|

市場調查報告書

商品編碼

1740804

自感應奈米複合材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Self-Sensing Nanocomposites Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

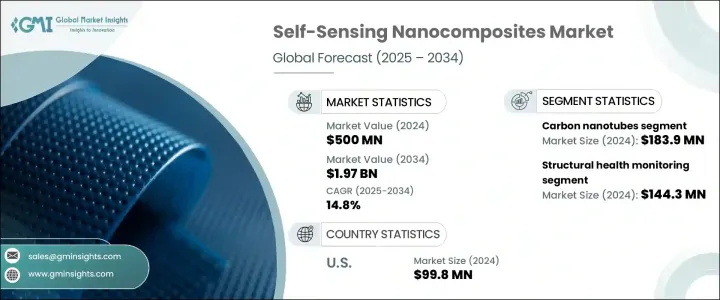

2024年,全球自感應奈米複合材料市場價值5億美元,預計到2034年將以14.8%的複合年成長率成長,達到19.7億美元。對智慧材料日益成長的需求正在重塑各行各業,尤其是基礎設施和航太領域,即時資料監控和性能評估在這些領域至關重要。這些先進的複合材料能夠檢測並響應其結構內部的變化,使其成為關鍵系統的理想選擇。它們無需外部感測器即可進行自我監控並提供持續回饋,這使得它們在高度依賴精度、可靠性和早期故障檢測的行業中越來越受歡迎。

嵌入式奈米複合材料正被整合到聚合物、塗層和混凝土中,使這些材料能夠感知並記錄內部發生的變化。這種能力推動了它們在需要持續追蹤結構完整性的高效能應用中的應用。結構健康監測 (SHM) 解決方案的重要性日益提升,提升了自感知奈米複合材料的作用,這種複合材料旨在即時向操作員發出系統漏洞警報。同時,隨著人們對生物醫學領域的興趣日益濃厚,市場動態也在發生變化,其應用範圍也擴展到穿戴式醫療技術。目前,人們正在探索將這些奈米複合材料應用於輕巧的攜帶式醫療設備,這些設備旨在追蹤生命徵象、檢測異常並傳輸資料進行遠端評估。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5億美元 |

| 預測值 | 19.7億美元 |

| 複合年成長率 | 14.8% |

根據所用奈米粒子的類型,自傳式奈米複合材料可分為不同類型的類型,每種類型都具有獨特的性能特徵。其中,碳奈米管引領市場,2024 年其價值為 1.839 億美元。預計該細分市場在 2025 年至 2034 年期間的複合年成長率將達到 13.6%。碳奈米管以其強導電性而聞名,由於其高精度和高耐用性,被廣泛用於應力和應變感測。石墨烯和氧化石墨烯等其他材料因其巨大的表面積和卓越的電響應性而日益受到關注,從而增強了跨多個平台的感測能力。

氧化鋅 (ZnO) 和二氧化鈦 (TiO2) 等金屬氧化物因其獨特的結構和響應特性,在熱感測、光感和磁感測領域備受關注。對於成本敏感的應用,炭黑是一種受歡迎的選擇,它能夠在不影響預算的情況下提供有效的電感。同時,奈米黏土、量子點和混合填料方面的創新正在為需要增強選擇性或響應性的利基應用鋪平道路。

自傳式奈米複合材料可根據感測機制進一步分類,包括電感、熱感、光感、磁感和聲感。電感引領市場,其廣泛應用於基礎設施、軟性電子產品和需要持續即時回饋的汽車系統。其他機制正在高級應用中發揮作用。磁感對於無損檢測和導航系統正變得越來越重要,而聲感測正成為一種檢測振動系統內部故障的有前景的新興方法。

按應用分類,市場包括結構健康監測、損傷檢測與修復、應力和應變監測、溫度感測、壓力感測和其他用途。 2024 年,結構健康監測細分市場的價值為 1.443 億美元,預計在 2025 年至 2034 年期間的複合年成長率為 16%,佔 28.8% 的市場佔有率。這種主導地位是由於迫切需要對建築物、隧道和橋樑的結構狀況進行準確、即時的評估。應力和應變監測以及損傷檢測在汽車和航太等性能和安全至關重要的領域越來越重要。同時,能源、電子和醫療保健等產業對溫度和壓力感測應用的需求不斷成長,這些產業對環境精度至關重要。

終端用途細分包括建築和基礎設施、汽車和航太、醫療保健、電子電氣、能源和電力以及其他行業。目前,大部分需求來自建築和汽車行業,這些材料有助於提高安全性、耐用性和即時監控。然而,醫療保健(尤其是穿戴式診斷)和智慧型裝置應用電子產品的日益融合,正在持續推動市場多元化。此外,能源和電力等行業正在採用這些材料來支援管道和發電系統中的高級故障檢測。

