|

市場調查報告書

商品編碼

1740784

超材料吸收器材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Metamaterial Absorbers Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

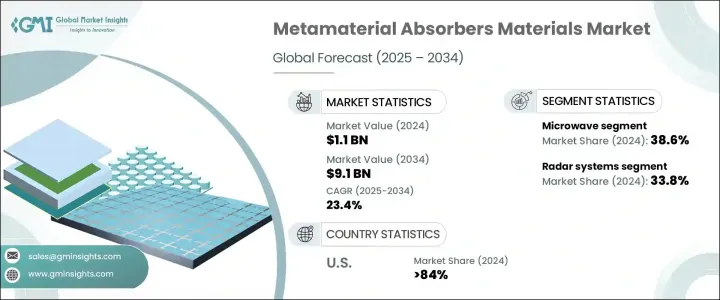

2024 年全球超材料吸波材料市場價值為 11 億美元,預計到 2034 年將以 23.4% 的複合年成長率成長,達到 91 億美元,這得益於對電磁干擾屏蔽的需求不斷成長以及對高頻通訊基礎設施(尤其是 5G 網路和其他先進系統)的投資不斷增加。在國防、電信、汽車和能源等領域,人們越來越關注吸波技術,以提高性能並減少訊號中斷。由於傳統材料難以應對高頻電磁波,超材料吸波材料透過在精確的諧振頻率下提供高吸收效率提供了一種有希望的解決方案。持續的研究和創新努力正在提高這些材料的可靠性和應用範圍,從而推動開發輕質、高性能的吸收技術,以應對現代基礎設施的挑戰。

這些先進材料透過工程結構操控電磁波,實現了近乎完全的吸收性能。此類吸波材料如今在民用和軍用領域對於提升隱身能力和最大程度減少反射都至關重要。近期的技術發展已透過先進的製造流程生產寬頻吸波材料,使其在環境電磁控制和雷達阻斷方面具有重要價值。超材料吸波材料設計靈活、性能強大,可整合到下一代航太、汽車和國防系統中。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 11億美元 |

| 預測值 | 91億美元 |

| 複合年成長率 | 23.4% |

根據頻率細分,微波吸波材料在2024年佔據最大佔有率,達到38.6%,這得益於其能夠有效抑制電磁波,同時重量輕且適用於軍事用途。這些材料透過最小化雷達截面,能夠有效降低雷達偵測風險,從而增強國防應用中的隱身能力。其高效性和易於整合的特性使其成為安全行業的首選。透過持續創新,擴大角度範圍和頻寬,該領域的市場主導地位得到了進一步鞏固。

2024年,雷達系統應用領域佔據33.8%的市場佔有率,這得益於超材料在提升偵測精度和降低雷達截面特徵方面無與倫比的能力。這些材料透過整合輕巧緊湊的組件,使雷達系統能夠高效運行,這些組件功耗更低,同時提供卓越的電磁波吸收性能。超材料吸波器的性能優勢使其成為速度、精度和隱身性至關重要的現代雷達應用的理想選擇。國防和國土安全部門持續的資金投入正在加速創新,其戰略重點是提高系統靈敏度,同時最大限度地降低可探測性。隨著研究的深入,雷達整合將繼續成為推動超材料吸波器材料市場成長的主要領域。

2024年,美國超材料吸波材料市場佔據84%的市場佔有率,產值達2億美元,這得益於其先進的軍事能力、強大的科研基礎設施以及聯邦機構對下一代國防技術的大力支持。美國在高性能國防和通訊系統超材料的研發和部署方面一直處於領先地位。憑藉持續的創新,該地區透過對研發的戰略投資、國防現代化項目以及政府機構與私營行業利益相關者之間的積極合作,保持了領先地位。

該市場的主要公司包括 Kymeta、Meta Materials Inc.、Metamagnetics、TeraView 和 Echodyne。這些公司透過投資專有技術、擴展產品組合、建立策略聯盟以及利用政府支持的研發項目來持續發展。他們也正在擴大產能並探索國防級認證,以增強全球競爭力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅的影響—結構化概述

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 主要出口國

- 國家 1

- 國家 2

- 國家 3

- 主要進口國

- 國家 1

- 國家 2

- 國家 3

- 主要出口國

註:以上貿易統計僅針對重點國家。

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 5G和下一代通訊的擴展

- 微型電子設備的使用日益增多,需要緊湊型吸收器

- 產業陷阱與挑戰

- 製造成本高、加工複雜

- 生產製造能耗高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按頻率,2021 - 2034 年

- 主要趨勢

- 頻率

- 微波

- 太赫茲

- 紅外線(IR)

- 其他

第6章:市場估計與預測:按材料類型,2021 - 2034 年

- 主要趨勢

- 電磁超材料

- 光子超材料

- 手性超材料

- 其他

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 雷達系統

- 隱形技術

- 無線通訊

- 醫學影像

- 太陽能收集

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Echodyne

- Entuple Technologies

- E-SONG EMC

- JEM Engineering

- Kymeta

- Meta Materials

- Metamagnetics

- MetaShield

- Microwave Measurement System

- Nanohmics

- Phoebus Optoelectronics

- TeraView

The Global Metamaterial Absorbers Materials Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 23.4% to reach USD 9.1 billion by 2034, driven by the increasing demand for electromagnetic interference shielding and rising investments in high-frequency communication infrastructure, particularly for 5G networks and other advanced systems. In sectors like defense, telecommunications, automotive, and energy, there is a growing focus on wave-absorbing technologies to enhance performance and reduce signal disruptions. As traditional materials struggle to cope with high-frequency electromagnetic waves, metamaterial absorbers offer a promising solution by delivering high absorption efficiency at precise resonance frequencies. Continued research and innovation efforts are enhancing the reliability and range of applications for these materials, enabling the development of lightweight, high-performance absorption technologies that address modern infrastructure challenges.

