|

市場調查報告書

商品編碼

1740793

嬰兒乾糧市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dried Baby Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

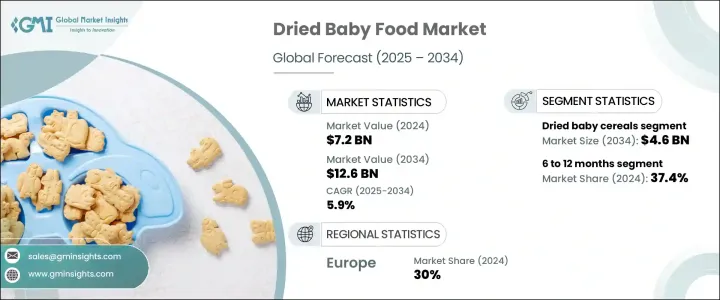

2024年,全球嬰兒乾糧市場規模達72億美元,預計到2034年將以5.9%的複合年成長率成長,達到126億美元,這得益於人們對易於準備且營養均衡的嬰兒食品日益成長的偏好。繁忙的生活方式、不斷成長的可支配收入以及父母對嬰兒健康的日益關注,正在推動已開發地區和發展中地區對嬰兒乾糧的需求。父母選擇嬰兒乾糧是因為它保存期限長、方便食用且營養豐富。該市場的歷史性擴張與人們對嬰兒營養的認知不斷演變息息相關,尤其是在城市中心,省時且安全的餵食方式至關重要。

隨著核心家庭和在職父母數量的增加,嬰兒食品的選擇也明顯轉向緊湊、方便攜帶。對於時間緊迫、注重營養和易用性的照顧者來說,便利性和便攜性已成為至關重要的因素。因此,製造商正專注於輕巧、可重複密封和一次性包裝,以無縫融入忙碌的生活方式。這些包裝形式減少了準備時間,最大限度地減少了浪費,並提高了衛生水平,使其成為現代育兒需求的理想選擇。有機、非基因改造和清潔標籤產品的趨勢正在重塑消費者的偏好,並支撐著全球市場的持續需求。家長對孩子食品的成分越來越謹慎,導致對透明原料採購和最低限度加工配方的需求激增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 72億美元 |

| 預測值 | 126億美元 |

| 複合年成長率 | 5.9% |

在產品類別中,預計到2034年,嬰兒乾米粉市場規模將達到46億美元,複合年成長率為6.1%,這得益於市場對強化、無過敏原、易消化、富含益生菌、維生素和必需礦物質的米粉的需求激增。如今,新配方專注於清潔成分和增強營養成分,以應對日益成長的兒童早期健康問題。市場見證了無麩質和有機食品的創新,以滿足特定的飲食需求。

根據年齡偏好,6至12個月大的嬰兒類別在2024年佔據最大佔有率,達到37.4%,預計到2034年將以6.5%的複合年成長率成長。嬰兒發育的這一階段需要引入更複雜的食物質地和營養成分,這推動了對方便、預先分配飲食的需求。可重複密封容器和一次性包裝袋等包裝創新使這些產品對在職父母來說更加實用。雙收入家庭的增加和即食產品的日益普及也是這一細分市場發展的驅動力。儘管市場正在擴張,但價格方面的擔憂可能會略微抑製成長,尤其是在對成本較為敏感的地區。

2024年,歐洲嬰兒乾糧市場佔最大佔有率,達30%,這得益於人們高度的營養意識和對嬰兒食品安全的監管支持。對優質和有機嬰兒食品的需求不斷成長,並持續影響該地區的產品發展。強勁的購買力以及歐洲家庭對清潔標籤產品的日益青睞也推動了市場擴張。除了強大的監管框架外,歐洲還受益於高購買力,這刺激了對高品質嬰兒食品的需求。

雅培實驗室、海恩天體集團、Sprout Foods Inc.、明治控股株式會社、雀巢公司、Hero Group、Holle Baby Food GmbH、Arla Foods amba、Ella's Kitchen Limited、Plum PBC、達能公司、菲仕蘭坎皮納、貝拉米培有機有限公司、Riri Baby Food Co. Ltd.、寶可本產品、卡夫米亨氏公司公司、Birnition?和喜寶國際等公司正積極提升市場佔有率。領先品牌正在投資產品多元化、永續採購和清潔標籤創新。許多品牌正在擴大有機產品線,與當地分銷商合作,並改進包裝以提升貨架吸引力。此外,各公司也正在增加數位互動和電商管道,以加強全球影響力並提升客戶便利性。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業回應