在美國,自感應奈米複合材料市場在2024年的價值為9,980萬美元,預計在2025-2034年期間的複合年成長率將達到15.3%。這一成長得益於美國蓬勃發展的航太和汽車行業,以及學術界和工業界對下一代材料的投資。

亞太地區目前憑藉著快速的工業化進程、基礎設施建設以及對智慧材料的強勁需求,引領全球市場。該地區各國受益於較低的生產成本和熟練的勞動力,使其成為自感應奈米複合材料的主要生產國和消費國。

市場領導者包括 Integran Technologies、Cabot Corporation、OCSiAl、Nanoco Group plc 和 Zyvex Technologies。這些公司透過持續創新、產品組合多元化以及跨核心產業的策略合作夥伴關係,維持著強大的市場地位。他們對永續性和客製化的關注,使其能夠滿足新興利基應用和主流需求,同時加強全球供應鏈和客戶關係。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 主要出口國

- 主要進口國

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 基礎設施和航太領域對智慧材料的需求不斷成長。

- 結構健康監測系統的發展。

- 穿戴式醫療感測器的使用日益增多。

- 物聯網感測網路的擴展

- 產業陷阱與挑戰

- 奈米複合材料的生產和加工成本高。

- 大規模製造能力有限。

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依奈米顆粒類型,2021-2034

- 主要趨勢

- 碳奈米管

- 石墨烯和氧化石墨烯

- 金屬氧化物

- 炭黑

- 其他

第6章:市場估計與預測:依感測機制,2021-2034 年

- 主要趨勢

- 電感

- 熱感應

- 光學感

- 磁感應

- 聲學感

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 結構健康監測

- 損傷檢測與修復

- 應力和應變監測

- 溫度感測

- 壓力感

- 其他

第8章:市場估計與預測:按最終用途產業,2021-2034 年

- 主要趨勢

- 建築與基礎設施

- 汽車與航太

- 衛生保健

- 電學

- 能源與電力

- 其他

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Cabot Corporation

- Nanoco Group plc

- Anisoprint 3D Printing Technology Limited Company

- OCSiAl

- Integran Technologies

- Platonic Nanotech

- AdNano Technologies Pvt Ltd

- Zyvex Technologies

- Mechnano

The Global Self-Sensing Nanocomposites Market was valued at USD 500 million in 2024 and is estimated to grow at a CAGR of 14.8% to reach USD 1.97 billion by 2034. Increasing demand for intelligent materials is reshaping industries, particularly infrastructure and aerospace, where real-time data monitoring and performance assessment have become essential. These advanced composites are capable of detecting and responding to changes within their structure, making them ideal for use in critical systems. Their ability to self-monitor and provide continuous feedback without external sensors has made them increasingly popular in sectors that rely heavily on precision, reliability, and early fault detection.

Embedded nanocomposite materials are being integrated into polymers, coatings, and concrete, allowing these materials to sense and log changes as they occur internally. This capability is driving their use in high-performance applications where structural integrity must be continuously tracked. The growing importance of structural health monitoring (SHM) solutions has elevated the role of self-sensing nanocomposites, which are designed to alert operators of system vulnerabilities in real time. At the same time, market dynamics are shifting as interest grows in the biomedical field, with applications expanding into wearable healthcare technologies. These nanocomposites are now being explored for use in lightweight, portable health devices designed to track vital signs, detect abnormalities, and transmit data for remote evaluations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $500 Million |

| Forecast Value | $1.97 Billion |

| CAGR | 14.8% |

Different types of self-sensing nanocomposites are classified based on the type of nanoparticles used, each offering distinct performance characteristics. Among these, carbon nanotubes led the market and were valued at USD 183.9 million in 2024. This segment is anticipated to grow at a CAGR of 13.6% from 2025 to 2034. Known for their strong conductive properties, carbon nanotubes are widely used for stress and strain sensing due to their high precision and durability. Other materials such as graphene and graphene oxide are gaining traction thanks to their expansive surface area and superior electrical responsiveness, which enhance sensing capabilities across multiple platforms.

Metal oxides like ZnO and TiO2 are gaining attention for their functionality in thermal, optical, and magnetic sensing, due to their unique structural and responsive traits. For cost-sensitive applications, carbon black is a popular option, offering effective electrical sensing without compromising budget. Meanwhile, innovations involving nanoclays, quantum dots, and hybrid fillers are paving the way for niche applications where enhanced selectivity or responsiveness is necessary.

Self-sensing nanocomposites are further categorized based on sensing mechanisms including electrical, thermal, optical, magnetic, and acoustic sensing. Electrical sensing leads the market, supported by its widespread use in infrastructure, flexible electronics, and automotive systems that require consistent, real-time feedback. Other mechanisms are finding roles in advanced applications. Magnetic sensing is becoming increasingly vital for non-destructive testing and navigation systems, while acoustic sensing is emerging as a promising approach for detecting internal faults in systems that emit vibrations.

