|

市場調查報告書

商品編碼

1716573

汽車市場人工智慧機會、成長動力、產業趨勢分析及 2025 - 2034 年預測AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

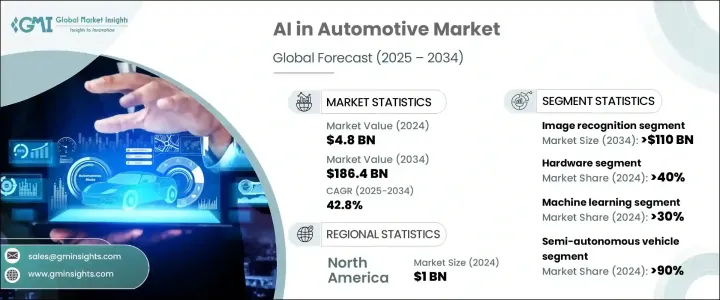

2024 年全球汽車人工智慧市場價值為 48 億美元,預計 2025 年至 2034 年間複合年成長率將達到驚人的 42.8%。隨著人工智慧技術繼續重新定義移動出行的未來,這種指數級成長反映了對智慧汽車解決方案日益成長的需求。人工智慧與車輛的融合正在改變汽車的運作方式,提升乘客的安全性和駕駛體驗。領先的汽車製造商和科技公司正在大力投資人工智慧驅動系統,特別是自動駕駛汽車和下一代高級駕駛輔助系統 (ADAS)。

人工智慧在增強車輛智慧、態勢感知和即時決策方面的作用正在推動汽車產業走向更安全、更互聯、更自主的未來。從交通管理和防撞到預測性維護和個人化車內體驗,人工智慧正在成為現代車輛架構的核心組成部分。汽車製造商也利用人工智慧提供預測導航、語音辨識和行為分析功能,提高駕駛和乘客的便利性。隨著消費者對更安全、更智慧的行動解決方案的需求不斷成長,人工智慧將成為汽車領域不可或缺的一部分,並在未來十年進一步加速市場成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 48億美元 |

| 預測值 | 1864億美元 |

| 複合年成長率 | 42.8% |

人工智慧應用的激增很大程度上是由 ADAS 和自動駕駛解決方案等技術的日益實施所推動的。人工智慧透過與先進感測器、高解析度攝影機、雷達和LiDAR系統的無縫整合,顯著提高了車輛安全性和整體駕駛體驗。車道維持輔助、自適應巡航控制、自動緊急煞車和行人偵測等功能均由人工智慧演算法提供支持,使車輛能夠分析周圍環境並做出即時駕駛決策,從而減少事故並提高道路安全。

市場主要根據資料探勘和影像辨識等流程進行細分,其中影像辨識佔據主導地位。由於該領域在實現自動駕駛汽車和 ADAS 功能方面發揮關鍵作用,預計到 2034 年該領域的產值將超過 1,100 億美元。影像辨識技術使人工智慧系統能夠處理和解釋即時環境資料,精確識別行人、交通標誌、車輛和車道標記。感知和理解動態路況的能力使影像辨識成為自動駕駛發展的基石。

從組件來看,汽車人工智慧市場分為硬體、軟體和服務,其中硬體在 2024 年將佔 40% 的佔有率。汽車製造商正在大力投資先進的硬體,以支援人工智慧汽車的運算需求。人工智慧晶片、GPU、感測器和LiDAR系統等專用組件對於處理大量資料流進行即時處理至關重要,可實現自動駕駛、影像偵測、感測器融合和基於深度學習的分析等無縫人工智慧功能。

由於美國強大的技術基礎設施和快速的人工智慧應用,美國汽車市場的人工智慧佔據了顯著的 33% 的佔有率,並在 2024 年創造了 10 億美元的產值。主要汽車製造商和科技巨頭在開發基於人工智慧的自動駕駛技術和先進安全系統方面處於領先地位,美國牢牢佔據著塑造全球人工智慧汽車格局的關鍵地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 技術提供者

- OEM製造商

- 經銷商

- 最終用途

- 利潤率分析

- 供應商格局

- 技術與創新格局

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 高級駕駛輔助系統 (ADAS) 和自動駕駛汽車

- 增強車輛安全性和防撞功能

- 預測性維護和車隊管理

- 人工智慧車載資訊娛樂和語音助手

- 產業陷阱與挑戰

- 實施成本高且整合複雜

- 資料隱私和網路安全問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 軟體

- 服務

第6章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 電腦視覺

- 情境感知

- 深度學習

- 機器學習

- 自然語言處理(NLP)

第7章:市場估計與預測:按工藝,2021 - 2034 年

- 主要趨勢

- 資料探勘

- 影像辨識

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 半自動駕駛汽車

- 完全自動駕駛汽車

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Alphabet

- Audi

- Bayerische Motoren Werke (BMW)

- Daimler

- Didi Chuxing

- Ford Motor

- General Motors

- Harman International Industries

- Honda Motor

- Intel

- International Business Machines (IBM)

- Microsoft

- NVIDIA

- Qualcomm

- Tesla

- Toyota Motor

- Uber Technologies

- Volvo Car

- Waymo

- Xilinx

The Global AI In Automotive Market was valued at USD 4.8 billion in 2024 and is projected to witness a staggering CAGR of 42.8% between 2025 and 2034. This exponential growth reflects the rising demand for intelligent automotive solutions as AI technologies continue to redefine the future of mobility. The integration of AI into vehicles is transforming the way cars operate, elevating both the safety and driving experience of passengers. Leading automakers and technology companies are heavily investing in AI-driven systems, particularly for autonomous vehicles and next-generation Advanced Driver Assistance Systems (ADAS).

