|

市場調查報告書

商品編碼

1721488

眼部過敏治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Eye Allergy Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

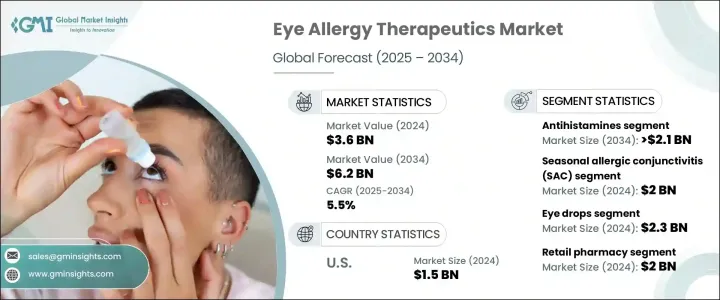

2024 年全球眼部過敏治療市場價值為 36 億美元,預計到 2034 年將以 5.5% 的複合年成長率成長,達到 62 億美元。隨著世界繼續面臨日益嚴重的空氣污染和氣候變遷的影響,過敏性結膜炎等眼睛過敏病例變得越來越常見。隨著都市化進程的加快,以及人們越來越頻繁地接觸室內外過敏原,如花粉、寵物皮屑和塵蟎,對更有效、更便捷的治療方法的需求也隨之激增。人們在空調和人工通風的空間裡度過的時間越來越多,這也增加了他們對環境觸發因素的敏感度。隨著越來越多的消費者積極尋求快速、安全、便利的治療方法,全球眼部過敏治療市場正在穩步成長。藥物輸送系統的技術進步以及對患者友善配方的更多重視正在重塑競爭格局。個人化醫療和標靶治療的轉變也為製藥公司提供了新的機遇,使其能夠提供更快、更持久的緩解的創新解決方案。

製藥商正在加大研發力度,以推出副作用最小的先進配方。處方藥和非處方藥 (OTC) 的普及擴大了治療管道,使消費者更容易控制症狀,而無需頻繁就診。美國食品藥物管理局 (FDA) 等監管機構透過批准新藥和輸送機制在這一成長中發揮關鍵作用。藥物洗脫隱形眼鏡和雙效眼藥水等產品正在擴大治療選擇並提高患者的依從性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 36億美元 |

| 預測值 | 62億美元 |

| 複合年成長率 | 5.5% |

市場依藥物類別細分為肥大細胞穩定劑、抗組織胺、雙重作用劑、減充血劑、皮質類固醇、免疫療法等。其中,抗組織胺藥物預計將成為主要的成長動力,預計年複合成長率為 5.4%,到 2034 年達到 21 億美元。這些藥物可以快速緩解搔癢、發紅和流淚等症狀,使其成為醫療保健提供者和患者的首選。由於可以透過處方藥和非處方藥管道輕鬆獲得抗組織胺藥,它已成為眼部過敏患者廣泛信賴的解決方案。

季節性過敏性結膜炎 (SAC) 領域仍然是主要的收入來源,到 2024 年將產生 20 億美元收入。在花粉水平達到高峰的春季和夏季,SAC 病例會激增,尤其是在污染嚴重的城市環境中。受積極的直接面對消費者的行銷活動的影響,消費者擴大轉向非處方藥,以提高認知度和便利性。

美國眼部過敏治療市場規模在 2024 年達到 15 億美元,並且在強力的監管監督和 FDA 對新療法的批准的支持下,該市場將繼續成長。零售連鎖店和藥局中非處方藥的便利供應為數百萬美國人提供了獲得治療的途徑。

領先的市場參與者包括 Bausch Health、AbbVie、Hikma Pharmaceuticals、輝瑞、Teva Pharmaceutical Industries、Regeneron Pharmaceuticals、賽諾菲、邁蘭、愛爾康、諾華、強生、Akorn、Nicox、參天製藥和太陽製藥。這些公司優先考慮產品創新、方便用戶使用解決方案和更廣泛的分銷合作夥伴關係。透過對自我管理療法、下一代隱形眼鏡和策略性零售聯盟的投資,產業領導者正在增強消費者參與度並加強其在全球市場的存在。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 污染和氣候變遷導致過敏性結膜炎盛行率上升