By application, the market includes structural health monitoring, damage detection and repair, stress and strain monitoring, temperature sensing, pressure sensing, and other uses. In 2024, the structural health monitoring segment was valued at USD 144.3 million and is set to grow at a CAGR of 16% between 2025 and 2034, holding a 28.8% share of the market. This dominance is due to the pressing need for accurate, real-time assessments of structural conditions in buildings, tunnels, and bridges. Stress and strain monitoring, along with damage detection, are gaining importance in sectors like automotive and aerospace, where performance and safety are top priorities. Meanwhile, temperature and pressure sensing applications are seeing rising demand from industries such as energy, electronics, and healthcare where environmental precision is critical.

The end-use segmentation includes construction and infrastructure, automotive and aerospace, healthcare, electronics and electricals, energy and power, and other industries. Most of the demand currently comes from the construction and automotive sectors, where these materials contribute to safety, durability, and real-time monitoring. However, growing integration in healthcare-particularly in wearable diagnostics-and in electronics for smart device applications continues to diversify the market. Additionally, industries such as energy and power are adopting these materials to support advanced fault detection in pipelines and power-generating systems.

In the United States, the self-sensing nanocomposites market was valued at USD 99.8 million in 2024 and is forecasted to grow at a CAGR of 15.3% during 2025-2034. This expansion is driven by the country's robust aerospace and automotive sectors, alongside academic and industrial investment in next-generation materials.

The Asia Pacific region currently leads the global market due to rapid industrialization, infrastructure development, and strong demand for smart materials. Countries across this region benefit from lower production costs and a skilled workforce, positioning them as major producers and consumers of self-sensing nanocomposites.

Leading players in the market include Integran Technologies, Cabot Corporation, OCSiAl, Nanoco Group plc, and Zyvex Technologies. These companies maintain strong market positions through continuous innovation, portfolio diversification, and strategic partnerships across core industries. Their focus on sustainability and customization has enabled them to address both emerging niche applications and mainstream requirements while strengthening global supply chains and customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for smart materials in infrastructure and aerospace.

- 3.7.1.2 Growth of structural health monitoring systems.

- 3.7.1.3 Increasing use in wearable healthcare sensors.

- 3.7.1.4 Expansion of IoT-enabled sensing networks

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High production and processing costs of nanocomposites.

- 3.7.2.2 Limited large-scale manufacturing capabilities.

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Nanoparticle Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carbon nanotubes

- 5.3 Graphene & graphene oxide

- 5.4 Metal oxides

- 5.5 Carbon black

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Sensing Mechanism, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Electrical sensing

- 6.3 Thermal sensing

- 6.4 Optical sensing

- 6.5 Magnetic sensing

- 6.6 Acoustic sensing

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Structural health monitoring

- 7.3 Damage detection & repair

- 7.4 Stress & strain monitoring

- 7.5 Temperature sensing

- 7.6 Pressure sensing

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & infrastructure

- 8.3 Automotive & aerospace

- 8.4 Healthcare

- 8.5 Electronics & electricals

- 8.6 Energy & power

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Cabot Corporation

- 10.2 Nanoco Group plc

- 10.3 Anisoprint 3D Printing Technology Limited Company

- 10.4 OCSiAl

- 10.5 Integran Technologies

- 10.6 Platonic Nanotech

- 10.7 AdNano Technologies Pvt Ltd

- 10.8 Zyvex Technologies

- 10.9 Mechnano

奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製造技術和應用分類-2026-2032年全球市場預測石墨烯奈米複合材料市場:2026-2032年全球市場預測(依聚合物基體、材料類型、產品形式、製造技術、終端用戶產業、應用與銷售管道)奈米黏土市場:2026-2032年全球市場預測(按奈米黏土的類型、形態、表面改質、應用和通路)

奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製造技術和應用分類-2026-2032年全球市場預測石墨烯奈米複合材料市場:2026-2032年全球市場預測(依聚合物基體、材料類型、產品形式、製造技術、終端用戶產業、應用與銷售管道)奈米黏土市場:2026-2032年全球市場預測(按奈米黏土的類型、形態、表面改質、應用和通路) 功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類

功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類 2026年全球奈米複合材料市場報告奈米結構陶瓷市場預測(至2032年):按類型、製造流程、特性、最終用戶和地區進行的全球分析

2026年全球奈米複合材料市場報告奈米結構陶瓷市場預測(至2032年):按類型、製造流程、特性、最終用戶和地區進行的全球分析 聚合物奈米複合材料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

聚合物奈米複合材料:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 全球航空電池用三元材料市場:按產品、應用和國家分析和預測(2025 年至 2034 年)

全球航空電池用三元材料市場:按產品、應用和國家分析和預測(2025 年至 2034 年)