- 供應鏈重構

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 主要出口國

- 主要進口國

- 供應鏈和分銷分析

- 原物料採購

- 製造流程

- 脫水技術

- 冷凍乾燥方法

- 品質管制

- 包裝創新

- 永續包裝

- 智慧包裝

- 便利功能

- 分銷網路

- 傳統零售

- 電子商務

- 直接面對消費者

- 供應鏈挑戰

- 原物料供應情況

- 端對端品質控制

- 後勤

- 供應鏈最佳化

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 全球監管標準

- 區域指南

- FDA(美國)

- 歐洲食品安全局(歐盟)

- FSSAI(印度)

- 中國國家食品藥物管理局

- 其他區域法規

- 品質和安全標準

- 重金屬和污染物

- 營養需求

- 標籤和聲明

- 包裝安全

- 有機認證標準

- 監理挑戰與策略

- 未來監理趨勢

- 衝擊力

- 成長動力

- 女性勞動參與率上升

- 提高對嬰兒營養的認知

- 都市化和生活方式的改變

- 方便且保存期限更長

- 產業陷阱與挑戰

- 偏好自製嬰兒食品

- 嚴格的監管標準

- 新興市場的價格敏感度

- 供應鏈中斷

- 市場機會

- 有機和清潔標籤產品

- 強化功能性嬰兒乾糧

- 新興市場的擴張

- 電子商務與D2C模型

- 市場挑戰

- 重金屬污染問題

- 競爭定價壓力

- 消費者偏好的改變

- 永續性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 消費者行為與偏好

- 消費者人口統計

- 購買決策因素

- 營養價值

- 品牌信任

- 價格敏感度

- 方便

- 有機和天然成分

- 消費者購買模式

- 線上與線下

- 訂閱模式

- 大量購買

- 消費者意識和教育

- 文化和地域偏好

- 社群媒體和影響者的影響

- 技術創新和產品開發

- 加工技術

- 高級脫水

- 營養保存

- 清潔標籤方法

- 成分創新

- 超級食物

- 替代蛋白質

- 天然防腐劑

- 包裝創新

- 可生物分解/可堆肥材料

- 主動智慧包裝

- 份量控制

- 數位化整合

- QR 圖碼和可追溯性

- 行動應用程式

- 電子商務最佳化

- 研發與未來趨勢

- 加工技術

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 嬰兒乾麥片

- 嬰兒乾糧

- 嬰兒乾零食和手指食物

- 乾果和蔬菜泥

- 冷凍乾燥嬰兒食品

第6章:市場估計與預測:依來源,2021-2034

- 主要趨勢

- 有機的

- 傳統的

第7章:市場估計與預測:依年齡段,2021-2034

- 主要趨勢

- 4-6個月

- 6-12個月

- 12-24個月

- 24個月以上

第8章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 超市和大賣場

- 專賣店

- 便利商店

- 網路零售

- 藥局和藥局

- 其他

第9章:市場估計與預測:依包裝類型,2021-2034

- 主要趨勢

- 袋裝

- 罐子和瓶子

- 罐頭

- 盒子和紙箱

- 其他

第10章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Nestle SA

- Danone SA

- Abbott Laboratories

- Hero Group

- Mead Johnson Nutrition Company

- The Hain Celestial Group, Inc.

- HiPP International

- The Kraft Heinz Company

- Plum, PBC

- Ella's Kitchen Limited

- Gerber Products Company

- Sprout Foods, Inc.

- Beech-Nut Nutrition Corporation

- Bellamy's Organic Pty Ltd

- Arla Foods amba

- FrieslandCampina

- Meiji Holdings Co., Ltd.

- Topfer GmbH

- Holle Baby Food GmbH

- Riri Baby Food Co., Ltd.

The Global Dried Baby Food Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 5.9 % to reach USD 12.6 billion by 2034, driven by the increasing preference for easy-to-prepare and nutritionally balanced infant meals. Busy lifestyles, rising disposable incomes, and growing parental awareness about infant health are pushing demand across developed and developing regions. Parents choose dried baby food for its long shelf life, convenience, and nutritional value. The market's historic expansion can be linked to the evolving perception of baby nutrition, particularly in urban centers where time-saving and safe feeding options are critical.

With an increasing number of nuclear families and working parents, there's also a noticeable shift toward compact, travel-friendly food options for infants. Convenience and portability have become essential factors for time-constrained caregivers who prioritize both nutrition and ease of use. As a result, manufacturers are focusing on lightweight, resealable, and single-serve packaging that fits seamlessly into busy lifestyles. These formats reduce preparation time, minimize waste, and offer greater hygiene, making them ideal for modern parenting needs. The trend toward organic, non-GMO, and clean-label products is reshaping buyer preferences and supporting sustained demand across global markets. Parents are becoming increasingly cautious about what goes into their children's food, leading to a surge in demand for transparent ingredient sourcing and minimally processed formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 5.9% |

Among product categories, the dried baby cereals segment is expected to reach USD 4.6 billion by 2034, growing at a CAGR of 6.1% influenced by the surge in demand for fortified, allergen-free, and easily digestible cereals that contain probiotics, vitamins, and essential minerals. New formulations now focus on clean ingredients and enhanced nutritional profiles to address growing concerns about early childhood health. The market witness's innovation through gluten-free and organic options catering to specific dietary needs.