- 擴大採用聯合療法來提高療效

- 非處方抗過敏眼藥水銷售成長

- 藥物輸送系統的進展

- 產業陷阱與挑戰

- 長期用藥的副作用

- 低成本學名藥和非處方藥替代品的可用性

- 成長動力

- 成長潛力分析

- 監管格局

- 管道分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按藥物類別,2021 - 2034 年

- 主要趨勢

- 抗組織胺藥

- 肥大細胞穩定劑

- 雙重作用劑

- 皮質類固醇

- 減充血劑

- 免疫療法

- 其他藥物類別

第6章:市場估計與預測:按過敏類型,2021 - 2034 年

- 主要趨勢

- 季節性過敏性結膜炎(SAC)

- 常年性過敏性結膜炎(PAC)

- 春季角結膜炎(VKC)

- 特應性角結膜炎(AKC)

- 巨乳頭性結膜炎(GPC)

第7章:市場估計與預測:按劑型,2021 - 2034

- 主要趨勢

- 眼藥水

- 注射劑

- 口服片劑/膠囊

- 凝膠和軟膏

第8章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 醫院藥房

- 零售藥局

- 電子商務

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AbbVie

- Akorn

- Alcon

- Bausch Health

- Hikma Pharmaceuticals

- Johnson & Johnson

- Mylan

- Nicox

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Santen Pharmaceutical

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

The Global Eye Allergy Therapeutics Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 6.2 billion by 2034. As the world continues to face rising levels of air pollution and the impact of climate change, cases of eye allergies such as allergic conjunctivitis are becoming increasingly common. Growing urbanization, along with extended exposure to indoor and outdoor allergens like pollen, pet dander, and dust mites, is triggering a spike in demand for more effective and convenient treatments. People are spending more time in air-conditioned and artificially ventilated spaces, which has also increased their sensitivity to environmental triggers. With more consumers actively seeking quick, safe, and accessible treatments, the global market for eye allergy therapeutics is witnessing steady growth. Technological advancements in drug delivery systems and a greater emphasis on patient-friendly formulations are reshaping the competitive landscape. The shift toward personalized medicine and targeted therapies is also opening up new opportunities for pharmaceutical companies to deliver innovative solutions that offer faster and longer-lasting relief.

Pharmaceutical manufacturers are ramping up research and development efforts to introduce advanced formulations with minimal side effects. The availability of both prescription and over-the-counter (OTC) products has broadened treatment access, making it easier for consumers to manage symptoms without frequent clinical visits. Regulatory authorities like the U.S. Food and Drug Administration (FDA) are playing a pivotal role in this growth by approving new drugs and delivery mechanisms. Products like drug-eluting contact lenses and dual-action drops are expanding therapeutic options and improving patient compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.5% |

The market is segmented by drug class into mast cell stabilizers, antihistamines, dual-action agents, decongestants, corticosteroids, immunotherapy, and others. Among these, antihistamines are anticipated to be the primary growth driver, projected to grow at a CAGR of 5.4% and reach USD 2.1 billion by 2034. These medications offer rapid relief from symptoms such as itching, redness, and tearing, making them the go-to choice for both healthcare providers and patients. With easy availability through both prescription and OTC channels, antihistamines have become a widely trusted solution for eye allergy sufferers.

The seasonal allergic conjunctivitis (SAC) segment remains a major revenue generator, producing USD 2 billion in 2024. SAC cases surge in spring and summer when pollen levels peak, particularly in highly polluted urban environments. Consumers are increasingly turning to OTC remedies, influenced by aggressive direct-to-consumer marketing campaigns that promote awareness and convenience.

The U.S. Eye Allergy Therapeutics Market reached USD 1.5 billion in 2024 and continues to grow, supported by strong regulatory oversight and the FDA's approval of novel therapies. Easy OTC availability in retail chains and pharmacies has streamlined access to treatments for millions of Americans.

