|

市場調查報告書

商品編碼

1708222

高阻隔包裝薄膜市場機會、成長動力、產業趨勢分析及2025-2034年預測High Barrier Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

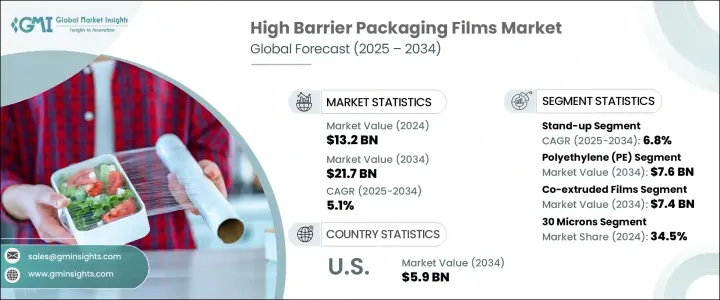

2024 年全球高阻隔包裝薄膜市場規模達 132 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5.1%,這得益於製藥行業的快速成長、電子商務的擴張以及在線食品配送服務日益普及。隨著製藥公司不斷創新和擴張,對保護敏感產品的先進包裝解決方案的需求變得更加迫切。高阻隔包裝膜可確保最佳地防止濕氣、氧氣和其他污染物,同時延長藥品的保存期限。此外,電子商務行業的蓬勃發展和線上食品配送服務的激增進一步刺激了對在運輸和儲存過程中保持產品完整性的高性能包裝的需求。消費者對安全、衛生和永續包裝的期望不斷提高也促進了市場的成長。此外,不斷增強的環保意識正在推動製造商投資可回收、可生物分解和高阻隔材料,以符合循環經濟目標。

市場涵蓋各種包裝形式,包括自立袋、平袋、袋子和麻袋、泡殼和蛤殼、包裝和蓋膜、小袋和條形包裝。其中,自立袋預計將經歷最高成長,到 2034 年的複合年成長率為 6.8%。這種成長主要歸因於消費者對輕量、高阻隔軟包裝的偏好日益成長,尤其是對於零食和即食食品而言。製造商擴大採用高品質的可回收材料並整合先進的可重新密封功能,以滿足消費者對便利性和永續性的需求。隨著對塑膠廢物的環境擔憂日益加劇,產業參與者正在開發減少環境影響同時保持產品安全和新鮮度的包裝解決方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 132億美元 |

| 預測值 | 217億美元 |

| 複合年成長率 | 5.1% |

就材料種類而言,高阻隔包裝薄膜市場分為聚乙烯(PE)、聚丙烯(PP)、聚對苯二甲酸乙二醇酯(PET)、聚偏氯乙烯(PVDC)、乙烯乙烯醇(EVOH)、聚醯胺(尼龍)等。聚乙烯 (PE) 預計將佔據該領域的主導地位,到 2034 年將達到 76 億美元。隨著公司強調永續實踐以滿足監管要求和客戶期望,可回收和生物基 PE 材料正在發生顯著轉變。製造商正在開發創新的單一材料 PE 薄膜,這種薄膜具有卓越的氧氣和防潮性能,在確保產品保護的同時促進永續性。 PE 材料的這些進步正在推動這一領域的成長,並滿足對環保包裝日益成長的需求。

受簡便食品和即食食品需求不斷成長的推動,北美高阻隔包裝薄膜市場在 2024 年佔據 38.4% 的佔有率。隨著消費者偏好轉向保存期限更長、更新鮮的包裝食品,對高阻隔包裝解決方案的需求持續成長。該地區預包裝冷凍食品、零食和食品托盤的消費量顯著成長,這進一步推動了高阻隔包裝薄膜的採用。此外,該地區對創新的高度重視,加上對永續和環保包裝解決方案日益成長的需求,預計將保持北美在市場上的主導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 電子商務和線上食品配送的成長

- 製藥業擴張

- 真空和氣調包裝(MAP)的需求不斷成長

- 乳製品和肉類包裝產業的擴張

- 快速的城市化和不斷變化的生活方式推動包裝商品

- 產業陷阱與挑戰

- 先進阻隔膜生產成本高

- 石化產品價格波動影響原物料供應

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按材料類型,2021 - 2034 年

- 主要趨勢

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二酯(PET)

- 聚偏二氯乙烯(PVDC)

- 乙烯乙烯醇 (EVOH)

- 聚醯胺(尼龍)