Based on age-based preferences, the 6 to 12-month category held the largest share in 2024 at 37.4% and is expected to grow at a 6.5% CAGR through 2034. This stage of infant development requires the introduction of more complex food textures and nutritional content, fueling demand for convenient, pre-portioned meals. Packaging innovation, such as resealable containers and single-use pouches, makes these products even more practical for working parents. The rise in dual-income households and the increasing popularity of ready-to-eat products are also driving forces in this segment. Although the market is expanding, pricing concerns may temper growth slightly, especially in more cost-sensitive regions.

Europe Dried Baby Food Market held the largest share of 30% in 2024, driven by high nutritional awareness and regulatory support for infant food safety. Increased demand for premium and organic baby food options continues to shape product development across the region. Market expansion is also supported by strong purchasing power and the rising popularity of clean-label offerings in European households. In addition to a strong regulatory framework, Europe benefits from high purchasing power, which fuels the demand for high-quality baby food products.

Companies such as Abbott Laboratories, The Hain Celestial Group, Sprout Foods Inc., Meiji Holdings Co. Ltd., Nestle S.A., Hero Group, Holle Baby Food GmbH, Arla Foods amba, Ella's Kitchen Limited, Plum PBC, Danone S.A., FrieslandCampina, Bellamy's Organic Pty Ltd, Riri Baby Food Co. Ltd., Gerber Products Company, The Kraft Heinz Company, Beech-Nut Nutrition Corporation, Topfer GmbH, and HiPP International are actively working to enhance market presence. Leading brands invest in product diversification, sustainable sourcing, and clean-label innovation. Many are expanding organic lines, partnering with local distributors, and enhancing packaging for greater shelf appeal. Additionally, companies are increasing digital engagement and e-commerce channels to strengthen global outreach and improve customer convenience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Supply Chain and Distribution Analysis

- 3.4.1 Raw Material Sourcing

- 3.4.2 Manufacturing Processes

- 3.4.2.1 Dehydration Technologies

- 3.4.2.2 Freeze-Drying Methods

- 3.4.2.3 Quality Control

- 3.4.3 Packaging Innovations

- 3.4.3.1 Sustainable Packaging

- 3.4.3.2 Smart Packaging

- 3.4.3.3 Convenience Features

- 3.4.4 Distribution Network

- 3.4.4.1 Traditional Retail

- 3.4.4.2 E-commerce

- 3.4.4.3 Direct-to-Consumer

- 3.4.5 Supply Chain Challenges

- 3.4.5.1 Raw Material Availability

- 3.4.5.2 End-to-End Quality Control

- 3.4.5.3 Logistics

- 3.4.6 Supply Chain Optimization

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 Global Regulatory Standards

- 3.7.2 Regional Guidelines

- 3.7.2.1 FDA (U.S.)

- 3.7.2.2 EFSA (EU)

- 3.7.2.3 FSSAI (India)

- 3.7.2.4 CFDA (China)

- 3.7.2.5 Other Regional Regulations

- 3.7.3 Quality and Safety Standards

- 3.7.3.1 Heavy Metals and Contaminants

- 3.7.3.2 Nutritional Requirements

- 3.7.3.3 Labeling and Claims

- 3.7.3.4 Packaging Safety

- 3.7.4 Organic Certification Standards

- 3.7.5 Regulatory Challenges and Strategies

- 3.7.6 Future Regulatory Trends

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising Female Workforce Participation

- 3.8.1.2 Increasing Awareness of Infant Nutrition

- 3.8.1.3 Urbanization and Changing Lifestyles

- 3.8.1.4 Convenience and Longer Shelf Life

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Preference for Homemade Baby Food