These advanced materials deliver near-complete absorption performance by manipulating electromagnetic waves with engineered structures. Such absorbers are now essential for improving stealth capabilities and minimizing reflection in both civil and military uses. Recent technological developments have produced broadband absorbers through advanced manufacturing processes, making them valuable for environmental electromagnetic control and radar blocking. With design flexibility and strong performance, metamaterial absorbers integrate into next-generation aerospace, automotive, and defense systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 23.4% |

Based on frequency segmentation, microwave frequency absorbers held the largest share at 38.6% in 2024 due to their ability to effectively dampen electromagnetic waves while being lightweight and adaptable for military use. These materials are highly effective in reducing radar detection by minimizing the radar cross-section, which enhances stealth capabilities in defense applications. Their efficiency and ease of integration make them the preferred choice across security-focused industries. Market dominance in this segment has been reinforced through ongoing innovation expanding angular range and bandwidth.

The radar system applications segment held a 33.8% share in 2024, driven by metamaterials' unmatched ability to enhance detection precision and reduce radar cross-section signatures. These materials allow radar systems to operate effectively by integrating lightweight, compact components that consume less power while delivering superior electromagnetic wave absorption. The performance benefits of metamaterial absorbers make them ideal for modern radar applications where speed, accuracy, and stealth are vital. Ongoing funding from defense and homeland security departments is accelerating innovation, with strategic emphasis on increasing system sensitivity while minimizing detectability. As research deepens, radar integration continues to stand out as a prime sector fueling growth in the metamaterial absorbers materials market.

United States Metamaterial Absorbers Materials Market held an 84% share in 2024 and generated USD 200 million reinforced by advanced military capabilities, a robust scientific infrastructure, and dedicated support from federal agencies for next-generation defense technologies. The U.S. has been at the forefront of developing and deploying metamaterials for high-performance defense and communication systems. With continued innovation, the region maintains its lead through strategic investment in R&D, defense modernization programs, and active collaboration between government institutions and private industry stakeholders.

Key companies in this market include Kymeta, Meta Materials Inc., Metamagnetics, TeraView, and Echodyne. These players are advancing by investing in proprietary technologies, expanding their product portfolios, forming strategic alliances, and leveraging government-backed R&D programs. They are also scaling production capacities and exploring defense-grade certifications to enhance global competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of 5g and next-gen communications

- 3.7.1.2 Growing use of miniaturized electronics requiring compact absorbers

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High manufacturing cost and complex processing

- 3.7.2.2 High energy consumption in production and fabrication

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Frequency, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Frequency

- 5.3 Microwave

- 5.4 Terahertz

- 5.5 Infrared (IR)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Electromagnetic metamaterials

- 6.3 Photonic metamaterials

- 6.4 Chiral metamaterials

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Radar systems

- 7.3 Stealth technology

- 7.4 Wireless communication

- 7.5 Medical imaging

- 7.6 Solar energy harvesting

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Echodyne

- 9.2 Entuple Technologies

- 9.3 E-SONG EMC

- 9.4 JEM Engineering

- 9.5 Kymeta

- 9.6 Meta Materials

- 9.7 Metamagnetics

- 9.8 MetaShield

- 9.9 Microwave Measurement System

- 9.10 Nanohmics

- 9.11 Phoebus Optoelectronics

- 9.12 TeraView

超材料市場:按類型、整合方法、頻段、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

超材料市場:按類型、整合方法、頻段、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 超材料市場(至 2035 年):依超材料類型、產品形式、應用、企業規模、終端用戶產業和地區劃分:產業趨勢和全球預測聲波超材料市場:按應用、類型、材料和頻率範圍分類,全球預測(2026-2032年)

超材料市場(至 2035 年):依超材料類型、產品形式、應用、企業規模、終端用戶產業和地區劃分:產業趨勢和全球預測聲波超材料市場:按應用、類型、材料和頻率範圍分類,全球預測(2026-2032年) 超材料市場:依類型、產品、波控制、應用和最終用戶劃分-全球預測至2036年

超材料市場:依類型、產品、波控制、應用和最終用戶劃分-全球預測至2036年 2034年全球電磁超材料市場機會與策略

2034年全球電磁超材料市場機會與策略 全球超材料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球超材料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球超材料市場按應用、最終用戶、產品、類型和地區分類-預測至2032年2026年全球超材料市場報告

全球超材料市場按應用、最終用戶、產品、類型和地區分類-預測至2032年2026年全球超材料市場報告 超材料市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測(2026-2033 年)平面超透鏡市場按類型、材質、波長和應用分類 - 全球預測 2026-2032

超材料市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測(2026-2033 年)平面超透鏡市場按類型、材質、波長和應用分類 - 全球預測 2026-2032