- 其他

第6章:市場估計與預測:依包裝形式,2021 - 2034 年

- 主要趨勢

- 自立袋

- 扁平袋

- 袋子和麻袋

- 水泡和蛤殼

- 包裝膜和蓋膜

- 小袋裝和條狀包裝

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 共擠薄膜

- 金屬化薄膜

- 濺鍍薄膜

- 原子層沉積(ALD)薄膜

- 層壓薄膜

第8章:市場預估與預測:依薄膜厚度,2021 - 2034 年

- 主要趨勢

- 高達 30 微米

- 30-50微米

- 50-70微米

- 70微米以上

第9章:市場估計與預測:依應用類型,2021 - 2034

- 主要趨勢

- 新鮮食品包裝

- 加工食品包裝

- 飲料包裝

- 保健產品

- 個人護理和化妝品

- 工業部件

- 農產品

第 10 章:市場估計與預測:按最終用途產業,2021 年至 2034 年

- 主要趨勢

- 食品和飲料

- 製藥和醫療

- 電子和半導體

- 工業的

- 其他

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第12章:公司簡介

- 3M

- ACG

- Amcor

- Bemis Manufacturing

- Berry Global

- Celplast Metallized Products

- Cosmo Films

- Innovia Films

- Jindal Poly Films

- Klockner Pentaplast

- Mitsubishi Chemical Advanced Materials

- Mondi

- Oike

- Perlen Packaging

- Sealed Air

- Sigma Plastics Group

- Sonoco Products

- Toppan

- Toray Plastics

- Uflex

- Winpak

The Global High Barrier Packaging Films Market generated USD 13.2 billion in 2024 and is expected to grow at a CAGR of 5.1% from 2025 to 2034, driven by the rapid growth of the pharmaceutical sector, the expansion of e-commerce, and the increasing popularity of online food delivery services. As pharmaceutical companies continue to innovate and expand, the need for advanced packaging solutions that protect sensitive products becomes more critical. High barrier packaging films ensure optimal protection against moisture, oxygen, and other contaminants while extending the shelf life of pharmaceuticals. Moreover, the booming e-commerce industry and the surge in online food delivery services have further fueled the demand for high-performance packaging that maintains product integrity during shipping and storage. Rising consumer expectations for secure, hygienic, and sustainable packaging have also contributed to market growth. Additionally, increasing environmental awareness is driving manufacturers to invest in recyclable, biodegradable, and high-barrier materials to align with circular economy goals.

The market encompasses a variety of packaging formats, including stand-up pouches, flat pouches, bags and sacks, blisters and clamshells, wraps and lidding films, and sachets and stick packs. Among these, stand-up pouches are projected to experience the highest growth, with a CAGR of 6.8% through 2034. This growth is largely attributed to the rising consumer preference for lightweight, high-barrier flexible packaging, particularly for snacks and ready-to-eat meals. Manufacturers are increasingly adopting high-quality recyclable materials and integrating advanced resealable features to meet consumer demands for convenience and sustainability. As environmental concerns about plastic waste intensify, industry players are developing packaging solutions that reduce environmental impact while maintaining product safety and freshness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.2 Billion |

| Forecast Value | $21.7 Billion |

| CAGR | 5.1% |

In terms of material type, the high barrier packaging films market is segmented into polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyvinylidene chloride (PVDC), ethylene vinyl alcohol (EVOH), polyamide (nylon), and others. Polyethylene (PE) is expected to dominate the segment, reaching USD 7.6 billion by 2034. A notable shift is underway towards recyclable and bio-based PE materials as companies emphasize sustainable practices to meet regulatory requirements and customer expectations. Manufacturers are developing innovative mono-material PE films that offer superior oxygen and moisture barriers, ensuring product protection while promoting sustainability. These advancements in PE materials are driving the growth of this segment and catering to the rising demand for environmentally responsible packaging.

North America High Barrier Packaging Films Market held a 38.4% share in 2024, propelled by increasing demand for convenience foods and ready-to-eat meals. As consumer preferences shift towards packaged foods that provide extended shelf life and freshness, the demand for high-barrier packaging solutions continues to grow. The region is witnessing a notable rise in the consumption of prepackaged frozen meals, snacks, and food trays, which further boosts the adoption of high barrier packaging films. Additionally, the region's strong emphasis on innovation, combined with the growing need for sustainable and eco-friendly packaging solutions, is expected to maintain North America's dominant position in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce and online food delivery

- 3.2.1.2 Expansion of pharmaceutical industry

- 3.2.1.3 Rising demand for vacuum and modified atmosphere packaging (MAP)

- 3.2.1.4 Expansion of the dairy and meat packaging industry

- 3.2.1.5 Rapid urbanization and changing lifestyles driving packaged goods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs of advanced barrier films

- 3.2.2.2 Volatility in petrochemical prices affecting raw material supply

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.3 Polypropylene (PP)

- 5.4 Polyethylene Terephthalate (PET)

- 5.5 Polyvinylidene Chloride (PVDC)

- 5.6 Ethylene Vinyl Alcohol (EVOH)

- 5.7 Polyamide (Nylon)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Packaging Format, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Stand-up pouches

- 6.3 Flat pouches

- 6.4 Bags & sacks

- 6.5 Blisters & clamshells

- 6.6 Wraps & lidding films

- 6.7 Sachets & stick packs

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Co-extruded films

- 7.3 Metallized films

- 7.4 Sputtered films

- 7.5 Atomic Layer Deposition (ALD) Films

- 7.6 Laminated films

Chapter 8 Market Estimates & Forecast, By Film Thickness, 2021 - 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Up to 30 microns

- 8.3 30-50 microns

- 8.4 50-70 microns

- 8.5 Above 70 microns

Chapter 9 Market Estimates & Forecast, By Application Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 Fresh food packaging

- 9.3 Processed food packaging

- 9.4 Beverage packaging

- 9.5 Healthcare products

- 9.6 Personal care & cosmetics

- 9.7 Industrial components

- 9.8 Agricultural products

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Kilo Tons)

- 10.1 Key trends

- 10.2 Food & beverages

- 10.3 Pharmaceuticals & medical

- 10.4 Electronics & semiconductor

- 10.5 Industrial

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 ACG

- 12.3 Amcor

- 12.4 Bemis Manufacturing

- 12.5 Berry Global

- 12.6 Celplast Metallized Products

- 12.7 Cosmo Films

- 12.8 Innovia Films

- 12.9 Jindal Poly Films

- 12.10 Klockner Pentaplast

- 12.11 Mitsubishi Chemical Advanced Materials

- 12.12 Mondi

- 12.13 Oike

- 12.14 Perlen Packaging

- 12.15 Sealed Air

- 12.16 Sigma Plastics Group

- 12.17 Sonoco Products

- 12.18 Toppan

- 12.19 Toray Plastics

- 12.20 Uflex

- 12.21 Winpak