- 3.8.2.2 Stringent Regulatory Standards

- 3.8.2.3 Price Sensitivity in Emerging Markets

- 3.8.2.4 Supply Chain Disruptions

- 3.8.3 Market opportunities

- 3.8.3.1 Organic and Clean Label Products

- 3.8.3.2 Fortified and Functional Dried Baby Food

- 3.8.3.3 Expansion in Emerging Markets

- 3.8.3.4. E-commerce and D2 C Models

- 3.8.4 Market Challenges

- 3.8.4.1 Heavy Metal Contamination Concerns

- 3.8.4.2 Competitive Pricing Pressure

- 3.8.4.3 Changing Consumer Preferences

- 3.8.4.4 Sustainability Concerns

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer Behavior and Preferences

- 3.12.1 Consumer Demographics

- 3.12.2 Purchase Decision Factors

- 3.12.2.1 Nutritional Value

- 3.12.2.2 Brand Trust

- 3.12.2.3 Price Sensitivity

- 3.12.2.4 Convenience

- 3.12.2.5 Organic and Natural Ingredients

- 3.12.3 Consumer Buying Patterns

- 3.12.3.1 Online vs. Offline

- 3.12.3.2 Subscription Models

- 3.12.3.3 Bulk Purchases

- 3.12.4 Consumer Awareness and Education

- 3.12.5 Cultural and Regional Preferences

- 3.12.6 Impact of Social Media and Influencers

- 3.13 Technological Innovations and Product Development

- 3.13.1 Processing Technologies

- 3.13.1.1 Advanced Dehydration

- 3.13.1.2 Nutrient Preservation

- 3.13.1.3 Clean Label Methods

- 3.13.2 Ingredient Innovations

- 3.13.2.1 Superfoods

- 3.13.2.2 Alternative Proteins

- 3.13.2.3 Natural Preservatives

- 3.13.3 Packaging Innovations

- 3.13.3.1 Biodegradable/Compostable Materials

- 3.13.3.2 Active and Intelligent Packaging

- 3.13.3.3 Portion Control

- 3.13.4 Digital Integration

- 3.13.4.1 QR Codes and Traceability

- 3.13.4.2 Mobile Apps

- 3.13.4.3 E-commerce Optimization

- 3.13.5 R&D and Future Trends

- 3.13.1 Processing Technologies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dried baby cereals

- 5.3 Dried baby meals

- 5.4 Dried baby snacks and finger foods

- 5.5 Dried fruit and vegetable purees

- 5.6 Freeze-dried baby food

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Age Group, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 4–6 Months

- 7.3 6–12 Months

- 7.4 12–24 Months

- 7.5 Above 24 Months

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores

- 8.4 Convenience stores

- 8.5 Online retail

- 8.6 Pharmacies and drugstores

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Pouches

- 9.3 Jars and bottles

- 9.4 Cans

- 9.5 Boxes and cartons

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 Danone S.A.

- 11.3 Abbott Laboratories

- 11.4 Hero Group

- 11.5 Mead Johnson Nutrition Company

- 11.6 The Hain Celestial Group, Inc.

- 11.7 HiPP International

- 11.8 The Kraft Heinz Company

- 11.9 Plum, PBC

- 11.10 Ella's Kitchen Limited

- 11.11 Gerber Products Company

- 11.12 Sprout Foods, Inc.

- 11.13 Beech-Nut Nutrition Corporation

- 11.14 Bellamy's Organic Pty Ltd

- 11.15 Arla Foods amba

- 11.16 FrieslandCampina

- 11.17 Meiji Holdings Co., Ltd.

- 11.18 Topfer GmbH

- 11.19 Holle Baby Food GmbH

- 11.20 Riri Baby Food Co., Ltd.

全球嬰幼兒食品市場規模、佔有率、趨勢及成長分析報告(2026-2034)嬰兒食品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測

全球嬰幼兒食品市場規模、佔有率、趨勢及成長分析報告(2026-2034)嬰兒食品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測 植物性嬰幼兒食品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年

植物性嬰幼兒食品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、產品、分銷管道、地區和競爭格局分類,2021-2031年 嬰兒食品市場規模、佔有率和成長分析(按產品類型、人口統計、性質、分銷管道和地區分類)-2026-2033年產業預測

嬰兒食品市場規模、佔有率和成長分析(按產品類型、人口統計、性質、分銷管道和地區分類)-2026-2033年產業預測 嬰兒食品創新市場預測至2032年:按產品、規格、年齡層、分銷管道和地區分類的全球分析全球嬰幼兒食品市場-2025-2030年預測

嬰兒食品創新市場預測至2032年:按產品、規格、年齡層、分銷管道和地區分類的全球分析全球嬰幼兒食品市場-2025-2030年預測 美國嬰幼兒食品市場規模及預測(2021-2031年)、國家佔有率、趨勢和成長機會分析報告涵蓋範圍:按產品類型、類別、年齡層和配銷通路分類

美國嬰幼兒食品市場規模及預測(2021-2031年)、國家佔有率、趨勢和成長機會分析報告涵蓋範圍:按產品類型、類別、年齡層和配銷通路分類 全球植物來源嬰兒食品市場全球冷凍嬰兒食品市場

全球植物來源嬰兒食品市場全球冷凍嬰兒食品市場 嬰兒果汁市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

嬰兒果汁市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測