|

市場調查報告書

商品編碼

1740886

汽車充氣式避震器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Gas Charged Shock Absorber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

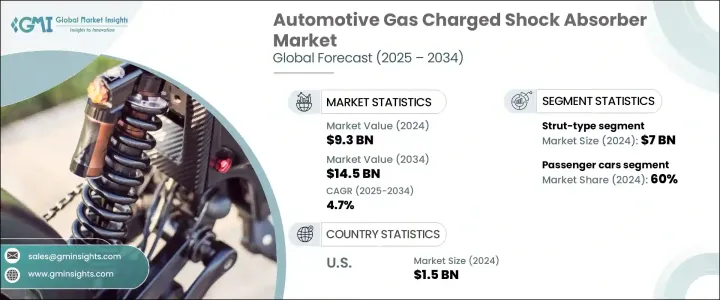

2024年,全球汽車充氣避震器市場規模達93億美元,預計2034年將以4.7%的複合年成長率成長,達到145億美元。這得益於消費者對更高乘坐舒適度、更卓越的車輛操控性以及更安全的多地形駕駛體驗的期望不斷提升。隨著汽車製造商持續轉向先進的懸吊系統,對充氣減震器等高性能零件的需求日益成長。這些減震器在減少振動、增強車輛穩定性和提供更平穩的駕駛體驗方面發揮關鍵作用,尤其是在高速和越野條件下。

隨著汽車技術的不斷發展,消費者如今期望他們的車輛兼具舒適性和性能,這使得先進的減震系統成為汽車工程的重中之重。高階汽車市場的全球擴張、日益嚴重的城市交通堵塞以及長途駕駛習慣的興起,共同推動了對更高效減震管理系統的需求。充氣式減震器相較於傳統液壓減震器具有至關重要的優勢,它能夠有效防止空氣進入和起泡,確保車輛在持續或激烈駕駛下始終保持性能穩定。隨著汽車產業日益向電氣化和智慧車輛系統靠攏,這些避震器正被客製化以支援動態負載,同時不影響能源效率或電池續航里程。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 93億美元 |

| 預測值 | 145億美元 |

| 複合年成長率 | 4.7% |

隨著注重性能的汽車平台(尤其是SUV和跨界車)的快速普及,充氣式減震器正成為乘用車和商用車的標準部件。它們能夠提供卓越的阻尼效率,並在各種負載和條件下保持最佳平衡,使其成為當今懸吊系統中不可或缺的一部分。這些避震器的設計旨在滿足消費者日益成長的需求,即提升操控性、減少車身側傾、改善俯仰控制以及提升整體駕駛體驗。汽車製造商正在將充氣式減震器整合到新車型中,以創造差異化的性能特徵,並滿足消費者對卓越駕乘體驗的需求。這種日益成長的偏好在城市和鄉村地區尤其明顯,因為這些地區的路況和駕駛預期差異很大,這進一步證明了充氣式減震系統的多功能性。

受個人汽車保有量成長、可支配收入增加以及中產階級人口不斷壯大的推動,乘用車市場將在2024年佔據60%的主導佔有率。消費者更重視舒適性、穩定性和操控性,尤其是在日常通勤和長途旅行中。在汽車銷售蓬勃發展的新興經濟體中,隨著消費者尋求能夠提供無縫駕駛體驗的車輛,對高階懸吊零件的關注度也日益提升。充氣式避震器憑藉更佳的阻尼特性滿足了這項需求,使其成為追求舒適性、操控性和安全性的現代汽車平台的首選。

按安裝類型分類,支柱式充氣避震器市場領先,2024 年估值達 70 億美元。此類部件因其整合結構(將螺旋彈簧和減震器整合為一個緊湊單元)而被廣泛採用。這種結構有助於提高前懸吊佈局的空間效率,並有助於減輕車輛總重,從而提高燃油效率並降低排放。此外,該設計還易於安裝和維護,使支柱式減震器成為大規模汽車製造的經濟高效的解決方案。

2024年,北美汽車充氣避震器市場規模達15億美元,預計2025年至2034年期間的複合年成長率將達到4.9%。這一成長得益於該地區強勁的汽車產量、大型原始設備製造商的佈局,以及消費者對皮卡和跨界車等大型車輛日益成長的需求,這些車輛需要高耐用性的懸吊系統。該地區的電氣化進程也推動了對先進減震器的需求,這些減震器不僅符合現代動力傳動系統的要求,還能減輕車輛重量並提高能源效率。