AI's role in enhancing vehicle intelligence, situational awareness, and real-time decision-making is pushing the automotive sector toward a future where cars are safer, more connected, and increasingly autonomous. From traffic management and collision avoidance to predictive maintenance and personalized in-car experiences, AI is becoming a central component of modern vehicle architecture. Automakers are also capitalizing on AI to offer predictive navigation, voice recognition, and behavior analysis features, enhancing both driver and passenger convenience. With growing consumer demand for safer and smarter mobility solutions, AI is set to become indispensable in the automotive world, further accelerating market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $186.4 Billion |

| CAGR | 42.8% |

The surge in AI adoption is largely driven by the increasing implementation of technologies such as ADAS and autonomous driving solutions. AI significantly enhances vehicle safety and overall driving experience through seamless integration with advanced sensors, high-resolution cameras, radar, and LiDAR systems. Features like lane-keeping assistance, adaptive cruise control, automatic emergency braking, and pedestrian detection are powered by AI algorithms that enable vehicles to analyze their surroundings and make instant driving decisions, reducing accidents and improving road safety.

The market is primarily segmented based on processes like data mining and image recognition, with image recognition dominating the landscape. This segment is expected to generate over USD 110 billion by 2034, driven by its critical role in enabling autonomous vehicles and ADAS functionalities. Image recognition technology allows AI systems to process and interpret real-time environmental data, identifying pedestrians, traffic signs, vehicles, and lane markings with precision. The ability to perceive and understand dynamic road conditions makes image recognition a cornerstone of autonomous driving development.

In terms of components, the AI in automotive market is divided into hardware, software, and services, with hardware accounting for a significant 40% share in 2024. Automotive manufacturers are heavily investing in advanced hardware to support the computational demands of AI-powered vehicles. Specialized components such as AI chips, GPUs, sensors, and LiDAR systems are essential to handle vast streams of data for real-time processing, enabling seamless AI functionalities like automated driving, image detection, sensor fusion, and deep learning-based analytics.

The U.S. AI in automotive market commanded a notable 33% share and generated USD 1 billion in 2024, thanks to the country's robust technological infrastructure and rapid AI adoption. Major automakers and tech giants are leading the charge in developing AI-based autonomous driving technologies and advanced safety systems, firmly positioning the U.S. as a key player in shaping the global AI-driven automotive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 OEM Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicles

- 3.5.1.2 Enhanced Vehicle Safety and Collision Avoidance

- 3.5.1.3 Predictive Maintenance and Fleet Management

- 3.5.1.4 AI-powered In-Vehicle Infotainment and Voice Assistants

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High Implementation Costs and Integration Complexity

- 3.5.2.2 Data Privacy and Cybersecurity Concerns

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Computer vision

- 6.3 Context awareness

- 6.4 Deep learning

- 6.5 Machine learning

- 6.6 Natural Language Processing (NLP)

Chapter 7 Market Estimates & Forecast, By Process, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Data mining

- 7.3 Image recognition

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Semi-Autonomous vehicles

- 8.3 Fully Autonomous vehicles

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet

- 10.2 Audi

- 10.3 Bayerische Motoren Werke (BMW)

- 10.4 Daimler

- 10.5 Didi Chuxing

- 10.6 Ford Motor

- 10.7 General Motors

- 10.8 Harman International Industries

- 10.9 Honda Motor

- 10.10 Intel

- 10.11 International Business Machines (IBM)

- 10.12 Microsoft

- 10.13 NVIDIA

- 10.14 Qualcomm

- 10.15 Tesla

- 10.16 Toyota Motor

- 10.17 Uber Technologies

- 10.18 Volvo Car

- 10.19 Waymo

- 10.20 Xilinx

汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類

汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類 2026年全球汽車人工智慧市場報告

2026年全球汽車人工智慧市場報告 2026-2030年全球汽車技術市場

2026-2030年全球汽車技術市場 汽車人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球汽車人工智慧市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車人工智慧市場規模、佔有率、趨勢和成長分析報告 汽車人工智慧(AI)市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、技術、工藝、應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031)車輛智慧系統市場-全球產業規模、佔有率、趨勢、機會與預測:按道路場景理解、車輛類型、進階駕駛輔助與監控、地區和競爭格局分類,2021-2031年

汽車人工智慧(AI)市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、技術、工藝、應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031)車輛智慧系統市場-全球產業規模、佔有率、趨勢、機會與預測:按道路場景理解、車輛類型、進階駕駛輔助與監控、地區和競爭格局分類,2021-2031年 汽車人工智慧模擬與合成資料生成市場機會、成長要素、產業趨勢分析及2026年至2035年預測

汽車人工智慧模擬與合成資料生成市場機會、成長要素、產業趨勢分析及2026年至2035年預測 汽車語音AI助理市場規模、佔有率及預測:依AI引擎(自然語言理解、自然語言處理)、語言支援、整合類型(原生、雲端連接)及功能(導航、媒體、車輛控制)劃分-全球預測至2036年

汽車語音AI助理市場規模、佔有率及預測:依AI引擎(自然語言理解、自然語言處理)、語言支援、整合類型(原生、雲端連接)及功能(導航、媒體、車輛控制)劃分-全球預測至2036年 AIGC平台模型市場:2026-2032年全球預測(按模型類型、部署格式、應用和產業分類)

AIGC平台模型市場:2026-2032年全球預測(按模型類型、部署格式、應用和產業分類)