AVX Components Corporation

- 8.7 Murata Manufacturing Co., Ltd.

- 8.8 Panasonic Corporation

- 8.9 SAMSUNG ELECTRO-MECHANICS

- 8.10 Schneider Electric

- 8.11 Siemens

- 8.12 TAIYO YUDEN CO., LTD.

- 8.13 TDK Corporation

- 8.14 Vishay Intertechnology, Inc.

- 8.15 WIMA GmbH & Co. KG

- 8.16 Xuansn Capacitor

高壓電容器市場分析及預測(至2035年):類型、產品、應用、技術、組件、最終用戶、材質類型、功能、安裝類型

高壓電容器市場分析及預測(至2035年):類型、產品、應用、技術、組件、最終用戶、材質類型、功能、安裝類型 2026年全球軸向引線電容器市場報告

2026年全球軸向引線電容器市場報告 全球雙電層電容器市場(按類型、電壓範圍、應用和分銷管道分類)預測(2026-2032年)雙電層電容器隔膜市場:2026-2032年全球預測(依產品類型、材質、厚度範圍及最終用途產業分類)

全球雙電層電容器市場(按類型、電壓範圍、應用和分銷管道分類)預測(2026-2032年)雙電層電容器隔膜市場:2026-2032年全球預測(依產品類型、材質、厚度範圍及最終用途產業分類) 家用電子電器產品用高壓電容器市場:機會、成長要素、產業趨勢分析及2026年至2035年預測

家用電子電器產品用高壓電容器市場:機會、成長要素、產業趨勢分析及2026年至2035年預測 全球低壓電容器市場全球高壓電容器市場中壓電力電容器市場機會、成長動力、產業趨勢分析及2025-2034年預測高壓電力電容器市場機會、成長動力、產業趨勢分析及2025-2034年預測全球電容器市場

全球低壓電容器市場全球高壓電容器市場中壓電力電容器市場機會、成長動力、產業趨勢分析及2025-2034年預測高壓電力電容器市場機會、成長動力、產業趨勢分析及2025-2034年預測全球電容器市場