日立Astemo、HL Mando、Gabriel India、KYB、昭和、採埃孚、Chassis Brakes、Endurance Technologies、Cofap和天納克等領先公司正透過創新和策略合作積極鞏固其市場地位。這些公司正在大力投資研發,以提高減震器性能,擴大其全球生產佈局,並與原始設備製造商建立重要的合作關係。許多公司還透過開發基於道路反饋和駕駛行為提供即時自適應能力的電子控制減震系統來豐富其產品線,以適應智慧和自動駕駛汽車的未來發展。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 組件提供者

- 製造商

- 技術提供者

- 配銷通路分析

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 對貿易的影響

- 技術與創新格局

- 專利分析

- 監管格局

- 成本細分分析

- 價格趨勢

- 地區

- 車輛

- 重要新聞和舉措

- 衝擊力

- 成長動力

- 對乘坐舒適性和操控穩定性的需求日益成長

- 電動和混合動力車的普及率不斷上升

- 懸吊系統的技術進步

- 全球汽車生產的擴張

- 產業陷阱與挑戰

- 與液壓減震器相比成本更高

- 嚴格的環境和安全法規

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 雙管氣體

- 單管氣體

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第7章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 支撐式

- 伸縮式

第8章:市場估計與預測:按銷售管道 2021 - 2034

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AL-KO Fahrzeugtechnik

- Bilstein

- Chassis Brakes

- Cofap

- Endurance

- Gabriel

- Hitachi Astemo

- ITW

- Jiangsu Huachuan

- KYB

- Liuzhou Shuangfei

- Magneti Marelli

- Mando

- Ride Control

- S&T Motiv

- Showa

- Tenneco

- Tokico

- YSS Suspension

- ZF Friedrichshafen

The Global Automotive Gas Charged Shock Absorber Market was valued at USD 9.3 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 14.5 billion by 2034, supported by rising consumer expectations for enhanced ride comfort, superior vehicle handling, and safer driving experiences across diverse terrains. As automakers continue to shift toward advanced suspension systems, the demand for high-performance components like gas-charged shock absorbers is gaining significant traction. These absorbers play a key role in reducing vibrations, enhancing vehicle stability, and delivering smoother rides, especially in high-speed and off-road conditions.

With evolving automotive technologies, consumers now expect their vehicles to offer both comfort and performance, which has placed advanced damping systems at the forefront of vehicle engineering. The global expansion of premium vehicle segments, growing urban traffic congestion, and a surge in long-distance driving habits are collectively fueling the need for better shock management systems. Gas-charged shock absorbers provide a crucial advantage over traditional hydraulic shocks by offering resistance to aeration and foaming, which ensures consistent performance under continuous or aggressive driving. As the automotive sector leans more into electrification and smart vehicle systems, these absorbers are being tailored to support dynamic loads without compromising energy efficiency or battery range.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $14.5 Billion |

| CAGR | 4.7% |

With the rapid adoption of performance-focused vehicle platforms, particularly SUVs and crossovers, gas-charged shock absorbers are becoming a standard component in both passenger and commercial vehicle categories. Their ability to deliver advanced damping efficiency and maintain optimal balance under varying loads and conditions makes them indispensable in today's suspension systems. These shock absorbers are engineered to meet the growing consumer need for better handling, reduced body roll, improved pitch control, and overall smoother rides. Automakers are integrating gas-charged absorbers into newer models to differentiate performance features and meet the demand for premium ride quality. This growing preference is evident in both urban and rural settings, where road conditions and driving expectations vary significantly, further validating the versatility of gas-charged systems.

The passenger vehicle segment commanded a dominant 60% share in 2024, driven by the increasing rate of personal car ownership, rising disposable incomes, and an expanding middle-class demographic. Consumers are prioritizing vehicles that offer improved comfort, stability, and handling-particularly for daily commutes and longer journeys. In emerging economies, where car sales are booming, the focus on premium suspension components is intensifying as buyers look for vehicles that deliver a seamless driving experience. Gas-charged shock absorbers meet this demand by providing better damping characteristics, making them a preferred choice in modern vehicle platforms aimed at comfort, control, and safety.

Based on mounting type, strut-type gas charged shock absorbers led the market with a valuation of USD 7 billion in 2024. These components are widely adopted due to their integrated construction, which combines the coil spring and shock absorber into one compact unit. This configuration supports space efficiency in front suspension layouts and helps reduce the vehicle's overall weight, contributing to fuel efficiency and lower emissions. The design also offers ease of installation and simplified maintenance, making strut-type shock absorbers a cost-effective solution for large-scale automotive manufacturing.