Leading market players include Bausch Health, AbbVie, Hikma Pharmaceuticals, Pfizer, Teva Pharmaceutical Industries, Regeneron Pharmaceuticals, Sanofi, Mylan, Alcon, Novartis, Johnson & Johnson, Akorn, Nicox, Santen Pharmaceutical, and Sun Pharmaceutical Industries. These companies are prioritizing product innovation, user-friendly solutions, and broader distribution partnerships. With investments in self-administered therapies, next-gen contact lenses, and strategic retail alliances, industry leaders are enhancing consumer engagement and strengthening their presence across the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of allergic conjunctivitis due to pollution and climate change

- 3.2.1.2 Increasing adoption of combination therapies for better efficacy

- 3.2.1.3 Growth in OTC allergy eye drops

- 3.2.1.4 Advancements in drug delivery systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of long-term medication use

- 3.2.2.2 Availability of low-cost generics and OTC alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antihistamines

- 5.3 Mast cell stabilizers

- 5.4 Dual-action agents

- 5.5 Corticosteroids

- 5.6 Decongestants

- 5.7 Immunotherapy

- 5.8 Other drug classes

Chapter 6 Market Estimates and Forecast, By Allergy Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Seasonal allergic conjunctivitis (SAC)

- 6.3 Perennial allergic conjunctivitis (PAC)

- 6.4 Vernal keratoconjunctivitis (VKC)

- 6.5 Atopic keratoconjunctivitis (AKC)

- 6.6 Giant papillary conjunctivitis (GPC)

Chapter 7 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Eye drops

- 7.3 Injectables

- 7.4 Oral tablets/capsules

- 7.5 Gels and ointments

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Retail pharmacy

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Akorn

- 10.3 Alcon

- 10.4 Bausch Health

- 10.5 Hikma Pharmaceuticals

- 10.6 Johnson & Johnson

- 10.7 Mylan

- 10.8 Nicox

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Regeneron Pharmaceuticals

- 10.12 Sanofi

- 10.13 Santen Pharmaceutical

- 10.14 Sun Pharmaceutical Industries

- 10.15 Teva Pharmaceutical Industries

眼科過敏治療市場:依產品類型、給藥途徑、通路和最終用戶分類-2026-2032年全球市場預測過敏治療市場:2026-2032年全球市場預測(依治療方法、過敏類型、銷售管道及最終用戶分類)

眼科過敏治療市場:依產品類型、給藥途徑、通路和最終用戶分類-2026-2032年全球市場預測過敏治療市場:2026-2032年全球市場預測(依治療方法、過敏類型、銷售管道及最終用戶分類) 過敏治療市場報告:按類型、治療方法、劑型、分銷管道和地區分類(2026-2034 年)皮膚過敏治療市場:2026-2032年全球市場預測(按治療分類、治療方法、患者年齡層、應用、分銷管道和最終用戶分類)

過敏治療市場報告:按類型、治療方法、劑型、分銷管道和地區分類(2026-2034 年)皮膚過敏治療市場:2026-2032年全球市場預測(按治療分類、治療方法、患者年齡層、應用、分銷管道和最終用戶分類) 過敏護理市場分析及預測(至2035年):按類型、產品類型、服務、技術、應用、形式、最終用戶和設備分類

過敏護理市場分析及預測(至2035年):按類型、產品類型、服務、技術、應用、形式、最終用戶和設備分類 2026-2034年全球皮膚過敏治療市場規模、佔有率、趨勢和成長分析報告全球過敏治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球皮膚過敏治療市場規模、佔有率、趨勢和成長分析報告全球過敏治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 過敏和免疫學市場 - 全球產業規模、佔有率、趨勢、機會和預測(按治療類型、過敏類型、分銷管道、地區和競爭格局分類,2021-2031年)過敏護理市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、療法、分銷管道、地區和競爭格局分類,2021-2031年

過敏和免疫學市場 - 全球產業規模、佔有率、趨勢、機會和預測(按治療類型、過敏類型、分銷管道、地區和競爭格局分類,2021-2031年)過敏護理市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、療法、分銷管道、地區和競爭格局分類,2021-2031年 全球樺木過敏市場:2032 年預測 - 按產品、治療類型、分銷管道、最終用戶和地區進行分析

全球樺木過敏市場:2032 年預測 - 按產品、治療類型、分銷管道、最終用戶和地區進行分析