The North America Automotive Gas Charged Shock Absorber Market accounted for USD 1.5 billion in 2024 and is projected to grow at a CAGR of 4.9% from 2025 to 2034. This growth is backed by strong regional vehicle production, the presence of major OEMs, and a rising preference for larger vehicles like pickups and crossovers that demand high-durability suspension systems. The region's push toward electrification is also boosting demand for advanced shock absorbers that align with modern drivetrain requirements while supporting weight reduction and energy efficiency.

Leading companies such as Hitachi Astemo, HL Mando, Gabriel India, KYB, Showa, ZF Friedrichshafen, Chassis Brakes, Endurance Technologies, Cofap, and Tenneco are actively strengthening their market positions through innovation and strategic collaborations. These players are investing heavily in R&D to enhance shock absorber performance, expand their manufacturing footprint globally, and form key partnerships with OEMs. Many are also diversifying their offerings by developing electronically controlled damping systems that provide real-time adaptability based on road feedback and driving behavior, aligning with the future of smart and autonomous vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Price trend

- 3.7.1 Region

- 3.7.2 Vehicle

- 3.8 Key news & initiatives

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing demand for ride comfort & handling stability

- 3.9.1.2 Rising adoption of electric and hybrid vehicles

- 3.9.1.3 Technological advancements in suspension systems

- 3.9.1.4 Expansion of global automotive production

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Higher cost compared to hydraulic shock absorbers

- 3.9.2.2 Stringent environmental & safety regulations

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Twin-tube gas

- 5.3 Monotube gas

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Mount, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Strut-type

- 7.3 Telescopic

Chapter 8 Market Estimates & Forecast, By Sales Channel 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AL-KO Fahrzeugtechnik

- 10.2 Bilstein

- 10.3 Chassis Brakes

- 10.4 Cofap

- 10.5 Endurance

- 10.6 Gabriel

- 10.7 Hitachi Astemo

- 10.8 ITW

- 10.9 Jiangsu Huachuan

- 10.10 KYB

- 10.11 Liuzhou Shuangfei

- 10.12 Magneti Marelli

- 10.13 Mando

- 10.14 Ride Control

- 10.15 S&T Motiv

- 10.16 Showa

- 10.17 Tenneco

- 10.18 Tokico

- 10.19 YSS Suspension

- 10.20 ZF Friedrichshafen

減震器市場:依設計、銷售管道、車輛類型和地區分類

減震器市場:依設計、銷售管道、車輛類型和地區分類 汽車充氣避震器市場規模、佔有率、成長分析(按安裝類型、技術、車輛類型和地區)—2025 年至 2032 年產業預測

汽車充氣避震器市場規模、佔有率、成長分析(按安裝類型、技術、車輛類型和地區)—2025 年至 2032 年產業預測 機械阻尼器 - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

機械阻尼器 - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 汽車減震器市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)

汽車減震器市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032) 汽車售後避震器市場(按車輛類型、產品類型、核心類型、分銷管道、最終用戶、懸吊類型、技術和價格分佈)——2025-2032年全球預測汽車減震器市場按懸吊類型、車輛類型、分銷管道、設計和位置分類-2025-2032年全球預測汽車減震器市場按車輛類型、產品類型、銷售管道和分銷管道分類-2025-2032年全球預測

汽車售後避震器市場(按車輛類型、產品類型、核心類型、分銷管道、最終用戶、懸吊類型、技術和價格分佈)——2025-2032年全球預測汽車減震器市場按懸吊類型、車輛類型、分銷管道、設計和位置分類-2025-2032年全球預測汽車減震器市場按車輛類型、產品類型、銷售管道和分銷管道分類-2025-2032年全球預測 點吸收器市場-全球產業規模、佔有率、趨勢、機會和預測,按吸收器類型、應用、營運環境、地區、競爭進行細分,2020-2030F

點吸收器市場-全球產業規模、佔有率、趨勢、機會和預測,按吸收器類型、應用、營運環境、地區、競爭進行細分,2020-2030F 汽車減震器市場預測至2032年:按類型、車輛類型、銷售管道、懸吊類型、應用和地區進行的全球分析

汽車減震器市場預測至2032年:按類型、車輛類型、銷售管道、懸吊類型、應用和地區進行的全球分析 2025年全球汽車避震器市場報告

2025年全球汽車避震器市場報告